Understanding India's manufacturing sector; understanding markets; sometimes its okay to do nothing

#Issue 31

Welcome to the latest issue of Markets and Macros by TradingQnA

Understanding India’s manufacturing sector

Why this topic?

India is witnessing jobless growth. Our demographic dividend could become a demographic nightmare If we don't fix the unemployment problem, if not inequality will become worse. There's research showing that jobless growth can lead to civic strife.

The manufacturing sector is more employment intensive than the services sector. It can also absorb the lower skilled workers which can reduce the pressure on the agriculture sector that employs about 46% of the workforce but only contributes to about 20% of the GDP.

Rural India accounts for a majority of the country’s manufacturing: 55% of the economy's manufacturing Gross Value Added (GVA) and 63% of India’s manufacturing fixed capital. Boosting manufacturing can reduce the pressure on cities as more people can be employed in the rural areas.

The government has introduced several measures such as PM GatiShakti, the National Logistics Policy, and the Production-Linked Incentive schemes to name a few.

Compared to any point in Indian history, we have a realistic chance of building a solid manufacturing base. The fact that countries want to diversify away from China helps.

Where do we stand?

As per the economic survey, growth in industrial income has kept pace with overall GVA growth in the economy since FY20. Manufacturing GVA, which contributes more than 50% of industrial GVA, has grown at a higher rate compared to overall GVA.

GVA explained

In economics, gross value added (GVA) is the measure of the value of goods and services produced in an area, industry or sector of an economy. "Gross value added is the value of output minus the value of intermediate consumption; it is a measure of the contribution to GDP made by an individual producer, industry or sector; gross value added is the source from which the primary incomes of the System of National Accounts (SNA) are generated and is therefore carried forward into the primary distribution of income account. — Wikipedia

However, in FY23, the Industry sector witnessed 4% growth compared to 10.3% in FY22. As per the survey this is likely due to input cost-push pressures, supply chain disruptions, and the Chinese lockdown.

Manufacturing output was also limited by a large build up in inventory. For 5 consecutive quarters ending in Q2 of FY23, inventory had accumulated to more than 1.3% of the GDP. A stock buildup slows down manufacturing as the accumulated stock meets current demand. As the inventory starts falling, manufacturing output increases to meet current demand..

Thankfully, estimates of H2:FY23 showed improvement in overall industrial growth, especially in the manufacturing sector.

A deeper look at the sector

The manufacturing sector is not homogenous and covers everything from automobiles to textiles

India is the 2nd largest mobile phone manufacturer globally. We used to make 6 crore units in FY15 but made 31 crore units in FY23. There is however a problem with manufacturing of high end mobile devices for example, only 50% of the Iphones made in the Foxconn plant in Tamil Nadu were up to the mark.

The Indian Pharmaceuticals industry is ranked 3rd worldwide by volume and 14th by value but as per the economic survey growth has slowed due to an unfavourable base effect and the waning of the pandemic. Another reason is elevated raw material prices, increased regulatory scrutiny and lower growth in the US generics market.

Understanding base effect

The base effect occurs whenever two data points are compared as a ratio where the current data point or point of interest is divided or expressed as a percentage of another data point, the base or point of comparison. Because the base number makes up the denominator in the comparison, comparisons using different base values can yield widely varying results. If the base has an abnormally high or low value it can greatly distort the ratio, resulting in a potentially deceptive comparison. - Investopedia

The value added in production of coke and refined petroleum has increased, as crude oil prices were higher than in FY22. Chemicals and chemical products such as caustic soda, soda ash, fertilisers and petroleum products have also performed well.

Textiles, apparel and leather have been showing tepid growth as exports have shrunk.

What about employment?

As per the Annual Survey of Industries 2019-20, employment in the organised manufacturing sector is rising. Employment is rising faster in factories employing more than 100 workers than in smaller ones, suggesting scaling up of manufacturing units.

According to a press release by the Ministry of Labour and Employment, estimated employment in the manufacturing sector in India was 5.7 crore in 2017-18, 6.12 crore in 2018-19 and 6.24 crore in 2019-20.

Is this the complete picture?

Udit Mishra, writing for the Indian express thinks otherwise.

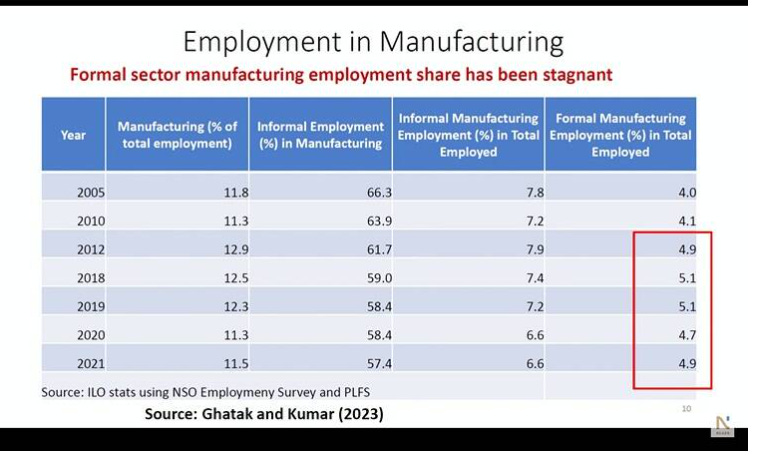

Formal employment has been stagnant while informal employment, which was the bigger contributor, has declined.

The figures given here, based on the CMIE data, are way off from the figures given by the government and there is already a debate about the accuracy of the CMIE data.

What is the problem with the existing workforce?

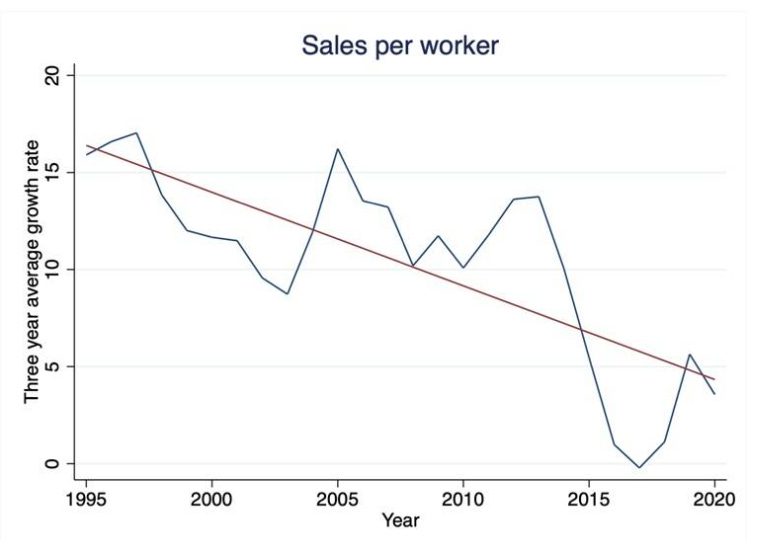

The manufacturing sector’s productivity growth is slowing down.

Our productivity per worker is also much lower than others.

Is there a fix for this?

This paper offers a solution. Productivity is strongly correlated with firms’ investments in their workers. So firms need to invest in their workforce. Too simple, no? So why isn't it happening?

Firms lack awareness or underestimate the potential benefits of investing in their employees.

As unemployment is high, there is no incentive to upskill and retain workers.

High attrition rates make firms reluctant to invest in employees as employees might use these skills to move to other companies.

Our workforce needs to be upskilled. The government is intervening through various schemes which you can find here. But, in isolation it won’t be enough, India Inc will also have to step in.

What are the other problems in this sector?

MSMEs’ share in manufacturing output in India’s Manufacturing Output during 2020-21 was around 36%. MSMEs will soon become the largest employment providers. The MSME sector itself has a whole host of issues with the main one being less favourable access to finance.

Then there is a complex maze of laws including licensing, tender and audit that are burdensome for enterprises and impedes their expansion.

Manufacturing sector is hampered by subpar supply chain management.

India is dependent on imports for things like plastic materials, iron and steel, paper, chemicals and fertilisers, and both electrical and non-electrical gear.

All of these areas need interventions but that discussion is for another day.

