Hangover after a 14-year party

Issue #13

Hello all, welcome to the latest issue of Markets and Macros by TradingQnA. In this week’s issue, we discuss;

Ashwath Damodaran on the impact of the Fed, QE, QT, and inflation on valuations

The future of energy transition and more…

Hindi: इस पोस्ट को हिंदी में पढ़ने के लिए यहाँ क्लिक करें।

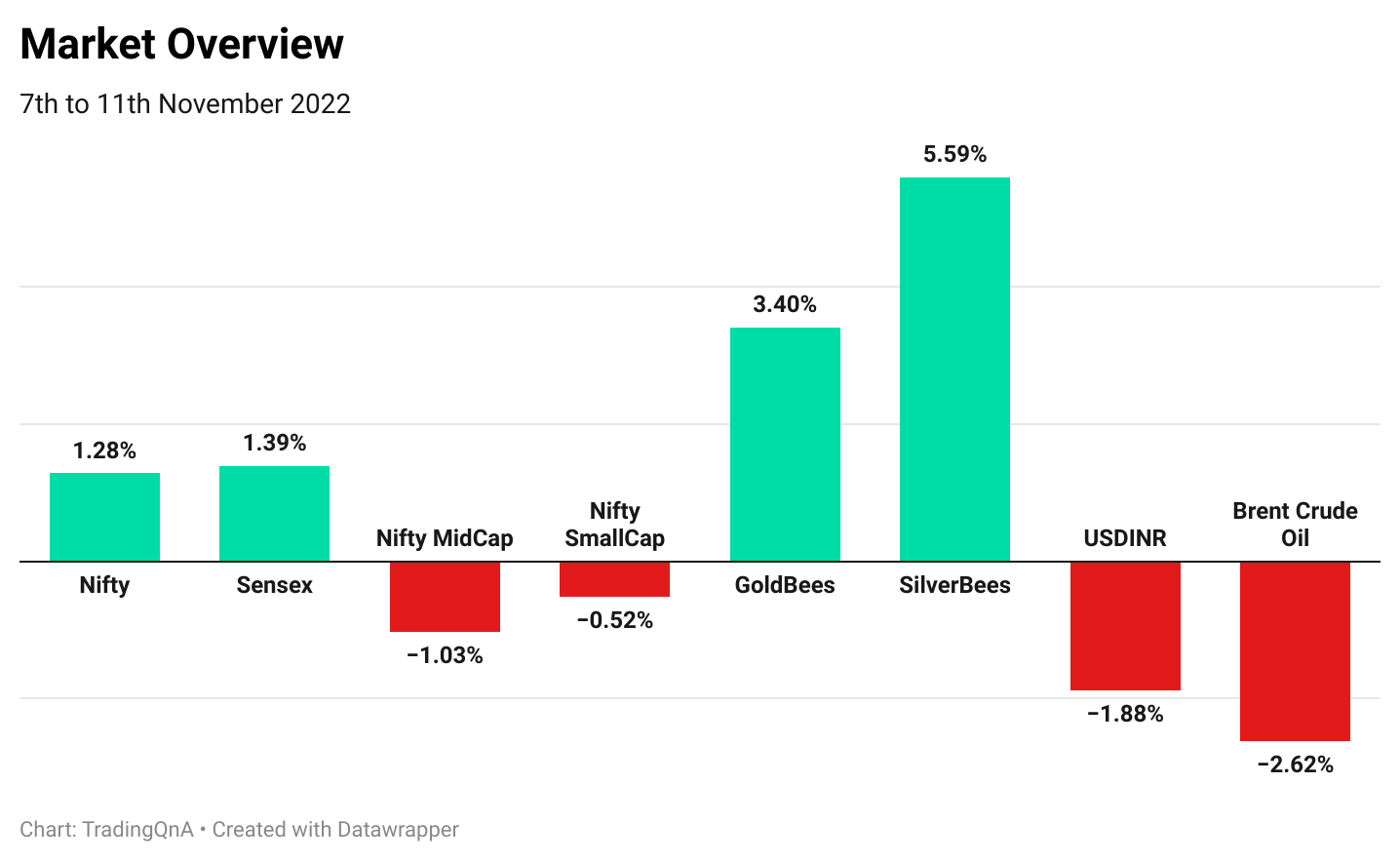

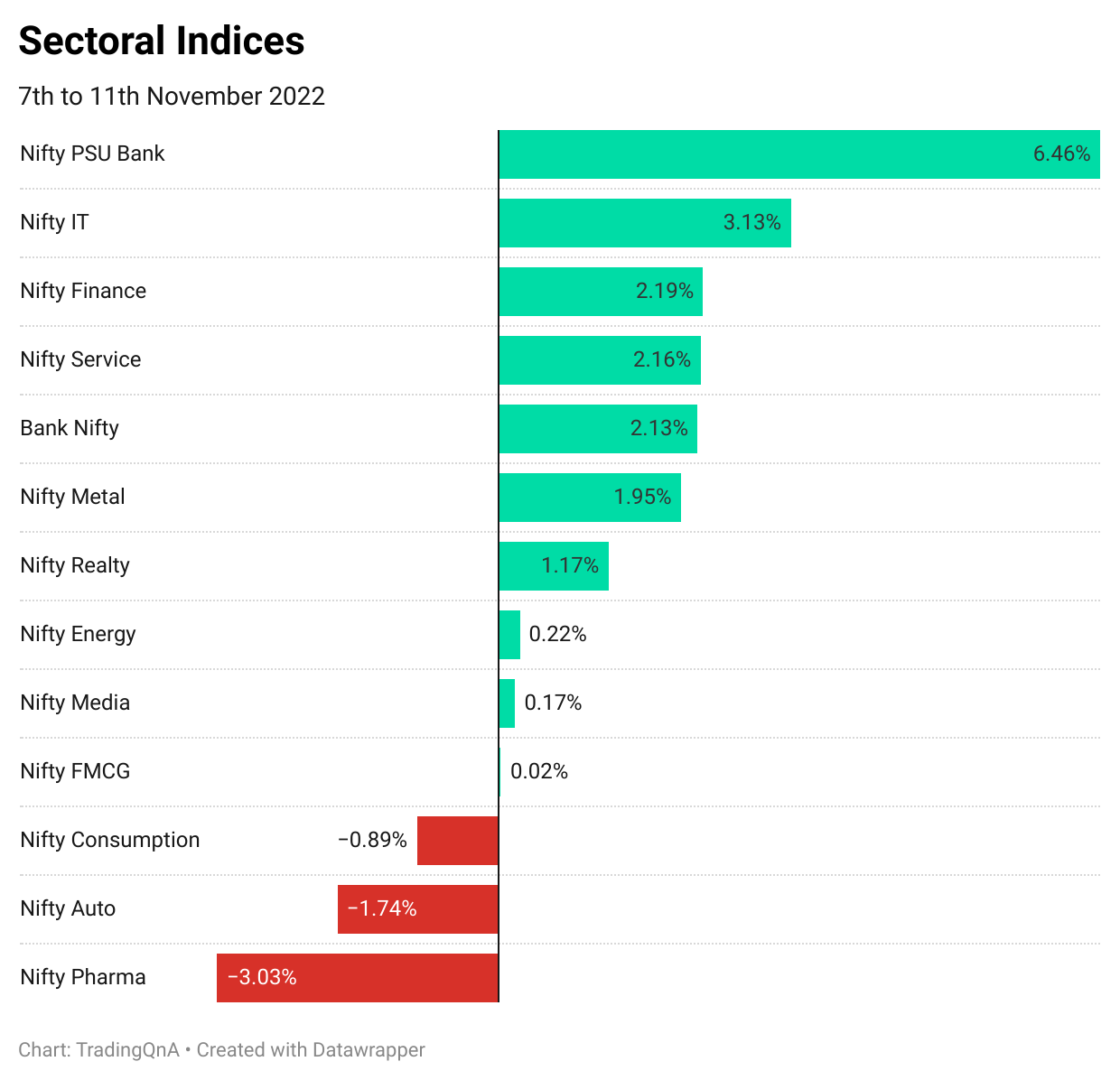

Weekly Market-wrap

Ashwath Damodaran on the impact of the Fed, QE, QT, and inflation on valuations and more

Professor Aswath Damodaran is often called the dean of valuations. He’s one of the sanest and most insightful voices on finance. He was recently on The Blockworks podcast and as usual, the conversation was filled with insights.

A few interesting titbits from the conversation:

What is the Sleep Test for investments?

If your portfolio doesn't allow you to sleep at night, you are doing something wrong. If you are worried about the fluctuations, then you are taking more risks than you can handle. Your portfolio performance should not dictate your lifestyle choices.

How does inflation impact asset prices?

Inflation drove up stocks over the last year. When inflation is unexpectedly high, any fixed-income security is going to lose value and people will turn to alternatives.

Unpredictable inflation is a bigger problem than high inflation. For eg: compare two economies, one with 7% fixed inflation and the other currently at 2% inflation which wavers from 5% to -2% a year. Running a business and investing in the markets in the first economy is far easier than in the second.

What is an equity risk premium?

The equity risk premium is the extra return that investors demand over and above a risk-free rate to invest in equities as a class. Thus, it is a receptacle for investor hopes and fears, with the number rising when the fear quotient dominates the hope quotient. In buoyant times, when investors are not fazed by risk and hope is the dominant force, equity risk premiums can fall. He has written in detail on the topic here.

The risk premium is the price that you demand to take on risk as an investor. It is person-specific depending on risk appetite.

There is a misconception that you can calculate risk premiums by looking at history. This is wrong for two reasons:

It’s backward-looking when trying to find a forward-looking number and

It’s static. One could be in the middle of the worst crisis in history and look backward to say that nothing’s wrong!

Prof. Damodaran has devised a different way of estimating it: A forward-looking dynamic premium.

Impact of interest rates on stock prices

Be careful when market gurus say, “interest rates are going up, therefore stock prices should go down”. You need to ask, why are interest rates going up?

There can be different consequences for value investing depending on whether they’re going up because the economy is doing well, inflation is increasing, or just because there’s some perception in the market that's pushing them up.

See the chart below, rates and stocks were both rising in phases 1 and 2. The basic “interest rates are going up, therefore stock prices should go down” mantra was only valid for phase 3.

Why are companies down 70-90%, especially the ones that went public in the period of excess liquidity (2020-2021)?

Many of these companies need capital just to keep going. They need huge amounts of new capital to be able to survive, forget about growth. With a downswing in the market, risk capital goes to the sidelines. Risk capital includes not just people investing in riskier stocks, but also VC money.

For these young companies, two things have happened:

Expectations have finally caught up with reality.

People are worried whether they will survive till risk capital comes back.

On Commodity and Energy Stocks

Commodity prices cannot be forecasted. It’s hubris to forecast prices in the face of so much macro uncertainty.

Commodity companies are susceptible to commodity prices. It doesn't make them good or bad investments, it just means as standalone investments they’re very risky.

The advantage of commodity stocks in a portfolio is that sometimes the forces that make them do well are the forces that make the rest of the market do badly. This year is a perfect example.

Fed, QE, QT, and impact on valuations

“We had a 14-year party and it’s time for the hangover.” This is what he had to say about rising interest rates and tightening financial conditions. Although he believes, central banks have a marginal impact on valuations and the effect of quantitive easing (QE) over the last 14 years was much milder than we all think, and it's also far lesser than inflation.

The Fed has been a player, but it hasn’t been the main player in the game in good ways or bad ways.

By worrying so much about what the Federal Open Market Committee(FOMC) is thinking and overanalyzing Jerome Powell's every word, we're getting distracted from looking at the true macroeconomic variables that drive value.

We overestimate the power that central banks have, and I think we do it because it makes us feel more comfortable thinking that there is an all-powerful entity that can come and save us. If you're truly in high inflation, a central bank can't save you.

On Bitcoin:

The advocates of Bitcoin claim, it is a currency and a collectible like gold. But:

As a medium of exchange bitcoin is an abysmally bad currency.

