Importance of economics in daily life, World Economic Outlook, Savings, Poverty, Pandemic and more

#Issue 25

This is the latest issue of Markets and Macros by TradingQnA written by Abhinav and Shubham.

Weekly market wrap

Why everyone should know a little economics

Most of us don’t think about it this way, but our everyday lives are affected by what happens in the economy. For example, inflation might seem like an abstract thing, but when inflation rises, our cost of living rises too. But the tragedy is that most of us think that economics is too hard to understand.

There’s some truth to the idea because most economists make a lot of things technical and complicated when there is no need. Having said that, at its core, economics is simple, and you don’t need an MBA or PhD to understand the key concepts that will affect the economy at large and your life as well.

Ha-Joon Chang has spent his entire life railing against the flaws of classical economics. He recently wrote a brilliant piece summarising how economics went wrong why it's important that we understand the basics of economics

“Like it or not, economics has become the language of power. You cannot change the world without understanding it. In fact, I think that, in a capitalist economy, democracy cannot function effectively without all citizens understanding at least some economics. These days, with the dominance of market-oriented economics, even decisions about non-economic issues (such as health, education, literature or the arts) are dominated by economic logic.

When so many collective decisions are formulated and justified with the help of the dominant economic theory, you don’t really know what you are voting for or against, if you don’t understand at least some economics.

Economics is not like studying, say, the Norse language or trying to identify Earth-like planets hundreds of light-years away. Economics has a direct and massive impact on our lives.”

World economic outlook

The World Economic Outlook 2023 was just published, aptly titled “A Rocky Recovery”.

Here’s the TLDR:

Despite facing the pandemic and Russia's invasion of Ukraine, the global economy is showing signs of a steady recovery.

China has fully reopened and is showing signs of an economic rebound.

The supply chain disruptions are gradually easing up and the energy and food markets, which were impacted by the war, are stabilising.

The tightening of monetary policies by central banks is bearing fruit and is expected to help control inflation and bring it back in line with targets.

India’s GDP growth forecast for FY25 has been cut to 6.3%. Despite this cut, India is poised to be the fastest growing economy over the next two years.

Major Highlights

Growth and inflation

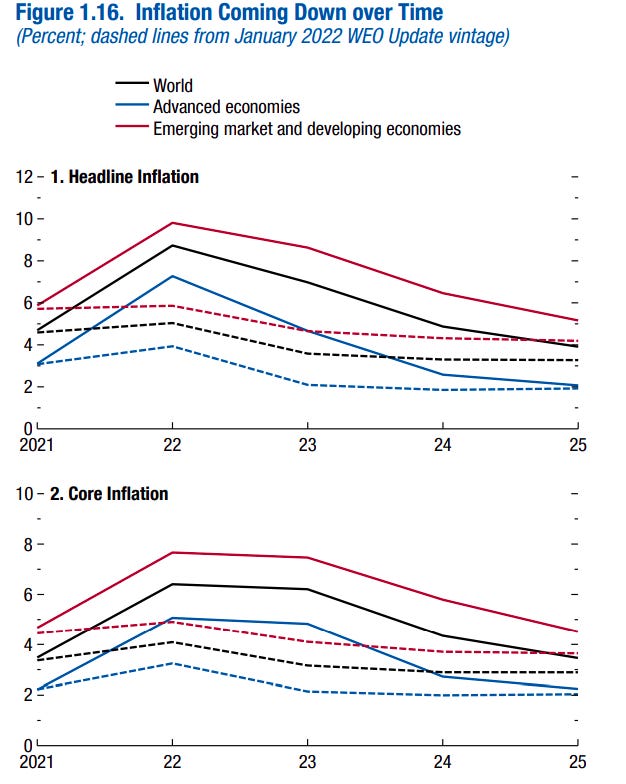

This time the economic slowdown is more pronounced in advanced economies and inflation is falling slower than anticipated.

Inflation has been sticky as discussed in an earlier newsletter. Global headline inflation is set to fall from 8.7% in 2022 to 7% in 2023 due to lower commodity prices, but core inflation is likely to decline more slowly.

Many countries have not reached their core inflation peak yet. Core inflation is likely to slow down to 5.1% this year, which is a significant upward revision of 0.6 % points from the previous update in January.

This is a cause for concern as it is well above the target inflation rate. Inflation’s return to target is unlikely before 2025 in most cases.

Employment

Economic activity is showing resilience as labour markets in most advanced economies remain robust (I had written about this in the American context in a previous newsletter).

As central banks tightened monetary policy, the IMF expected to see a slowdown in output and employment growth. But in the last two quarters, the estimates for output and inflation have been adjusted upwards, indicating stronger than expected aggregate demand. There is a possibility that monetary policy might need some more tightening for a longer period than previously anticipated.

But what about real wages (real wages are wages adjusted for inflation, or, equivalently, wages in terms of the amount of goods and services that can be bought.)? The increase in prices is outpacing nominal wage gains, resulting in a decline in real wages. Since the demand remains strong it is likely that real wages will also increase soon. Can it lead to a wage-price spiral? The IMF does not think so.

Monetary tightening and financial instability

Last year’s rapid monetary policy tightening raised funding costs, triggered losses on long-term bonds, hitting banks’ bottom line.

Remember SVB? I had written about it here.

What is the possible impact of this?

To quote from the WEO

“The baseline forecast, which assumes that the recent financial sector stresses are contained, is for growth to fall from 3.4% in 2022 to 2.8% in 2023, before rising slowly and settling at 3%

five years out––the lowest medium-term forecast in decades. Advanced economies are expected to see an especially pronounced growth slowdown, from 2.7% in 2022 to 1.3% in 2023. In a plausible alternative scenario with further financial sector stress, global growth declines to about 2.5% in 2023 with advanced economy growth falling below 1%.”

As per the WEO, the potential risks to the economic outlook are skewed towards the downside with the possibility of a hard landing having increased significantly. This could lead to stress in the financial sector which could weaken the economy.

Additionally, there could be some problems with sovereign debt distress, which could worsen in the face of higher borrowing costs and lower growth. For more on sovereign debt default, refer to our previous newsletter.

Slowbalisation

The WEO exposed me to this new word slowbalization— a slowdown in globalisation. This is not a new phenomenon, and for most countries it dates back to the GFC. Global FDI has declined from 3.3% of GDP in the 2000s to 1.3% between 2018 and 2022. There are a range of factors contributing to this but the fragmentation of capital flows along geopolitical fault lines and the potential emergence of regional geopolitical blocs are new factors that the WEO talks about.

To make supply chains less susceptible to geopolitical conflicts companies and governments are becoming more interested in plans to relocate production processes to countries they can trust and have similar political views with.

India

In January, the IMF had predicted India’s GDP to grow 6.1% in FY24 and 6.8% in FY25 but now the forecast for FY25 has been cut to 6.3%. Despite this cut, India is poised to be the fastest growing economy over the next two years.

The IMF projects India’s inflation to slow to 4.9% in the current year and further to 4.4% next fiscal year.

Poverty and the Pandemic

I came across this interesting debate around poverty.

A Pew research report suggested that the middle class may have shrunk by 30% and the number of poor rose by 7.5 crore during the pandemic. The report uses World Bank projections of economic growth to estimate the impact of COVID-19 on Indian incomes. The report further states

“The methodology in this analysis assumes that incomes change at the same rate for all people. If the COVID-19 recession has worsened inequality, the increase in the number of poor is likely greater than estimated in this analysis, and the decrease in the number who are high income is likely less than estimated. The middle class may have shrunk by more than projected”.

But now a paper written by Arvind Panagariya, former Vice Chairman of Niti Aayog, and Vishal More contradicts this. This paper concludes that

“claims of massive increases in poverty and inequality during COVID-19 are patently false. On an annual basis, poverty continued to fall in rural areas during the Covid year of 2019-20 albeit at a significantly lower rate. Rural poverty saw the same sharp decline in 2020-21 as in the pre-Covid year of 2018-19”

It accepted that there was some increase in urban poverty though. This paper relied on the Periodic Labour Force Survey (PLFS) data to come to this conclusion.

So who is right?

Himanshu, writing for the Indian express, says that the paper makes this claim based on data on consumption expenditure collected as part of the PLFS conducted from 2017-18 onwards. To their credit, he says, they are right in pointing out the superiority and credibility of publicly available data with “benefit of scrutiny and oversight by scholars and statisticians” as against privately collected data.

More support poured in from former CEA Dr krishnamurthy Subramanian

https://twitter.com/SubramanianKri/status/1646326834290622465?s=20

But there is a problem here. Poverty estimates in India have always been based on consumption estimates from the NSO, particularly based on the consumption expenditure surveys (CES), but this was jettisoned by the government in 2017-18. Although the PLFS also collects some consumption aggregates, these estimates of poverty are not comparable with those from the CES due to the different levels of detail in which consumption expenditure data is collected by these two surveys.