Additional reading

Understanding the markets

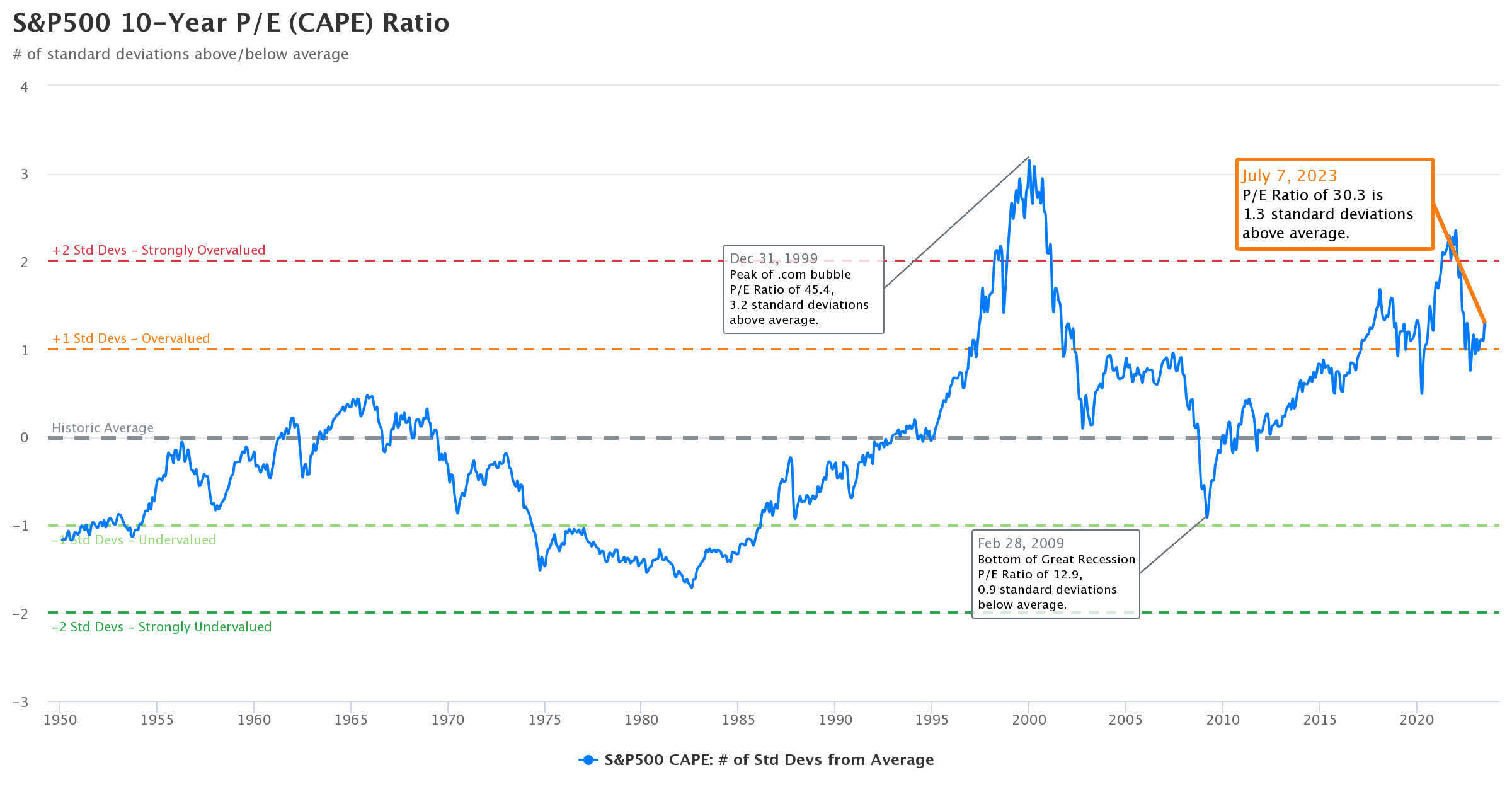

Mountains of evidence shows that market timing is almost impossible. To make matters worse, even if you get a sense that the markets are irrational and the data is screaming in your face, timing is still difficult. For example, the US markets were in the overvalue zone for well over 7-10 years if you look at the CAPE ratio. But if you had timed the markets based on valuations, you would’ve lost money.

{kind=link}

Does that mean you can’t do anything? When the markets are euphoric or stupid, even, there are some things you can do.

Having a sensible asset allocation of equities, debt and gold means you will be pretty well covered for all market cycles. In other words, diversification is the only free lunch for most retail investors like you and I.

If you are one of the gifted few, you can underweight or overweight asset classes, styles and themes based on the market sentiment. For example, value investing in the US since 2008 has performed horrendously. That also means, since it has done poorly value is cheaper than ever and has the highest future expected returns

Seasoned investors make a killing at the expense of rookies who repeat the same mistakes. How do these guys do it? They use strategies based on their experience.

One such seasoned investor is Howard Marks. He has written a memo where he discusses 5 calls he made that turned out to be right. He did this with a bit of common sense and a little bit of luck. Of course, his aim and complexities of investing are very different and might not even be prudent for most of us to replicate but you should read about it in any case. It will help you understand the way of the markets.

Compressing what he has said into a summary will rob you of a great learning experience, take some time out and read the entire memo.

If there was only one thing I could talk about from this entire memo that would be his sceptical approach. It’s very important to understand what he means by scepticism. To him

scepticism and pessimism aren’t synonymous. Scepticism calls for pessimism when optimism is excessive. But it also calls for optimism when pessimism is excessive.

Additional reading

Sometimes it's okay to do nothing

Imagine this situation

You are a goalkeeper about to face a penalty kick. You have three options to make the save. You can dive left, dive right or stay in the middle. Having looked at the stats you know the probabilities are most in your favour if you stand still. So what do you do? You dive to the left or the right. Why? Because if you don’t and the penalty taker scores it will look like you didn’t even try. Not only will you feel worse, but the fans won’t be happy – the least you could have done is put in some effort.

The penalty kick example is from a 2007 paper exploring the concept of action bias. Action bias is not just an issue for goalkeepers but also retail investors. Yet, the data shows this doesn’t work. If you just invested in index funds and chilled, you would’ve done better than all the other people trying to pick the best fund, theme style etc.

We are hardwired to think that doing something is better than doing nothing because this reduces regret. You can tell yourself a story that you tried at least.

It might seem ridiculous to suggest that thinking of ways to reduce our activity could improve investment outcomes, but it works. This idea is explored further in this blog post.

This is not just true for investing. I came across a book called Subtract which explores this theme. You can find a short summary of the book here.

Watch

Listen to

That's all from us for this issue. Thank you for reading. Do let us know your feedback in the comments below and share the post if you liked it. We are at @TradingQnA on Twitter.