Gold is a time-tested collectible. It has held its value during crises. It goes up when stocks are down. Bitcoin goes up when stock markets are buoyant and when risk capital is in the game, it behaves like a very risky tech stock which is not the way a collectible should behave.

Advice for investors on behavioural mistakes they often make

As human beings, we tend to be overconfident about the things we think we know and that ends up biting us. Humility will help you the most in the long term. Sometimes things are going to happen that are out of your control and you’ve got to be willing to let go.

You can watch the full conversation here:

— Summarised by Meher and Abhinav

The future of energy transition

At this point, it’s abundantly clear that climate change is the biggest challenge facing mankind. We’re increasingly seeing the devastating effects of climate change. Just this year we’ve seen the worst heat wave ever recorded in China and Europe, the worst floods ever seen in Pakistan, a hurricane in Florida, to name a few. Climate change is no longer a vague and distant threat, it’s here, and we’re seeing the effects from natural disasters to food shortages.

Despite knowing the devastation climate change can cause, countries around the world aren’t worried as much as they should. In most cases they’re doing the bare minimum to show some action, make vague promises that don’t mean anything and hold climate conferences that don’t lead to anything.

At the 2015 United Nations Climate Change Conference in Paris. 196 countries agreed to keep the global temperature from not rising above 2° Celsius, and 1.5° Celsius is possible by 2100. We are very likely to miss this target but nevertheless, we need to do as much as possible to come close.

To do this, the world needs a massive shift away from dirty oil and gas-based energy toward cleaner sources like solar, wind, nuclear etc.

S&P Global recently published a report on Energy Transition. Let's take a look at some of the important insights.

Oil

Oil demand peaked in developed countries in 2019 but developing countries, with their growing middle class and transportation needs, will need more oil. Global oil demand will peak in 2037 at around 112.5 million barrels per day (b/d) versus the 101 million b/d projected for 2022.

The transition from oil is complicated. While renewables like solar and wind can replace coal and gas, it’s not so easy to replace petrol and diesel. Electric vehicles are still decades away.

American and European companies are responding in different ways. European companies are investing more in renewables, while American companies are investing more in carbon capture technologies.

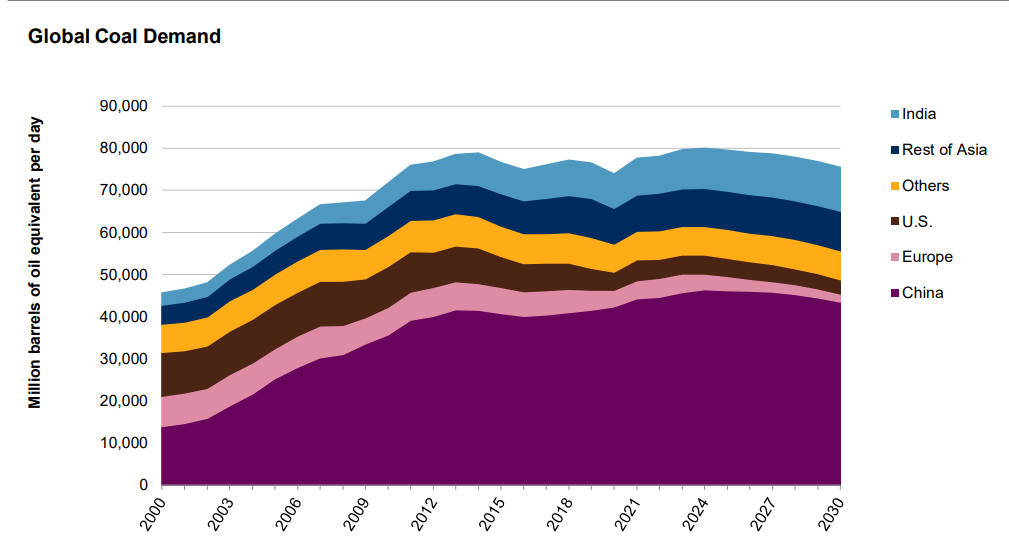

Coal

Coal accounts for about 25% of primary energy globally (and about 2/3rd of the power sector’s generation), but this will reduce to 21% by 2030 and trend downwards thereafter

In the US it will fall to 12% by 2030 (from 22% in 2021). But issues like the reliability of power, an area where renewables still lack, could hamper the progress.