“This issue of sensitivity to the details of questions asked to collect consumption expenditure is not just relevant across different surveys but also across different rounds of the PLFS. While the annual PLFS had a single question to elicit information on consumption expenditure between 2017-18 and 2019-20, in 2020-21 the number of questions was increased to six, along with detailed instructions being given in the questionnaire itself. This change in questionnaire design makes the PLFS estimates of consumption expenditure before 2020-21 non-comparable with those after.”

So what happened to poverty during the pandemic? Well, I am as confused as you are. Know one really seems to know.

I am no academic expert but to me Independent data from multiple sources on wages, incomes and consumption of durables seems to confirm the distress in the economy, especially during the pandemic years.

India and savings

Let's talk about how India saves. First we must understand basic things about how Indian households save and what factors determine savings.

This paper by Somya Kanti Ghosh, chief economist SBI, concludes that real per capita income — or earnings on an inflation-adjusted basis — and access to banking facilities are the most important determinants of savings in India. Some important things that I noted in this paper are

A 1% increase in per capita income leads to a 0.37% increase in the private saving rate in the long run.

A 1% increase in inflation led to a 1.23% decrease in private saving rate in the long run.

Bank density — the number of available banks per person — has an inverse correlation with savings.

Based on these, this paper concludes that macroeconomic policies aimed at boosting productivity, lowering inflation and increasing real income could help elevate the savings rate in India. Moreover, policies facilitating the “proliferation of banking” would help mobilise savings.

Why are we discussing savings?

Savings are important as they can provide resources for investments in the economy. By putting money into investments that can increase its value, individuals contribute to the generation of wealth, which ultimately leads to the betterment of the lives of a larger population.

I came across this article and learnt that India’s savings rate exceeds the UK, US, Brazil’s (the savings rate peaked at 36.91% in 2010-11. In 2021-22 it was 30.2%). The major challenge now though is to channel these savings to investments.

As per the Indian household savings landscape report a large fraction of the wealth of Indian households is in the form of physical assets.

“In India, the average household holds 77% of its total assets in real estate, 7% in other durable goods (such as transportation vehicles, livestock and poultry, agricultural machinery and non-farm business equipment), 11% in gold and the residual 5% in financial assets (such as deposits and savings accounts, publicly traded shares, mutual funds, life insurance and retirement accounts).”

This is in contrast to developed economies, where households hold a substantial portion of their wealth in financial assets.

Insurance and pension penetration are also low by international standards. Pension funds’ assets are less than 2% of GDP. The life and non-life insurance premium income formed 2.82% and 0.94% of GDP respectively in 2019. This is low compared to the global average of 3.35% and 3.88% respectively.

But things are changing. Over the past few years, financial savings have been witnessing a compositional shift with more households diversifying their portfolio and shifting away from traditional instruments such as bank deposits. The last year saw profound changes in the savings and investment pattern of households.

There has been a shift in the composition of gross financial savings over the past decade. In 2011-12, bank deposits dominated household financial savings, contributing more than half of it. For the year ending March 2022, bank deposits constituted roughly one fourth of the households’ financial savings.

The contribution of provident and pension funds has risen over the last decade. In 2011-12, provident and pension funds accounted for 10% of the financial savings. Last year, the share had risen to more than 22%, indicating greater move towards a formalised economy. They had the second highest share in 2021-22. These were followed by life insurance funds and small savings.

There has also been an increase in the share of mutual funds and equity in households’ financial savings, particularly in 2021-22. The share of mutual funds (MF) in households’ financial savings stood at 6.3%, a more than 4% rise from 2020-21. Direct exposure to equity instruments has also seen a sustained rise. From a meagre 0.28% share in FY 2018-19, the share of equity instruments has risen to 1.9% in 2021-22.

What does all this mean? Simply put, as more and more savings are channelled into financial assets they can be mobilised for investments and contribute to India’s growth story.

Insights on housing finance

HDFC Securities shared a comprehensive research report on the Indian home loan market and my colleague Meher has posted some of the key themes and highlights from it on TQ&A.

Listen to

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna

Thanks for reading Markets and Macros by TradingQnA! Subscribe for free to receive new posts and support my work.