Conflicts to watch in 2023, revival of PSBs, emergence of new world energy order and more...

Issue #19

Hello all, welcome to the latest issue of Markets and Macros by TradingQnA.

You can listen to the audio summary of this issue below 👇

Investing is easy but not simple

There’s no grand secret to investing. All you have to do is invest regularly, have a diversified portfolio and be disciplined. Despite this being obvious, very few people are successful at investing.

Why?

Jack Raines in this timely piece at the beginning of the year and the end of the longest bull market in history puts it succinctly:

“Investing is hard because the risk-adjusted way to win is to index and chill while someone, somewhere, hits the lottery every single day.”

10 conflicts to watch out for in 2023

We are still reeling from the effects of the ongoing Russia-Ukraine war but every day we see less coverage of it. That's how our attention spans work, sad but true.

Saying that the invasion was unthinkable in the 21st century is one thing but saying that you never saw it coming would be a stretch. The writings were on the wall for quite some time. Was it the only conflict that one could see coming? No. It was the one which grabbed the most eyeballs.

2022 proved that warfare is back in fashion. So, will 2023 see major powers go to war or break a nearly 80-year nuclear taboo? Will political crises, economic hardship, and climate breakdown cause a social meltdown in not just individual countries but a swath of the world? Worst-case answers to this year’s big questions seem far-fetched. But after the past few years, it would be complacent to dismiss the unthinkable.

Foreign Policy has compiled a list of 10 conflicts to watch out for in 2023.

Public Sector Banks

The public sector banks (PSBs) seem to have turned the corner in the past year. SBI is up more than 30%, while Punjab National Bank is up almost 50%. Others like the Bank of Baroda and UCO Bank have more than doubled. While private sector bank stocks have also seen a sharp rise – Axis is up almost 35%, while ICICI is up 17% — public sector banks have outperformed their private counterparts by a significant margin.

The Nifty PSU bank index is up over 54% in the past year, while in comparison, the private bank index is up around 11%.

Why has this happened?

We had covered this earlier in a previous newsletter. One explanation is that the performance of PSBs is in part due to the resolution of non-performing loans, write-offs, sales to asset reconstruction companies, and recapitalization.

PSBs have been on a multi-year drive to clean up their balance sheets and shore up capital. While there are still some concerns over possible slippages from accounts that were restructured during the pandemic, gross non-performing assets (NPAs) or bad loans were down to 6.5% at the end of September 2022. Lending is growing at a brisk pace and banks’ spreads also have improved with the interest rate cycle on the upswing.

Well, this seems like good news but have you ever stopped to think why the NPA problem was rampant in the PSBs to begin with?

Sucheta Dalal shares her insight on the corporate bad loan problem. She uncovers reasons like dubious lending, diversion of funds, meaningless guarantees, and staff accountability. Below is a small extract from this piece:

“The defaults date back to 2013-14 or earlier and had already gone through a loan restructuring process involving significant concessions from the lender. Forensic audits are invariably commissioned just before filing bankruptcy proceedings and have invariably revealed massive diversion of funds, and, in many cases, outright fraud.

The documents put to the Wilful Defaulter Committee fail to answer the most obvious questions that comes to mind: Why wasn't the use of funds better monitored and why were forensic audits not ordered before restructuring loans? The answer lies in what the late Dr KC Chakrabarty, former deputy governor of the RBI, used to tell us. He said, by the time a bank gets around to declare a company a wilful defaulter, there is nothing much left to recover—not even the guarantees collected at the time of disbursing multiple loans.

Indian banks, especially PSBs, have poor processes for monitoring the use of funds and the guarantee process is downright dubious.”

Is a new world energy order taking shape?

For the last 70 years, we have been witness to one of the most important political alliances between Saudi Arabia and the USA in which US security in the Middle East was bartered for oil pegged in dollars. But times change, and 2023 may be remembered as the year that this grand bargain began to shift, as a new world energy order between China and the Middle East took shape.

China has for some time been buying increasing amounts of oil and liquefied natural gas from Iran, Venezuela, Russia, and parts of Africa in its own currency, President Xi Jinping’s meeting with Saudi and Gulf Co-operation Council leaders in December marked “the birth of the petroyuan”, as Credit Suisse analyst Zoltan Pozsar put it in a note to clients.

According to Pozsar

“China wants to rewrite the rules of the global energy market, as part of a larger effort to de-dollarise the so-called Bric countries of Brazil, Russia, India and China, and many other parts of the world after the weaponisation of dollar foreign exchange reserves following Russia’s invasion of Ukraine.

What does that mean in practice? For starters, a lot more oil trade will be done in renminbi. Xi announced that, over the next three to five years, China would not only dramatically increase imports from GCC countries, but work towards all-dimensional energy co-operation”.