(Source: S&P)

In Europe, emissions reduction policies will lead to a drop in coal to less than 5% of the energy mix in 2030 (15% in 2020). However, Russian gas interruptions have temporarily delayed the retirement of coal plants. Germany, for example, is considering setting up a 10 gigawatt (GW) coal-fired power generation capacity reserve and many Eastern European countries are still heavy users of coal.

Electricity demand is increasing in Asia and coal is the most affordable option. China and India account for 70% of the world’s coal demand. At the 26th UN Climate Change Conference, where over 40 countries agreed to phase out coal, China and India agreed only to phase down. For India, it’s not just about reducing its carbon emissions, the coal industry also provides 3.6 million direct and indirect jobs in 159 districts, often the most backward.

Another practical factor is that the coal plants in the West are approaching the end of their life cycles (40-50 years) while Asian plants are much younger, making early closures unlikely.

Are China and India the villains? Short answer, No.

Rapid industrialization in the developed world produced excessive CO2 while raising the standard of living for their populations really fast. Now, emerging economies cannot be robbed of the same rights. Thus, they are given some leeway.

So what is the best case outcome for Asia now?

Well, countries could look at Carbon Capture Utilization and Storage (CCUS) but the numbers don’t add up yet. For example, for CCUS technology to be viable at its current costs, it would require a carbon price of $40-$60 per ton of CO2, whereas Chinese carbon prices currently trade at less than $10 per ton.

Click here to know more about carbon capture projects being executed around the world.

Are governments the only players here?

Not really.

Financial markets are forcing change through capital allocation. Funding availability for coal projects is shrinking.

Gas

Natural gas emits half the CO2 compared to coal. It is a source of reliable power that’s used to cover intermittent supply from renewables and seasonal demand fluctuations in summer and winter.

Energy security is an important factor for transitioning to gas from coal. For example, in China, locally procured coal is cheaper, and its supply is guaranteed irrespective of geopolitical developments.

There are cleaner alternatives to gas for power generation, but it’s hard to substitute the use of gas as a raw material in chemical production.

(Source: S&P)

Europe aims to reduce emissions and risks to supply security by eliminating Russian gas imports by 2027. If the EU achieves its goals for green gas, it could cover 20% of European gas demand by 2030 in two ways

Through a biogas target of 35 billion cubic meters (bcm) by 2030 i.e. 10x higher than current levels (8% of European gas demand) and

through green hydrogen targets of 10 million tonnes of domestic production and 10 million tonnes of imports by 2030.

Nuclear

Nuclear is an important zero-carbon source of energy. 1 GW of nuclear power saves 3 million tonnes of CO2 emissions per year compared to gas (6 million tonnes compared to coal). The main problem with Nuclear power is the stability risks of reactors and waste disposal concerns.

The crisis in Europe has increased the focus on the security of the energy supply, leading to greater support for nuclear power.

(Source: S&P)

As per S&P the share of nuclear power in Europe and the US is decreasing and will reach about 15% of the power mix by 2035 (from 20% in 2020).

But one must note that the European Parliament just labelled nuclear as green for taxation benefits. Germany has delayed its plans to close nuclear power plants by 2022, and Belgium has extended the operation of two reactors to 2035. France announced plans to build 14 new nuclear reactors by 2050 to offset the closure of old plants. The UK also plans to achieve a 24 GW target from nuclear power plants by 2050. Nuclear power amounts to 20% of the energy mix in the USA, and 2 new plants are expected to become critical in 2023.

China's 14th five-year plan (2021-2025) laid out plans for 70 GW of operational units by 2025 (up from 55.7 GW currently) and it could rise to 145 GW by 2035.

(Source: S&P)

India’s nuclear power capacity of 6.8 GW will also increase to 22.5 GW by 2031.

Renewable Energy

What are the major roadblocks for renewable energy generation?

It is unreliable as it depends on weather conditions. Storage cost for excess energy generated during good weather conditions is also very high.

Renewable energy technologies are new and inefficient. The installation and maintenance cost for such facilities is quite high.

Obtaining permits for renewable projects is hard. Measures like REPowerEU are trying to tackle this through “renewables go-to zones”. These are locations suitable for the installation of renewable energy plants with minimal environmental impact.

Renewable energy projects take up a lot of space. A 10-acre solar plant generates about 2 MW. In the same space, a nuclear power plant can produce 850 MW.

Renewable energy sources make up the majority of new investments in power generation, yet they still represented just 13% of global primary energy consumption in 2020. This will increase to 18% by 2030.

As per the REPowerEU strategy, the share of renewables (including hydro) will reach 45% with 1236 GW by 2030 from 350 GW today.

In the US the Inflation Reduction Act, of 2022 gives new and expanded clean energy tax credits and installed wind and solar capacity will reach 510 GW by 2030 from 225 GW in 2021.

China has been adding 100 GW of renewable capacity per year, its 2030 target of 1200 GW is well within reach and likely to be exceeded.

In India, renewable energy sources have a combined installed capacity of 163 GW. Click here to see the breakup. In 2015, India committed to a 40% share of power generation from non-fossil fuel sources and achieved this target a decade ahead of the 2030 timeline.

India now aims to achieve Net Zero Emissions by 2070 while increasing renewables capacity to 500 GW by 2030.

As the cost of renewable energy gets cheaper by the day it is inevitable that renewables will someday become our primary source of electricity.

Who will be the major driver of this change? Will it be state-led or will private financial institutions allocate capital more effectively than anyone else?

There is an argument that the entrepreneurial state must lead on climate change, with the private sector playing its part. You can find more on this here.

(Source: Visual Capitalist)

More on the topic

Carbon-Capture Projects Are Taking Off. Here’s How They Stash the Greenhouse Gas

The Entrepreneurial State Must Lead on Climate Change

The world is going to miss the totemic 1.5°C climate target

— Written by Abhinav and Bhuvan

🐦 On Twitter

📖 Reading Recommendations

Handle Hard Well - Ted Lamade

Like the sirens from Greek mythology, low interest rates seduced investors into speculating in cryptocurrencies, meme stocks, and get-rich-quick schemes. In pursuit of higher returns, investors’ due diligence waned and their perception of risk became skewed, especially as nearly every investment they touched appreciated in value. It all felt too easy.

Unfortunately, in pursuit of higher returns, many investors this time around once again chose what is untried, less safe, and less secure. This means we are likely in for a tough sled. It is going to be hard. Interest rates are the price of money and that price has gone up. A lot.

These periods aren’t fun. They never are, but the good news is that in their wake something positive happens.

Continue reading…

The Present Defines the Past - Nick Maggiulli

While we can imagine many different ways in which history could’ve unfolded, at the end of the day we don’t live in those alternate realities. We live in this one.

The present defines the past. How we view yesterday is determined by what is happening today. Something that seemed trivial years ago can suddenly have meaning and something that was once important can instantly lose its significance.

Whatever you’re thinking right now, you have to realize that you’re being biased by current events. The present is redefining your past. Sometimes this is necessary so that you don’t make the same mistakes again in the future. However, sometimes, the present can teach you the wrong lessons. Differentiating between the two (i.e. signal vs. noise) is the hard part.

Continue reading…

The Opportunity Cost of Everything - Jack Raines

Decisions themselves are quite literally the inflection point of opportunity where we choose one path over another.

You are either too disinterested to pursue what you want out of life, or too vain to realize you are pursuing short-lived things.

The thing about life is that you don't get a do over. You don't get to go back. You don't get to reach the mountain top, realize that you can't hold on to those fleeting feelings of success, and try to reset your life. Because those dots in your calendar can't be erased.

Life isn't a Pixar film. It's not a television series. Our life isn't some chain of events and decisions that leads to a climax. A final moment of victory. Life is the chain of events itself.

🎧 Listen to

— Curated by Shubham

Thank you for reading. do like and share this with your friends and let us know your views in the comments section below.

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna