Value v quality investing, greedflation, startup fraud, finfluencers, Japan, car makers and mining, rising ocean temperatures

Value v quality investing, greedflation, startup fraud, finfluencers, Japan, car makers and mining, rising ocean temperatures

#Newsletter 30

Hello all, welcome to the latest edition of Markets and Macros by TradingQnA.

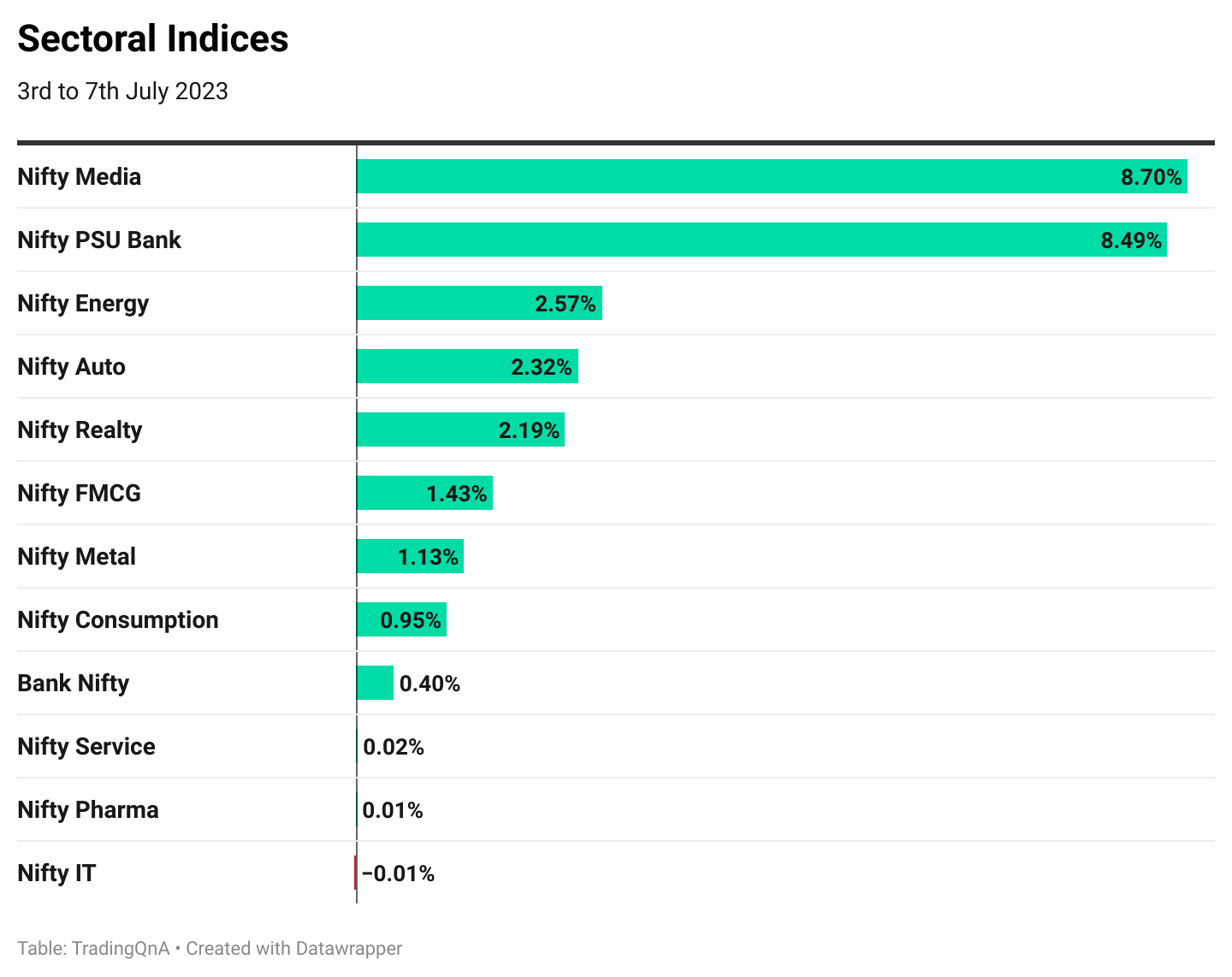

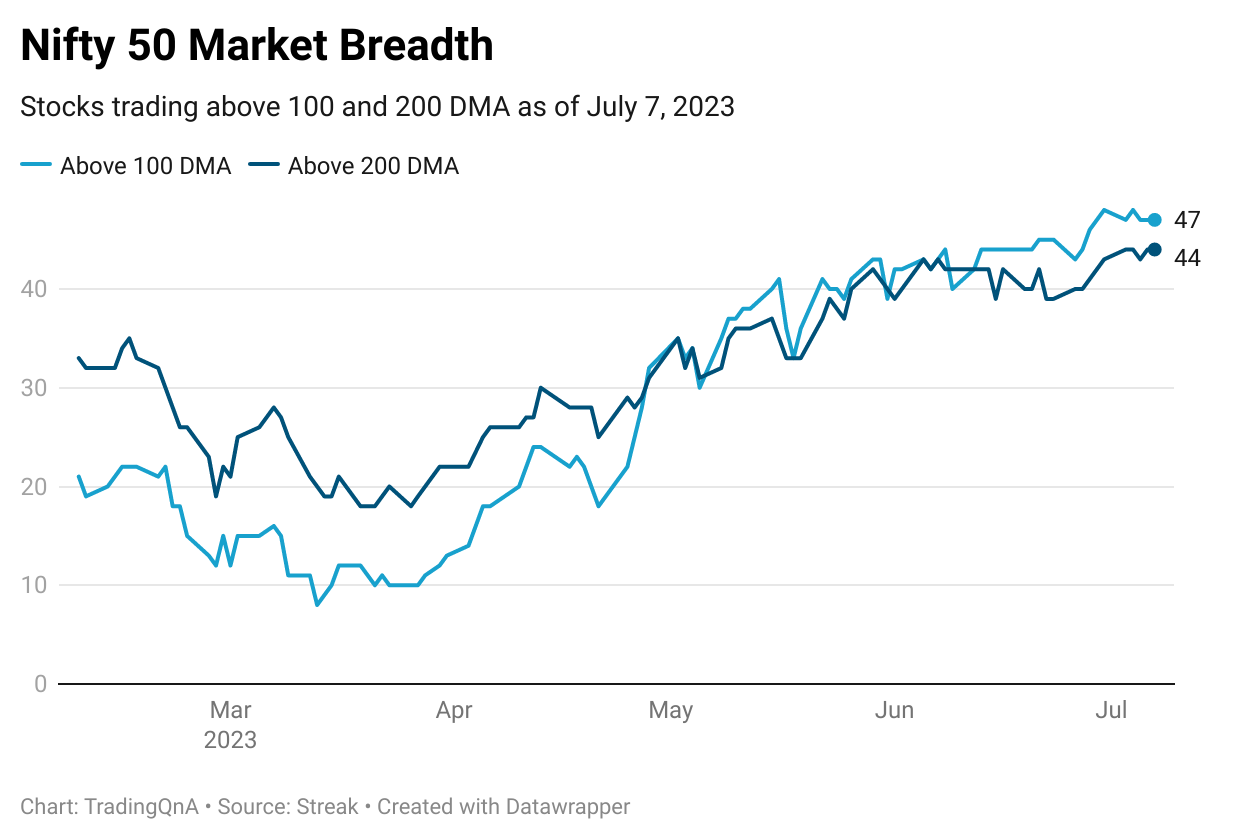

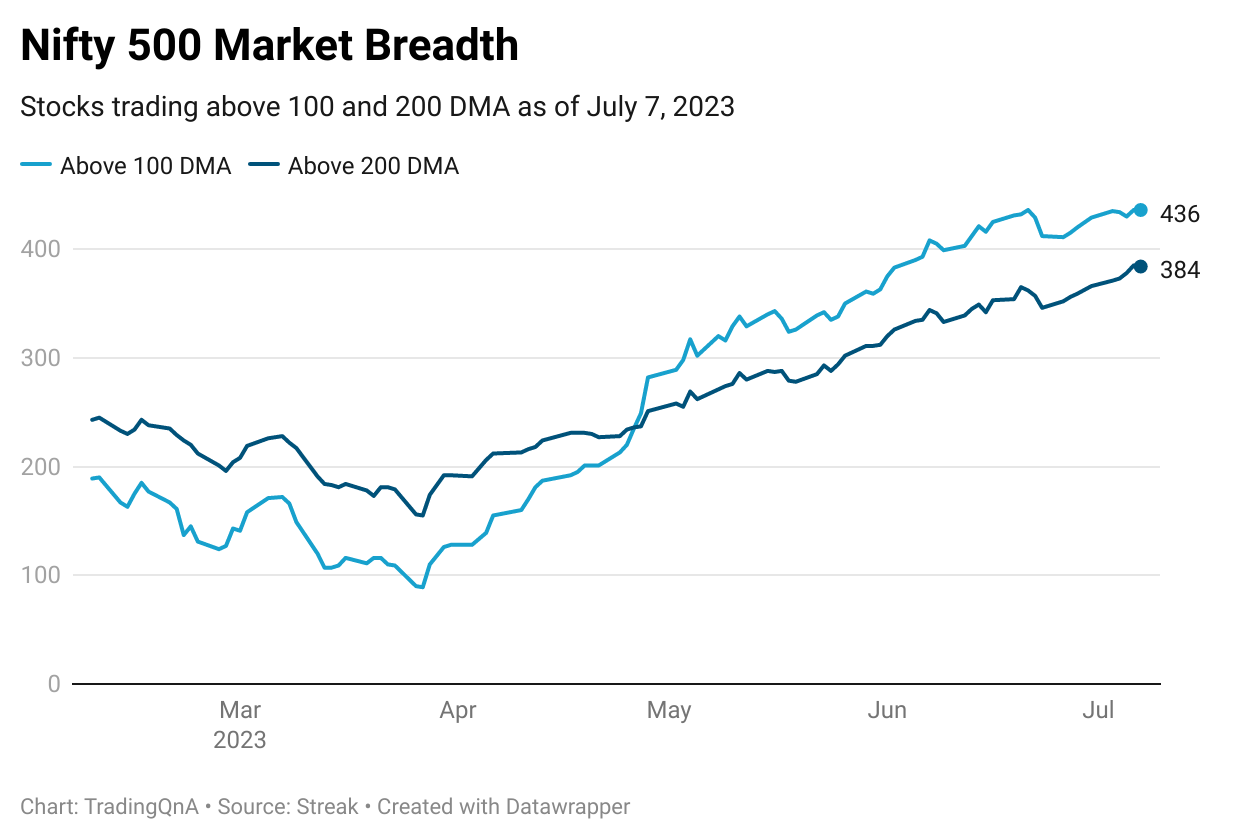

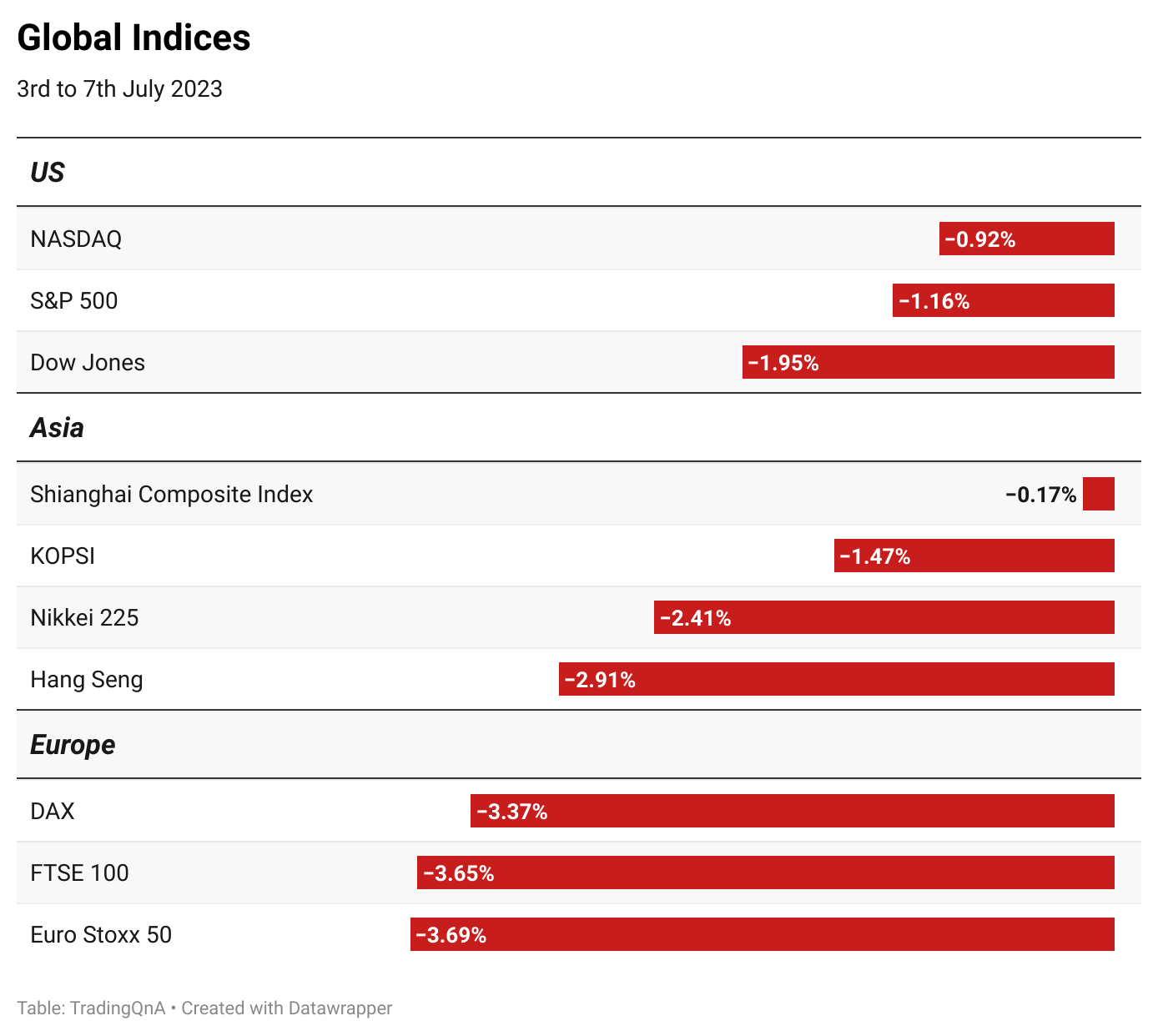

Weekly market wrap

A quick look at how the markets performed in the week ending July 7, 2023;

Value investing versus quality investing

Value investing vs. quality investing is one of the oldest debates in finance. Verdad has come up with an interesting piece that helps to sort out this dilemma.

In a paper, Robert Novy-Marx says that value and quality are philosophically and economically related as they both aim to generate returns in companies by purchasing them at a discount.

There's a long debate about the similarities and differences between value and quality The differences between value and quality mean that they are complementary in a portfolio as they work in different ways and at different times.

Both strategies have exhibited a factor premium over a long period of time. Thus there should ideally be no dilemma. Value and quality should both be key ingredients in building a portfolio that aims to outperform the market in the long run.

