The golden age of fraud

Issue #15

Hello and welcome to the latest edition of Markets and Macros by TradingQnA. In this issue;

Bubbles, manias, and frauds

Weekly market wrap

Planning for longevity risk in retirement and more…

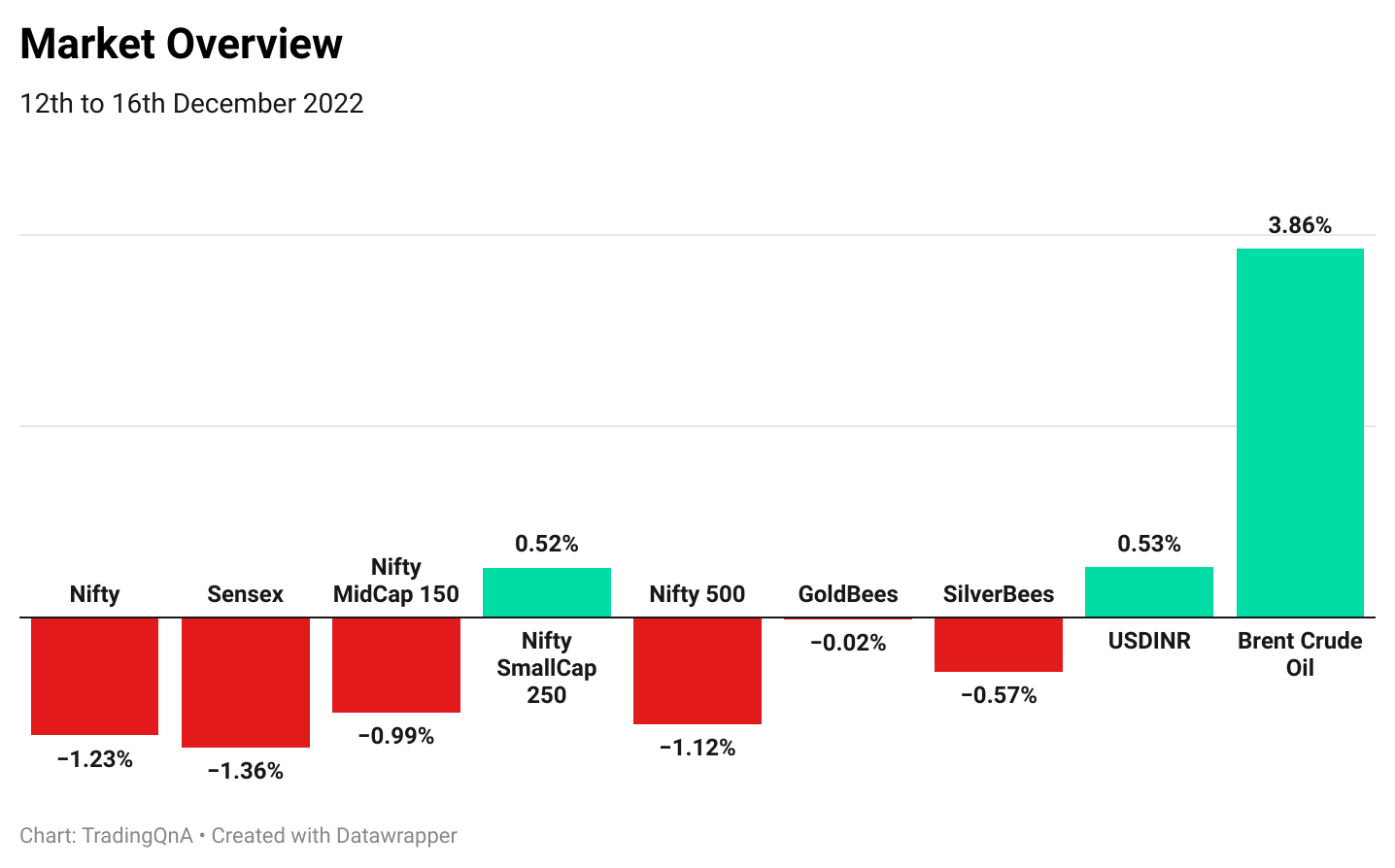

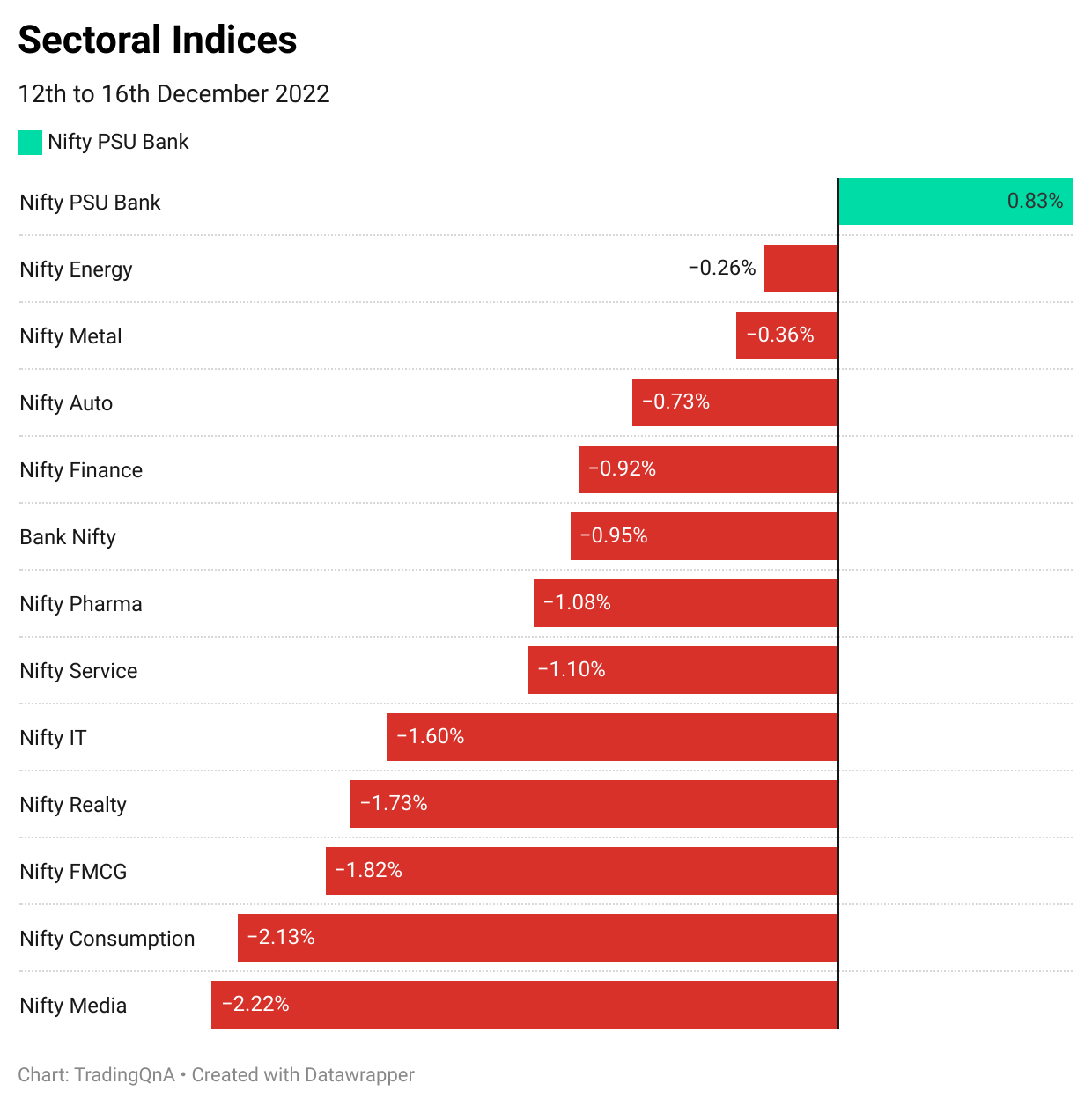

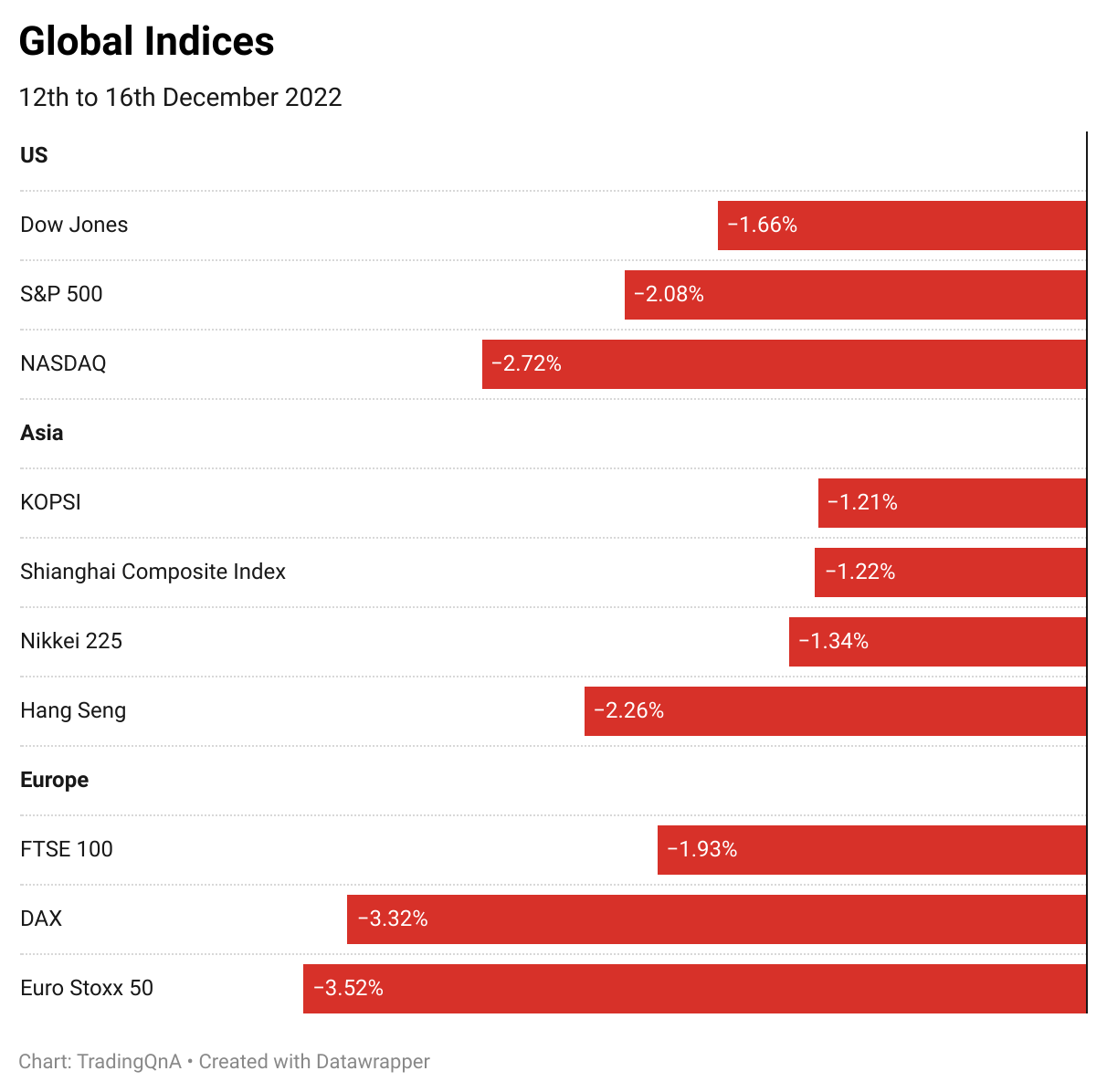

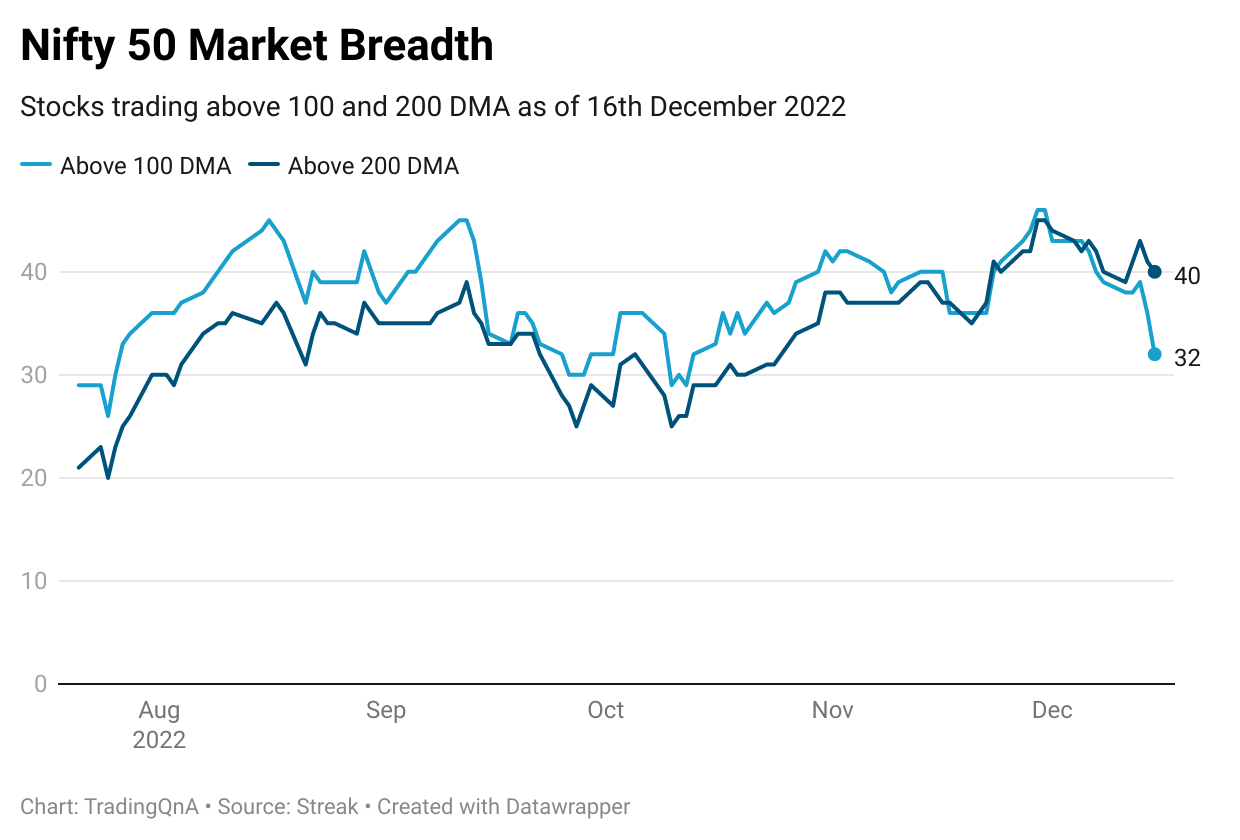

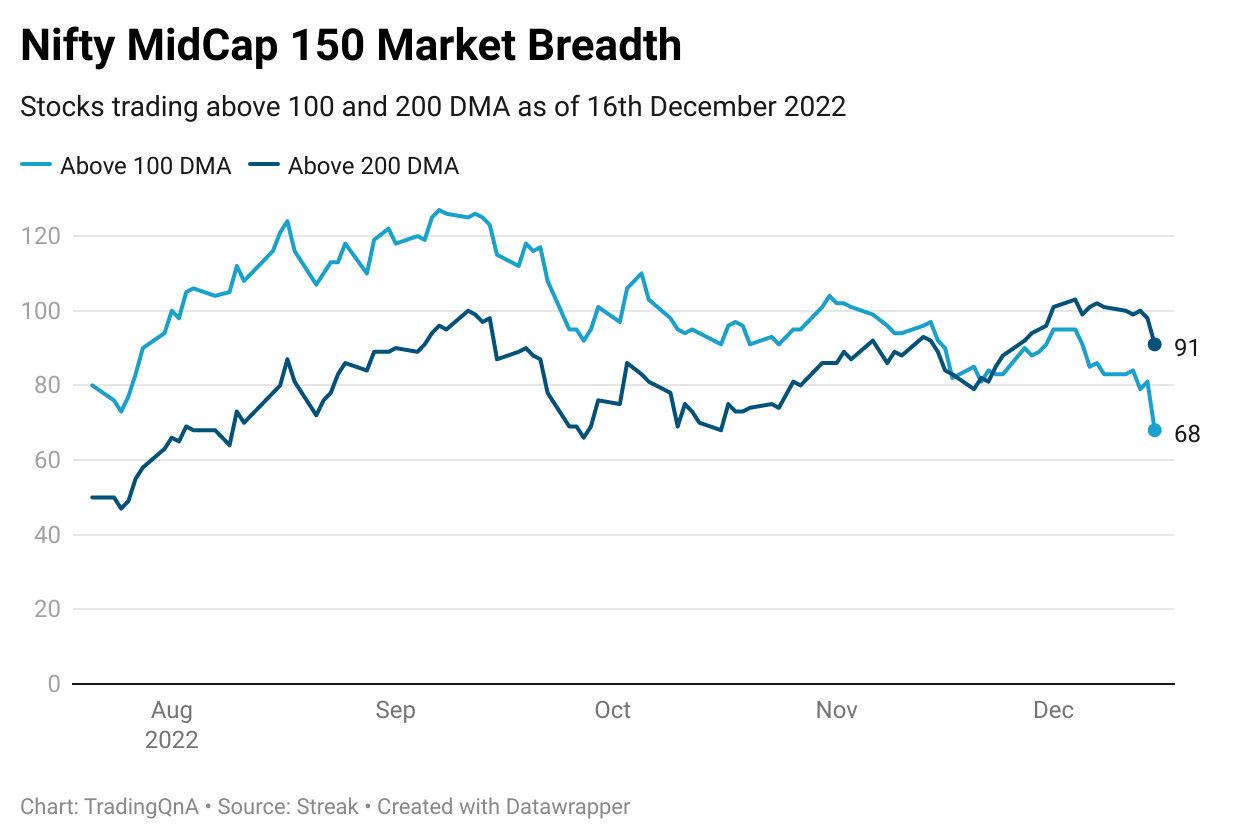

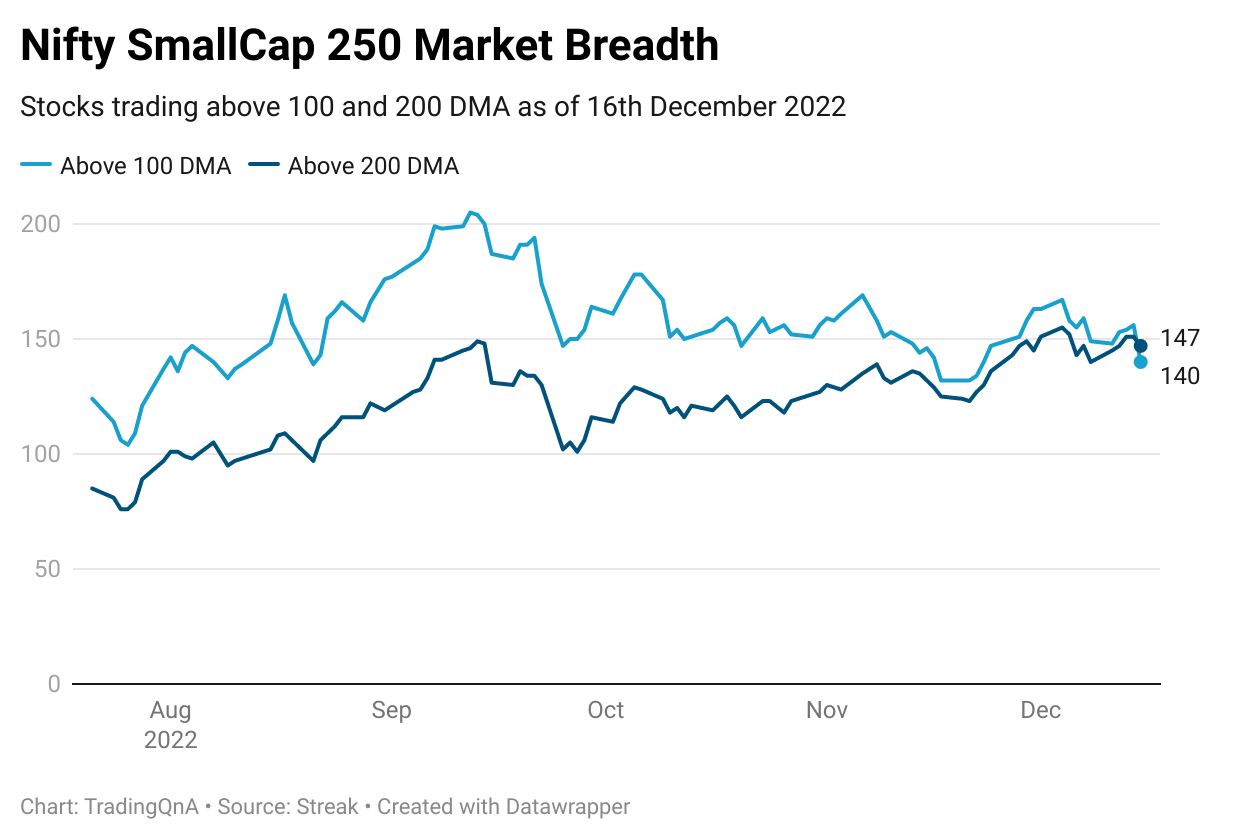

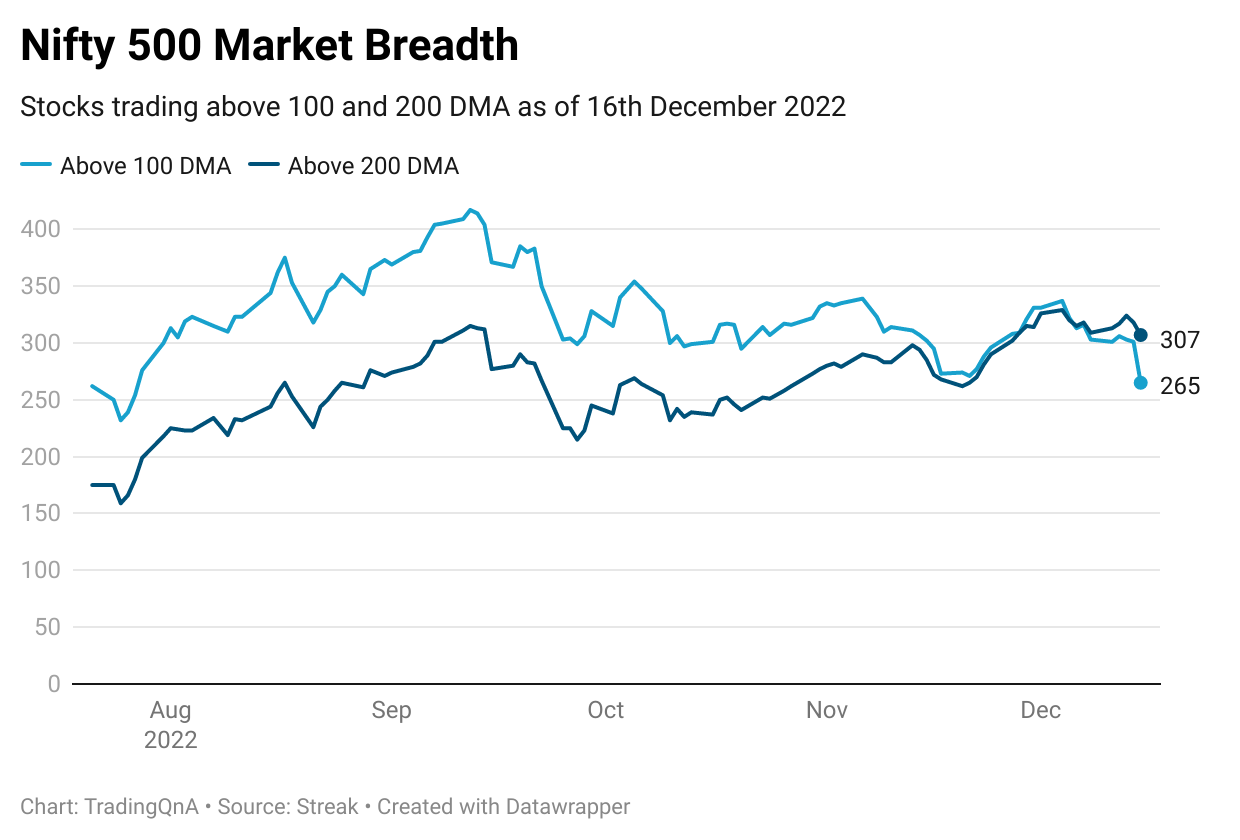