This could potentially involve joint exploration and production in places such as the South China Sea, as well as investments in refineries, chemicals, and plastics. Beijing’s hope is that all of it will be paid for in renminbi, on the Shanghai Petroleum and Natural Gas Exchange, as early as 2025.

Financial Times has an interesting take on this potential new energy order. We have also been speaking about this topic in our previous newsletter and have also discussed this in brief in our podcast with Debashish Bose.

But there are others like Brad Setser who claim that we are far away from a reorder of the global power dynamics and that the new energy/world order or the demise of the petrodollar is still far away.

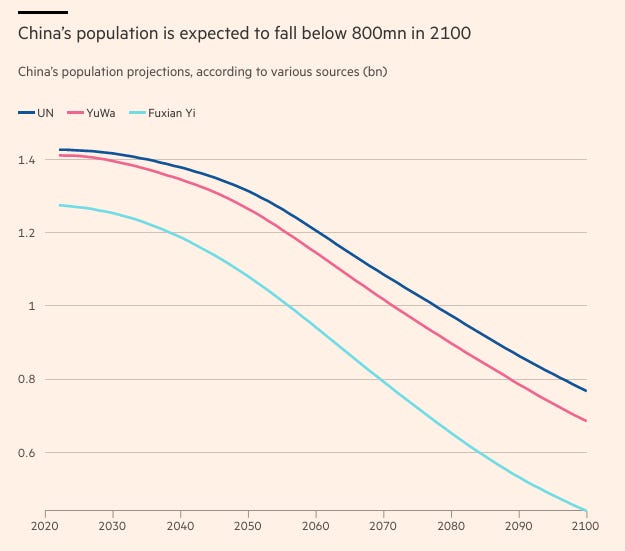

India will become the world’s most populous country in 2023

The United Nations estimates that India’s population will surpass that of China on April 14th. India’s population on the following day is projected to be 1,425,775,850.

India is expected to provide more than a sixth of the increase of the world’s population of working age (15-64) between now and 2050. China’s population, by contrast, is poised for a steep decline. The number of Chinese people of working age peaked a decade ago. By 2050 the country’s median age will be 51, 12 years higher than what it is now.

What does it mean for India?

With a median age of 28 and a growing working-age population, India now has a chance to reap its own demographic dividend. But India’s prosperity depends on the productivity of its youthful people, which is not as high as in China. Fewer than half of adult Indians are in the workforce, compared with two-thirds in China. Chinese aged 25 and older have on average 1.5 years more schooling than Indians of the same age.

So the question now is, will we reap a demographic dividend or is it possible that it will turn into a demographic nightmare? Devender Singh believes that our demographic dividend may be withering away!

What does it mean for China?

Source: Financial Times.

China’s one-child policy did pay its dividends. China’s economic miracle was in part the result of the rising ratio of working-age adults to children and elderly from the 1970s to the early 2000s. With fewer mouths to feed, parents could invest more in each child than they otherwise would have.

But the same policy which contributed to China’s economic boom is starting to show its side effects. As this FT article covers;

Over the next five years, the first cohort of people who became parents during the “one-child policy” era that began in 1980 will increasingly advance from their 60s and 70s — or what sociologists describe as being “young-old” — into their 80s.

This growing group of “old-old”, with a higher likelihood of developing costly chronic diseases, would make greater care demands both on their children and the state.

Local governments are already struggling to meet the rising cost of health and social care. Their spending on China’s sprawling zero-Covid infrastructure has ballooned, while tax receipts from the battered property sector have plummeted.

“If this continues, how can China sustain the pension payments for this enlarging elderly population?”

Around the web

Reading Recommendations

We Will See the Return of Capital Investment on a Massive Scale

Market strategist and historian Russell Napier warns of a 15- to 20-year phase of structurally elevated inflation and financial repression. He shares his views on how investors should prepare for this new world.

In an in-depth conversation with The Market NZZ, he explains why most developed economies are undergoing a fundamental shift and why the system most investors have become accustomed to over the past 40 years is no longer valid.

Continue reading…

The Inside Game

In a bubble, there are two games being played, an outside game and an inside game.

The outside game is the sermon of the true believer. You hear the outside game on podcasts, YouTube, Twitter, and from that wacky friend from college. The message will sound radical, almost too crazy to believe, but just take a moment to hear it out. Disruption. Innovation. A new paradigm. Everything is changing - what matters today will be worthless tomorrow.

The inside game is a bit more complicated. The inside game recognizes and exploits a zero-sum game of social contagion. The asset in question - and any concept of valuation - is irrelevant. What matters is how much hype you can generate and how many new outsiders you can lure. The essential tools are human emotions: greed, jealousy, and fear (of missing out).

Listen to

Thank you for reading. do like and share this with your friends and let us know your views in the comments section below.

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna