The almighty dollar

Issue #6

Hey folks, welcome to another issue of Markets and Macros by TradingQnA. In this issue we take a look:

Effects of strengthening dollar

Highlights from RBIs August bulletin and more…

Written by Esha, Bhuvan, Abhinav, Meher and Shubham

Almighty dollar

Everybody is worried about an impending slowdown in economic growth across the world. Here’s the Google search trend for the term “recession.”

Pretty much everybody is attributing the cause of the global slowdown to the dramatic spike in inflationary pressures around the world, the war in Ukraine, supply chain issues, and so on. But a strengthening dollar hasn’t received as much attention as the other factors. As of writing this post, the US dollar as measured by the dollar index (DXY) is up ~15%.

Why is the dollar rising?

The dollar is a safe haven asset. Whenever there’s trouble anywhere in the world, investors rush to dollar assets. The other big reason is that rising interest rates lead to a strengthening of the dollar. Also, relatively speaking, the US is in a much better economic position compared to Europe and Japan.

What does a strong dollar mean for the global economy?

A strong dollar disproportionately affects emerging markets compared to advanced economies. It leads to lower GDP, investment growth, exports, and imports.

A rising dollar makes imports costlier for import-heavy countries reducing investments.

A BIS study showed that a 1% rise in the dollar leads to a decline in the GDP of emerging economies by 0.3%.

This is particularly true for countries that have larger dollar-denominated debts and higher foreign ownership of local bonds. A rising dollar leads to increased interest costs, leading to worsening effects on the most vulnerable emerging and developing economies.

This year we’ve already seen vulnerable countries like Sri Lanka, Zambia, and Lebanon default on their international debts. Several other countries like Pakistan, Egypt, Ghana, etc are at high risk of defaults and currency crises.

As the dollar strengthens, it weakens the other currencies, which should theoretically make the exports of emerging economies more competitive. But Druck et al. have found that this isn’t the case.

Since most of the global trade is invoiced in dollars, this effect is negated.

Given that most global trade is denominated in dollars, a rising dollar means falling commodity prices, dampening global trade and growth.

A stronger dollar leads to rising interest rates for countries and corporate with dollar debt, weakening their balance sheets.

How does this affect the markets?

Emerging markets and the dollar are negatively correlated. A stronger dollar is bad for emerging markets stocks. In this chart, I’ve compared the iShares MSCI Emerging Markets ETF (EEM), iShares MSCI India ETF (INDA)—both in dollar terms—and the Dollar index (DXY).

It’s no wonder that emerging markets are among the cheapest globally.

Dive deeper

Wonking Out: The Mysteries of the Almighty Dollar by Paul Krugman

Global liquidity and dollar debts of emerging market corporates

Dollars and exports: The effects of currency strength on international trade

Nothing Will Stop the Dollar From Getting Stronger

Highlights from RBIs August Bulletin

Private Corporate Investment: Growth in 2021-22 and Outlook for 2022-23*

*More than one-third of the total CAPEX investment envisaged during 2021-22 is expected to be spent in 2022-23.

The study on private corporate investments covers only projects costing above Rs. 10 crores and private ownership above 51%.

The important highlights

New project announcements weakened during 2019-20 and deteriorated further in 2020-21 due to the pandemic. Subsequently, with the resumption of business activities and improved sentiment, new CAPEX project announcements showed some signs of revival.

Overall, investment plans for 791 projects were made during 2021-22 aggregating to Rs. 1,94,548 crores as against 576 projects in 2020-21 with investment intentions of Rs. 1,16,603 crores. This is comparatively lower than the levels seen since 2016-17.

Greenfield projects increased significantly during 2021-22 as compared to the previous year, even higher than the greenfield projects announced during 2019-20. Just 11% of the total project cost was directed towards the expansion and modernisation of existing projects

Infrastructure projects

The total cost of such projects increased from Rs. 56,103 crores to Rs. 81,221 crores.