Weekly market wrap

Here’s what the markets were up to in the week ended 16th December;

Bubbles, manias, and frauds

After decades, we’re seeing a sustained rise in interest rates around the world on the back of the dramatic surge in inflation. At a high level, we know the impact of rising interest rates. They lead to higher borrowing costs, reduce demand and impact asset prices. But one of the underappreciated results of rising rates is that they expose all sorts of fraud and speculative business models.

As rates have risen this year, we’ve seen the spectacular implosion of frauds, most notably in crypto, with the FTX bankruptcy being the most recent. We are also slowly seeing VC-backed companies that had poor fundamentals, to begin with go through a lot of turmoil. We’re also seeing sovereign debt crises in countries like Egypt, Pakistan, and Sri Lanka.

So why do we keep seeing these crises?

Hyman Minsky is one of the most underrated economists of the last decade. He made seminal contributions to further the understanding of capitalist economies, the shortcoming of Keynesian policy prescriptions, and the dynamics of financial systems. Perhaps, best known for his Financial Instability Hypothesis (FIH).

It's a brilliant concept that can help us understand how financial markets work and why they are inherently unstable.

Before Minksy, the view held by the likes of Adam Smith was that the economy is an equilibrium-seeking and sustaining system, and some external shock is needed to cause a crisis. But Charles Kindleberger stated that the economy is not an equilibrium-seeking system but a self-sustaining disequilibrating process.

Banks play a crucial role in the economy. They are at the heart of the financial system, where they channel the flow of savings from depositors to borrowers who need money. Minsky said that banks are profit-seeking institutions that make money by lending. But this activity can undermine the stability of the economy. Debt plays a crucial role in determining the system’s behavior, and so Minsky analyses three distinct income-debt relations for economic units.