Greedflation

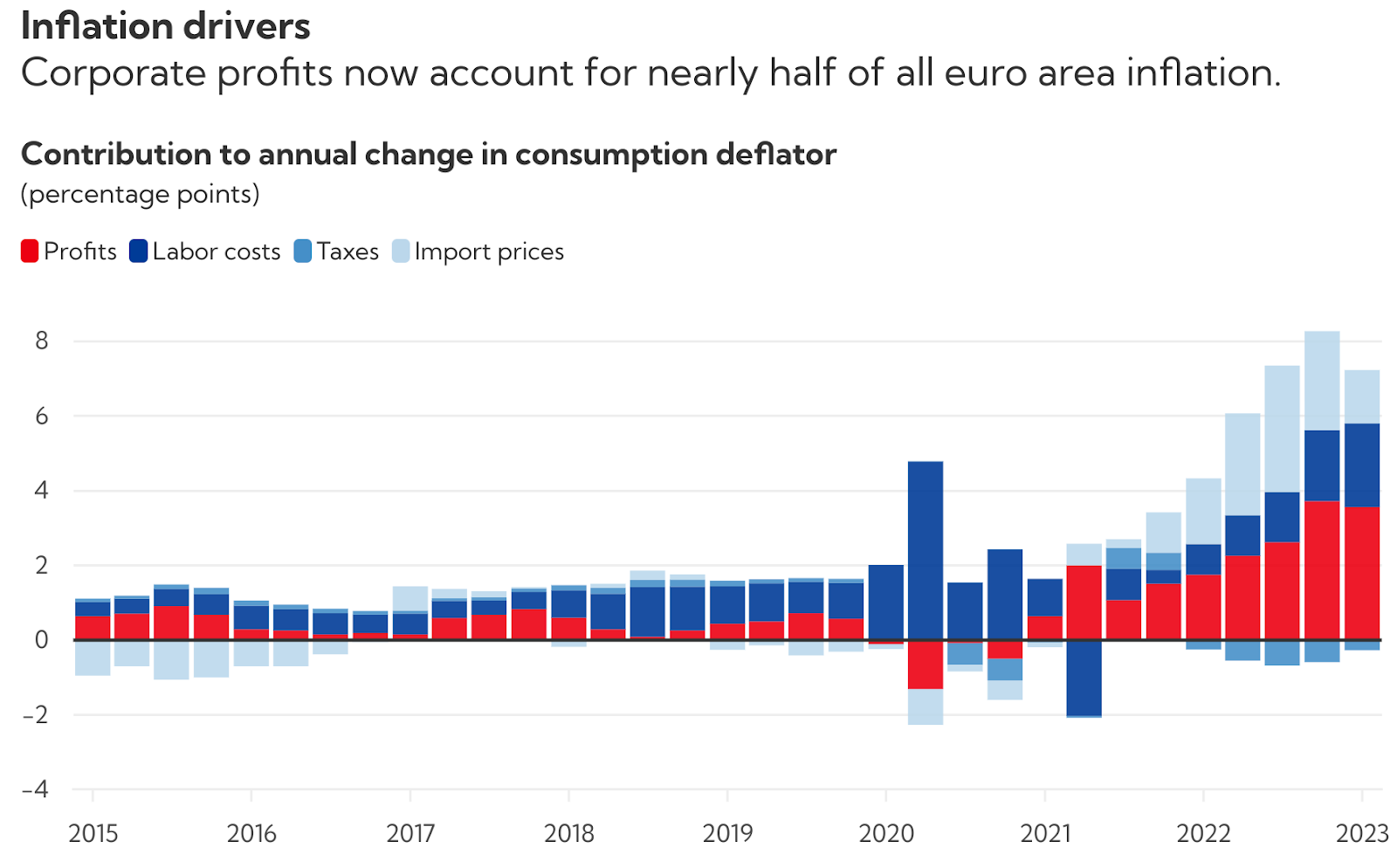

What is greedflation?

Greedflation implies that companies exploited the inflation that people were experiencing by putting up their prices way beyond just covering their increased costs and then used that to maximise their profit margins. That, in turn, further fuelled inflation.

As per IMF (International Monetary Fund) rising corporate profits accounted for 45% of the increase in Europe’s inflation since 2022 due to companies increasing prices by more than the increase in costs of imported energy. Import costs accounted for about 40% of inflation and labour costs accounted for 25%.

Source: IMF

What happened to wages? There was a lag in wage gains as wages are slower than prices to react to shocks. But now that wages have dipped by 5%, in real terms in 2022, workers are pushing for pay rises.

You can listen to this podcast with Philip R. Lane, Chief Economist of the European Central Bank on this issue.

https://www.ecb.europa.eu/press/tvservices/podcast/html/ecb.pod230623_episode62.en.html

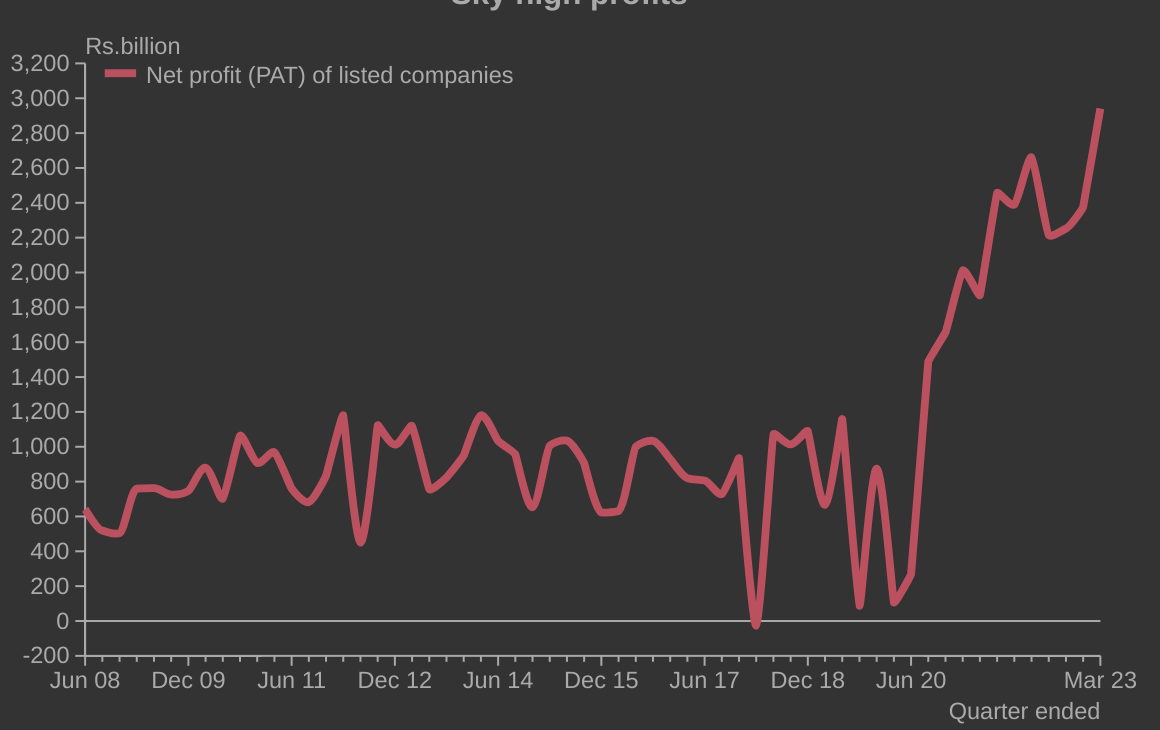

Is India also witnessing greedflation?

The profit after tax (PAT) of Indian companies over the last 2 decades is shown below

Source: CMIE

Net profits of 4,293 listed companies reached Rs.2.9 trillion in the March 2023 quarter. This is over 3.5 times the average quarterly profit earned by listed companies till before the pandemic of 2020

As per CMIE (quoted in this Indian Express article)

sixty per cent of the growth in net profit can be attributed entirely to the increase in profit margin. The increase in sales contributed an additional 36 per cent and the rest was a bonus from a combination of the two.

The golden age of fraud

A previous newsletter was titled “The Golden Age of Fraud” which talked about bubbles, manias and frauds. You can also watch Jim Chanos, who coined the term, talk about it

In the newsletter, I had said

the other area where we could potentially see a lot of blow-ups are companies with high debt or zombie companies

The chickens have come home to roost.

We are now seeing this unfold in the Indian context too with many frauds coming to light. Be it Go Mechanic’s financial misreporting, financial irregularities at Zillingo, Sequoia’s exit from Trell after allegations of irregularities, allegations of fraud in Bikayi or the very well-covered alleged misappropriation of funds at Bharatpe. Freshly joining this list is Mojocare.

The story of all these companies mentioned above are eerily similar, hinting at a systemic issue with the Indian startup ecosystem. What can this be? Well, the folks at Finshots have covered this.

Japanese economic turnaround

A previous newsletter covered how when other central banks were hiking interest rates one exception was the Bank of Japan (BOJ). It kept interest rates lower at -0.1% despite inflation surging to its highest levels in 40 years (3%). BOJ felt that making money more expensive would only suppress the already weak demand and set back economic recovery.

The inflation pressure was due to the strong dollar and supply issues affecting imports — factors outside BOJ's control. Increasing interest rates would not have affected the price pressures and would have only increased business costs. This NYTimes article explores this in more detail.

It looked like an interesting story and I had said that let’s revisit this issue later and see what’s in store. So here we are. Let’s take a look at the Japanese economy.

As per Deloitte, Japan's economy struggled to bounce back after fully reopening last year. In Q3 2022, the real GDP contracted and in Q4 it only managed to grow 0.1% on an annualised basis. Despite initial setbacks, recent data suggests economic recovery as the economy gains momentum in 2023.

Due to the economic rebound, inflation has been above BoJ’s 2% target. It has still maintained its accommodative monetary policy stance but we might now see modest tightening.

BOJ introduced its current monetary easing policy in 2013 during Shinzo Abe’s presidency. Abe’s strategy had three “arrows” aimed at kick-starting economic growth and higher wages: loose monetary policy, fiscal stimulus and structural economic reforms. Al Jazeera had written about Abenomics: Abe’s economic legacy aimed for Japan’s revival, after his assassination last year.

Finfluencers face the heat

In a recent press conference after the SEBI board meeting, Chairperson Madhabi Puri Buch was asked about the regulator’s views on finfluencers. Here is what she had to say (See from 42:50 onwards)

https://www.youtube.com/live/jwdrxyGTTOw?feature=share

She spoke about this in Hindi and here is a translation of what she said:

You would have observed that we have, in the recent past, passed some orders. Beyond that, Sebi is crystallising its views on this matter.

In a few months, we will come out with a consultation paper.

One essential element in this will be that entities regulated by Sebi, such as exchanges, brokers, mutual funds, etc., will not in any way—whether by way of advertising, equity, profit sharing, referral fee, etc.—be involved with unregistered entities. Sebi’s thinking is that if an entity is regulated by Sebi, your partners and those with whom you have relationships should also be regulated. So, you will not be able to advertise on channels and other mediums of unregulated entities. You will not be able to give them referral fees. You will not be able to give your link there. This will be an important element of our consultation paper which is not yet ready. But this much has been crystallised.

If someone is genuinely educating people; this is, in fact, good because our objective too is to have investor awareness and education. But if someone gives inducements—for instance, that you can make lakhs and crores of rupees if you trade, and can become fabulously rich in just a couple of years (genuine experts know that such things don’t happen in the market, there is no guarantee, Warren Buffett can also make a loss) or represent to people that this is a guaranteed way of making money—it will be considered an inducement in our system, and as fraudulent, misrepresentation, misleading activity.

They don’t come under our (regulatory) ambit. If one has a social contract with someone—for instance, if someone advises their uncle about where to invest—we can’t go after them.

It is not our intention to regulate those who teach people about investing. But if someone gives advice, stock recommendations, portfolio recommendations, they need to be registered with us. It’s already a part of the Investment Advisor law. But if you are an educator and stay with education, we have no problem at all.

It seems that the finfluencer party is in its last stages.

TLDR version of what she said:

A significant portion of their income could vanish as SEBI-regulated entities will no longer be able to do business with them. Finfluencers will have to stick to financial education.

A replacement for the 23-year-old Information Technology Act, 2000

The Information Technology Act, 2000 (IT Act) predates Facebook and other familiar names in the digital domain. The draft Digital India Act (DIA), will be the replacement of the 23-year-old IT Act.

It will retain a lot of the old provisions and will include provisions to address new-age crimes such as cyberbullying, improper and unauthorised digital use of government-issued identity cards and misinformation.

Inflation around the world

Source: New York Times

Newest entrants in the mining industry: Automobile makers

Lithium scarcity is pushing the automobile industry into mining as Ford, General Motors and others strike deals with mining companies to avoid raw material shortages to avoid hiccups to their electric vehicle plans.

They are scrambling to lock up exclusive access to smaller mines before others swoop in. The problem here is that they will now be exposed to the risky business of mining, often located in politically unstable countries with weak environmental protections.

“Auto executives said they had no choice because there weren’t sufficient reliable supplies of lithium and other battery materials, like nickel and cobalt, for the millions of electric vehicles the world needs.”

Ocean temperatures off the charts

In a previous newsletter I had talked about a positive development, the world had finally reached an agreement to protect the oceans. But there is a big problem with the oceans, which ought to get more coverage than the oceangate saga, the average ocean temperatures are off the charts.

What are the possible implications? In short, marine heatwaves starve the oceans of oxygen. Food chains collapse. Heat accumulates. Ocean currents stop.

Listening recommendations

That's all from us for this issue. Thank you for reading. Do let us know your feedback in the comments below and share the post if you liked it. We are at @TradingQnA on Twitter.