This sector accounted for more than half of the total project cost during 2021-22. However, its share in total project cost has declined from 74.3% in 2020-21 to 56.7% in 2021-22, despite an increase in the number of projects during the same period.

This decline was mainly driven by the falling share of the power sector. Within the power sector, announcements in solar and wind power projects were dominant during 2021-22.

The share of investment in roads and bridges improved significantly in recent years as compared from 2012-13 to 2019-20.

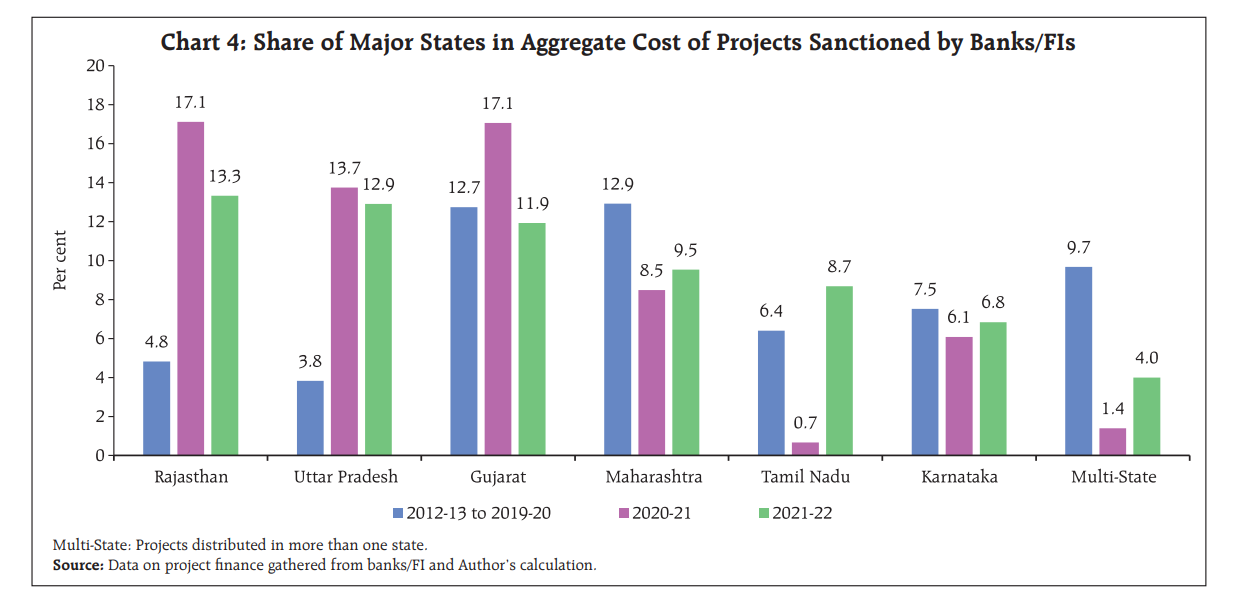

Performance of states

In 2021-22, Rajasthan accounted for the highest share in the total cost of projects sanctioned by banks/FIs, retaining the top place for two consecutive years.

While the share of Rajasthan, Uttar Pradesh, and Gujarat declined during 2021-22, Maharashtra, Tamil Nadu, and Karnataka improved their share in the total cost.

Privatization of Public Sector Banks: An Alternate Perspective

Privatization of public sector banks (PSBs) has been widely viewed as a key area of pending reforms in India.

In developing countries, the average share of assets held by PSBs declined from 40% in 1995 to 17% in 2008. While in high-income countries, it same fell from 36% in 1995 to 10% in 2008.

Post the Great Financial Crisis of 2008 (GFC) however, there has been a renewed interest in the public ownership of banks as many countries capitalized or nationalized stressed banks.

Why are PSBs important?

The Social View (Financial Inclusion)

State-owned enterprises are created to address market failures and often their social benefits exceed the social costs. An important aspect that is often ignored by proponents of privatization is the role played by PSBs in financial inclusion.

PSBs have the highest share of bank branches in rural areas and dominate in meeting the rural credit demand. PSBs have twice the number of ATMs in rural areas compared to private sector banks (PVBs).

Pradhan Mantri Jan Dhan Yojana (PMJDY), envisages universal banking access. As of July 2022, out of the more than 45 crore beneficiaries, 78% of them have accounts in PSBs. Above 60% of PMJDY accounts opened in PSBs were in rural and semi-urban areas.

As per the Global Financial Index, around 78% of Indian adults own bank accounts.

Aren't PVBs meeting their financial inclusion obligations by matching their priority sector lending (PSL) requirements?

PVBs meet their targets by investing in PSL certificates (PSLCs), especially in agriculture and small and marginal farmers categories rather than through organic lending.

These categories attract higher premiums. The PVBs pay higher premiums to meet their PSL targets rather than invest time and effort in developing skills and expertise in PSL.

Lending by PSBs is countercyclical

Lending by PSBs is either countercyclical or less pro-cyclical than lending by PVBs, especially in emerging and developing economies thus contributing to macroeconomic stability.

We saw this during the cyclical downturn that started in the Indian economy in 2017-18. By providing credit to the industry when PSV credit ran dry, the PSBs have played a countercyclical role

PSBs have also played a key role in catalyzing financial investments in low-carbon industries thereby promoting green transition in countries such as Brazil, China, Germany, Japan, and the EU.

Since the corporate bond markets in India are not deep and vibrant, industries had fewer other avenues to raise resources than banks more so for smaller entities.

In India, infrastructure finance has been a bottleneck in the country’s development and growth. PSBs have a lion’s share in these lendings and this is crucial against the backdrop of the withering away of erstwhile development financial institutions.

The efficiency argument

The results of a long-term study by the RBI suggest that where profit maximisation is the sole motive, the efficiency of the PVBs has always surpassed that of the PSBs. However, when the objective is financial inclusion—like total branches, agricultural advances and PSL advances—PSBs prove to be more efficient than PVBs.

A Steady Ship in Choppy Waters: An Analysis of the NBFC Sector in Recent Times

Non-bank financial intermediaries (NBFIs) accounted for almost half of the global financial assets in 2020.

India is still a small player (0.7% of the global NBFI assets in 2020). But the NBFI sector as a share of India’s GDP has increased from 18% in 2002 to 60% in 2020. As of January 31, 2022, there were 9,495 Non-Banking Financial Companies (NBFCs) registered with the RBI.

The consolidated balance sheet of NBFCs recorded a higher year-on-year growth for the quarter ending December 2021 as compared to December 2020.

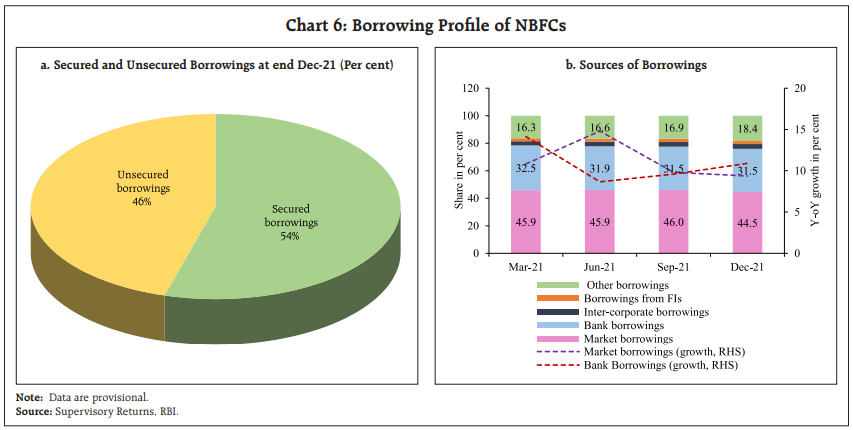

Liabilities structure

Borrowings, reserves and surplus together constitute 88% of the liability side of the balance sheets. Reserves and surplus grew robustly owing to ploughing back of profits.

NBFCs, other than deposit-accepting NBFCs, rely heavily on bank and market borrowings (Debentures and Commercial Papers) to meet their funding requirements.

Post the IL&FS episode, there has been a gradual realignment of NBFCs’ borrowings with increasing reliance on long-term borrowings.

NBFCs’ Commercial Papers (CPs) subscriptions are dominated by mutual funds and banks, together accounting for 86.8% of total CP subscriptions by December 2021.

Assets structure

Loans and advances followed by investments are the largest components on the assets side with long-term investments dominating total investments.

NBFC credit grew 11.1% at the end of December 2021 as compared to 17.7% in December 2020, due to a favourable base effect.

NBFCs continued their investment in equity shares and government securities as a result of which investment in government securities grew by 41.6% in December 2021.

Financial Performance, Asset Quality and Capital Adequacy

The profitability of NBFCs improved in Q3 of the financial year 2021-22 compared to Q3 2020-21. The asset quality, which had worsened due to the second wave also stabilised during the third quarter of FY 2021-22.

NBFCs are required to maintain a minimum capital ratio of 15% of their aggregate risk-weighted assets (including both on and off-balance sheet items).

To further strengthen their capital position, the PCA framework for NBFCs will become effective from October 2022. Any NBFC breaching the risk threshold will fall under PCA.

However, the NBFC sector looks comfortably poised to comply with these new regulations with an overall CRAR (Capital to Risk Asset Ratio) of 27.5% by the end of December 2021.

Distribution of Credit and NPAs

NBFCs deploy the largest quantum of credit to the industrial sector followed by retail, services and agriculture.

Within the industry, power was the largest recipient of credit due to many large government-owned NBFCs which operate in this segment (33.7% in overall credit extended by Dec end 2021.)

The industrial sector accounted for the largest share of NPAs followed by retail loans, services, and agriculture respectively.

Within the industrial sector, the power sector accounted for 30% of overall NPAs (the retail sector accounted for 31.3% of NPAs). In the services sector, Commercial Real Estate accounted for the largest share of NPAs (5.8%).

🐦On Twitter

📖 Reading Recommendations

The Illusion of Knowledge by Howard Marks

In his latest memo, Howard Marks explains why creating profitable forecasts is so difficult. He discusses the incredible complexity involved in modeling an economy and that forecasting mostly provides the illusion of knowledge and also argues that investors are better off accepting reality and focusing on what they can know.

Read - The Illusion of Knowledge by Howard Marks

Three Big Things: The Most Important Forces Shaping the World by Morgan Housel

Every current event – big or small – has parents, grandparents, great grandparents, siblings, and cousins. Ignoring that family tree can muddy your understanding of events, giving a false impression of why things happened, how long they might last, and under what circumstances they might happen again. Viewing events in isolation, without an appreciation for their long roots, helps explain everything from why forecasting is hard to why politics is nasty.

Those roots can snake back infinitely. But the deeper you dig, the closer you get to the Big Things: the handful of events that are so powerful they influence a range of seemingly unrelated topics.

Continue reading…

Which Inflation Hedges Have Worked? by John Rekenthaler

Over time, most investments overcome inflation’s headwind. Stocks eventually prosper as businesses recoup their higher costs by increasing the prices that they charge their customers. The prices of tangible assets, such as real estate or gold, rise. Even bonds recover, as their yields adjust to the new reality.

The transition, however, tends to be painful.

Good Ignorance by Jack Raines

Ignorance gets a bad rap, but applied ignorance can buy you enough time to bridge the gap between sucking and succeeding. If you fully understand the risks and low odds of success for a new endeavor from the offset, you would likely never start. But if your ignorance prevents you from quitting, and you keep hacking away day after day, you just might pull it off.

Just doing a lot of things works, if you can do it long enough.

That’s it from us today. Hope you loved reading the latest issue, do let us know your views in the comments section below. And do like and share 😃

If you have any queries related to trading, investing and anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna

Hii