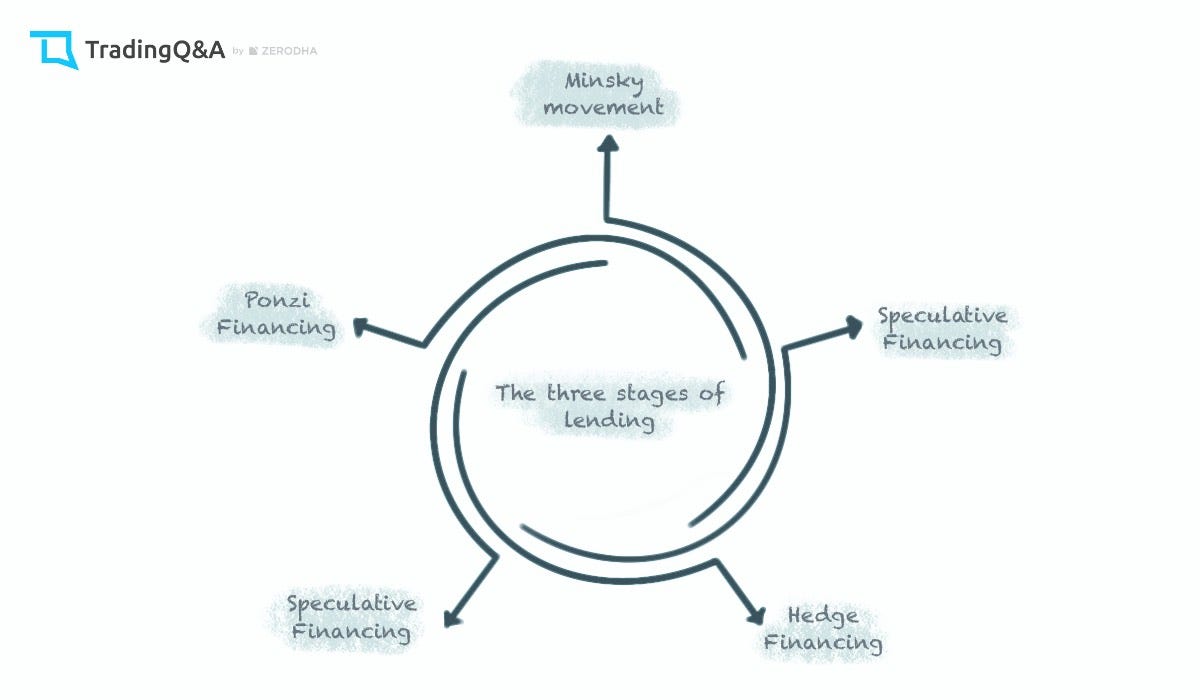

The three stages of lending which Minsky identifies are the Hedge, Speculative and Ponzi stages. You can get a fair idea about what happens in these stages by looking at the image below:

Hedge finance: Borrowers can meet all debt payments (interest and principle) from their cash flows from investment.

Speculative finance: Borrowers can meet their interest payments from investment, but must roll over their debt over to pay back the original loan.

Ponzi finance: Borrowers can neither repay the interest nor the original debt from the original investment, and rely entirely on rising asset prices to allow them continually to refinance their debt.

Despite not coining the term himself, Minsky’s FIH predicts that capitalist economies in the Ponzi stage will experience a ‘Minsky moment’.

It is the moment when the loans issued in the Ponzi stage are recognized to be impossible to pay off. When this realization hits, confidence in the system plummets and people rush to sell assets, which further results in a greater price fall, making paying debts back even harder.

In his book Manias, Panics and Crashes, Kindleberger talks about how markets take the shape of a Ponzi/pyramid scheme. People keep buying in, increasing the prices, and then comes an inflection point when you can't pass the buck, and everything comes tumbling down. This book is a classic account of the life cycle of financial crises.

In his book, Irrational Exuberance, Robert Shiller, the Nobel laureate who predicted the 2008 housing bubble, explains the same with respect to the securities markets. Irrational exuberance refers to investor enthusiasm that drives asset prices higher than those assets' fundamentals justify. The term was popularized by former Fed chairman Alan Greenspan in a 1996 speech.

He argues that people's actions more often depend on stories than hard data and complex formulas. He calls them economic narratives. Prices in large segments of the markets go up based on stories and are totally detached from fundamentals.

The so-called “new-age tech stocks,” thematic ETFs, Special Purpose Acquisition Companies (SPACs), and IPOs are perfect examples of this.

Investors blindly bought into vague and meaningless sales pitches like “disruptive innovation” and “innovation as an asset class.” Another example of a narrative detached from reality was the TAM (total addressable market). VC-Backed companies sold some version of, “India has 125 crore people, and even if we get 1% market share.” Given the last 3 years weren’t just exuberant but downright crazy, VCs funneled billions of dollars into startups that had nothing to show except stories. To be fair, that’s the nature of VC investing, but in a lot of cases, they were throwing good money after bad ideas, terrible and even scammy founders. FTX and Sam Bankman-Fried embody this.

For example, the TAM of handing out free money is infinite, but it's not a business model, right?

Let's say I go to any city center and start handing out 2000 Rupee notes for Rs. 1500. Sounds downright stupid, right? My TAM is the entire population of the city. This enterprise will grow incredibly fast in terms of “customer acquisition,” but the nexus of the transaction is negative. Just like this example, you have to figure out who is selling you these TAM stories just to float shares or pump the stock.

After a decade of free money, things are imploding everywhere.

While talking about a lot of tech stocks, Jim Chanos, the founder of Kynikos Associates and most famous for exposing massive frauds like Enron says;

“This is the inherent insanity of the TAM type stories because we have gone from network effect to negative transaction economics. I do not think that there is any significant critical thinking that is going behind this. Again, it is the unique confluence of Silicon Valley and a need to deploy capital.”

A few years ago, he said that we’re in “the golden age of fraud,” and it was a prescient call.

It seems odd that in an age of information and transparency, there could still be such widespread examples of fraud and wrongdoing in markets. It is interesting to note that frauds and investment bubbles have a lot in common. Click here to find out more.

Why are we always late in detecting fraud? Well, as per Chanos the greatest defense attorney and harshest prosecutor for a company is its stock price. He says, and I am paraphrasing for brevity:

“As long as it is rising, no one cares if you are massaging numbers or committing fraud etc. Once it starts falling, everyone pays attention and is keen to know what's happening. The minute people start losing money in a big way, they begin to basically say, well, it was not my insane levels of leverage nor did I not understand what I was doing when I bought Enron, it is actually the management that are crooks, and they stole from me, and you better do something about this.”

He says that people are going to do crazy things, they do not understand that what they are doing is basically like being in a casino and that even if they are not paying commissions, they need to understand things like bid-ask spreads. But most people won’t care, and they are going to trade themselves into oblivion.

While talking to FT, Chanos describes the current environment as

“a really fertile field for people to play fast and loose with the truth, and for corporate wrongdoers to get away with it for a long time”. He reels off why: a 10-year bull market driven by central bank intervention; a level of retail participation in the markets reminiscent of the end of the dotcom boom; Trumpian “post-truth in politics, where my facts are your fake news”; and Silicon Valley’s “fake it until you make it” culture, which is compounded by Fomo — the fear of missing out. All of this is exacerbated by lax oversight. Financial regulators and law enforcement, he says, “are the financial archaeologists — they will tell you after the company has collapsed what the problem was.”

Why am I telling you this? Simple. Beware. Take care of your money, don't be reckless with it.

Another question is, are we poised for a crisis? Well, If I could answer it with this much accuracy, I would be doing something better than writing this newsletter. But chances are that we may have had a Minsky Moment.

We have seen rising inflation, rising interest rates, and a strong dollar. All of these things lead to rising borrowing costs for new loans, increased repayment costs of dollar-denominated loans, and eventual defaults.

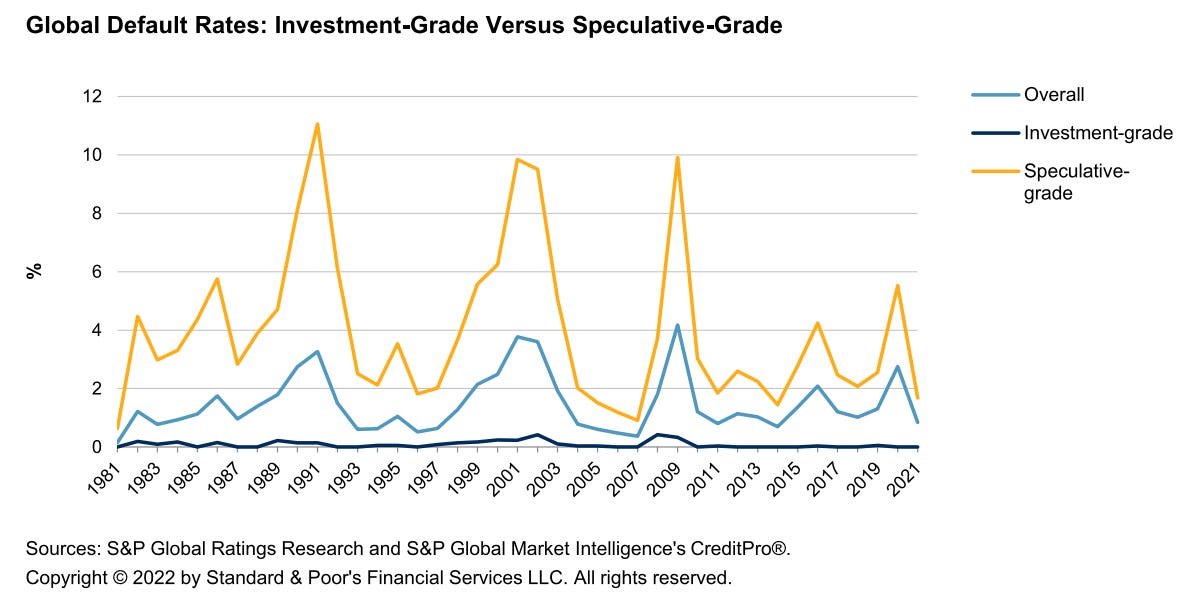

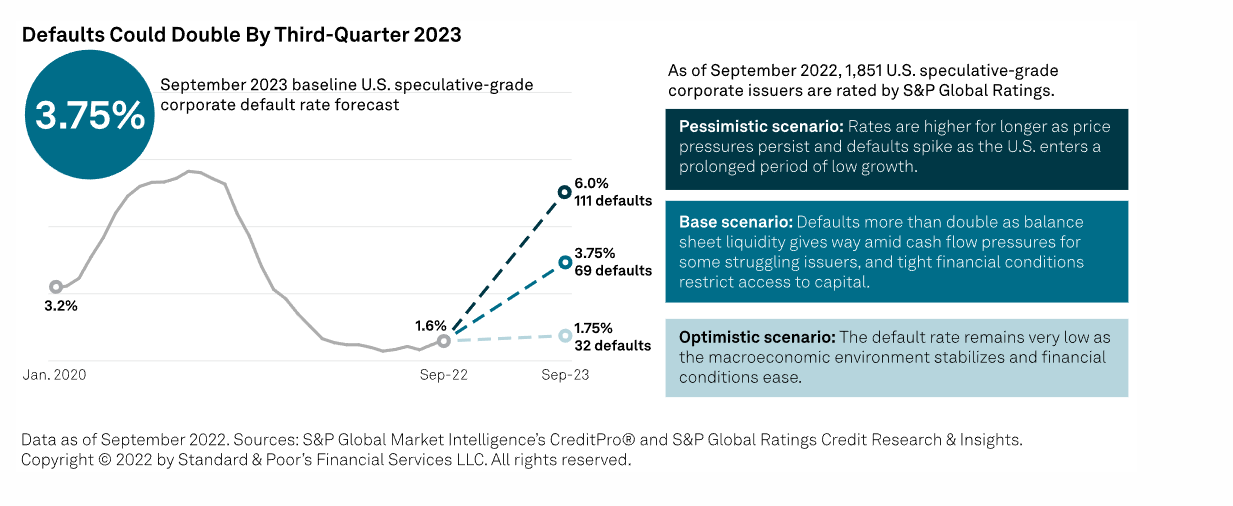

The other area where we could potentially see a lot of blow-ups are companies with high debt or zombie companies. As long as interest rates were low, these companies could keep rolling over their debt and avoid inevitable death. Corporate defaults and bankruptcies were around the words for well over a decade. But if rates continue rising and remain high, this will change.

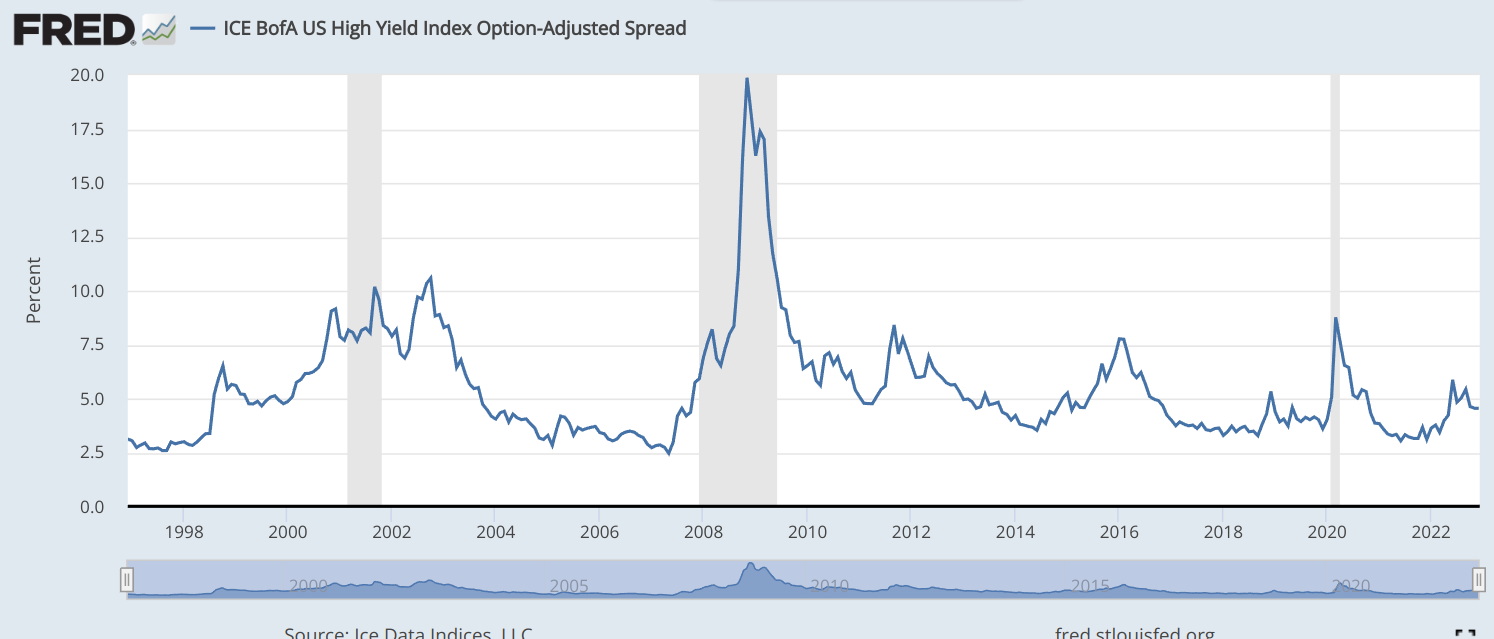

S&P has predicted a base scenario where the U.S. trailing 12-month speculative-grade corporate default rate would reach 3.75% by September 2023, from 1.6% in September 2022.

Take a look at the US High Yield Index Option-Adjusted Spread since 1998. It has been a leading indicator of a downturn in the markets.

If we zoom in and look at this index for the 2020-22 period, we can see momentum is developing for another spike. Could it be a leading indicator for a downturn to follow? Maybe, maybe not, only time will tell.

Takeaways

If something is too good to be true, it always is.

Never invest based on stories—trust, but verify. Scammer the product, better the story.

In bull markets, crowds can become delusional. It’s very important to recognize this tendency and stay away from following the crowd.

— Abhinav and Bhuvan

Planning for longevity risk in retirement

Most people, when they plan for their retirement, they look at the average life expectancy and then assume that's the age they will probably live to. However, averages can be misleading because they conceal the variation of people who do not live to the average life expectancy mark or live past it. When you are making your retirement assumptions, it's always better to be over prepared and save more with the assumption that you might live to be 100 years old or more. It's not really hypothetical because science is getting better all the time. In 1960, the average Indian life expectancy was 40 years, and in 2020 it was 70 years old. Not planning for a long life is called "longevity risk," and most people don't intuitively think about it.

So what does this mean in investing terms? You will have to have a higher equity exposure because equities, in the long run have higher expected returns compared to all the other asset classes like debt, real estate, and gold. But this leads to questions like what stocks, how to pick them, etc.

But there's a much simpler, tax-efficient, evidence-backed, and historically proven way of investing in equities for the long run. In this video, Karthik explains how to think about longevity risk and how to invest to cover that risk.

On TradingQnA

Recently, Franklin Templeton shared a research article on the factors that are going to contribute to India’s growth recovery. Here are some of the interesting charts and other highlights from the same… 👇

Ready for India’s growth recovery: Powered by domestic demand

In the last 2-3 years, there was a mania around IPOs. A lot of people thought of them as guaranteed moneymakers. The news headlines of IPOs going up 100–200% are enough to induce greed. But do IPOs “always” make money? A look at the performance of IPOs in recent years… 👇

Performance of IPOs from 2020-2023

🐦 On Twitter

📖 Reading Recommendations

Mirror, Mirror on the Wall, Who Knew That Stocks Would Fall?

Countless hunches and gut feelings flicker through our consciousness over the course of a year. We naturally remember the ones that turn out to be right. The multitude of other hunches that turn out to be wrong go into our mental garbage can.

Looking back at yourself a year ago, what you know now has indelibly altered your perception of what you knew then.

This pattern, which psychologists call hindsight bias, makes us feel that we foresaw the future all along, what happened was inevitable and anybody who didn’t see it coming is a dope. It’s close to irresistible—and it’s an illusion.

Continue reading…

The End of Blitzscaling

Blitzscaling worked well for the better part of a decade. In fact, it worked so well that it was largely responsible for creating hundreds of unicorns. The trouble, as we now know with hindsight, was that this phenomenon was fleeting in many cases and largely the result of low interest rates and easy access to capital.

The result?

A trend that, as it always has been, was unsustainable.

Continue reading…

Some Thoughts About Investing

The fear of missing out and the joy of missing out are two sides of the same coin. In bull markets, you feel like an idiot for not going all-in on the highest of high fliers.

In bear markets, that FOMO quickly turns into JOMO (the joy of missing out).

Continue reading…

🎧 Listen to

— Curated by Shubham

Thank you for reading. do like and share this with your friends and let us know your views in the comments section below.

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna