RBI May 2023 bulletin, passive funds, AT1 bonds, climate change and gender, recycling and reclaiming life from work

#Issue 27

This is the latest issue of Markets and Macros by TradingQnA written by Abhinav and Shubham.

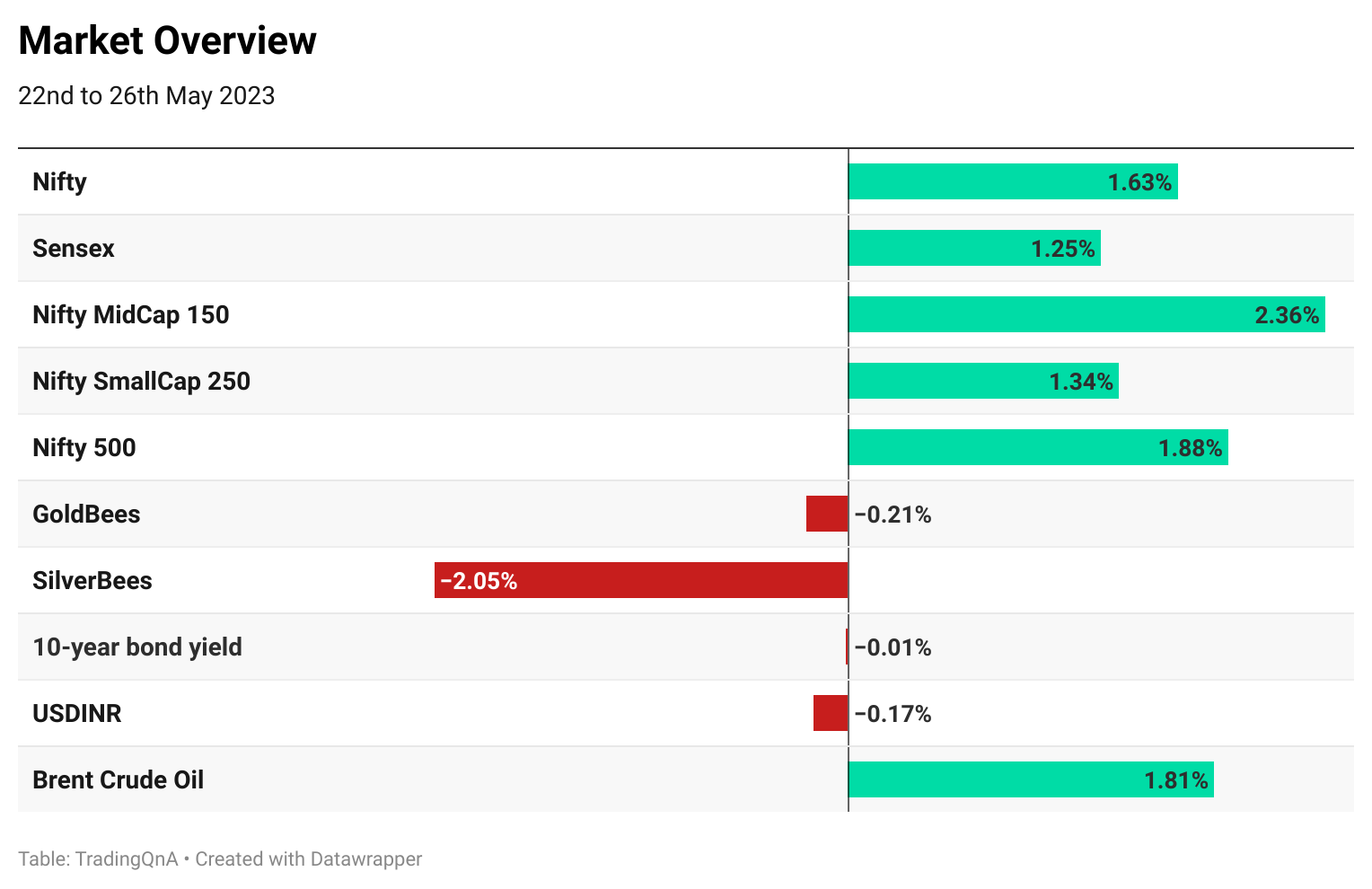

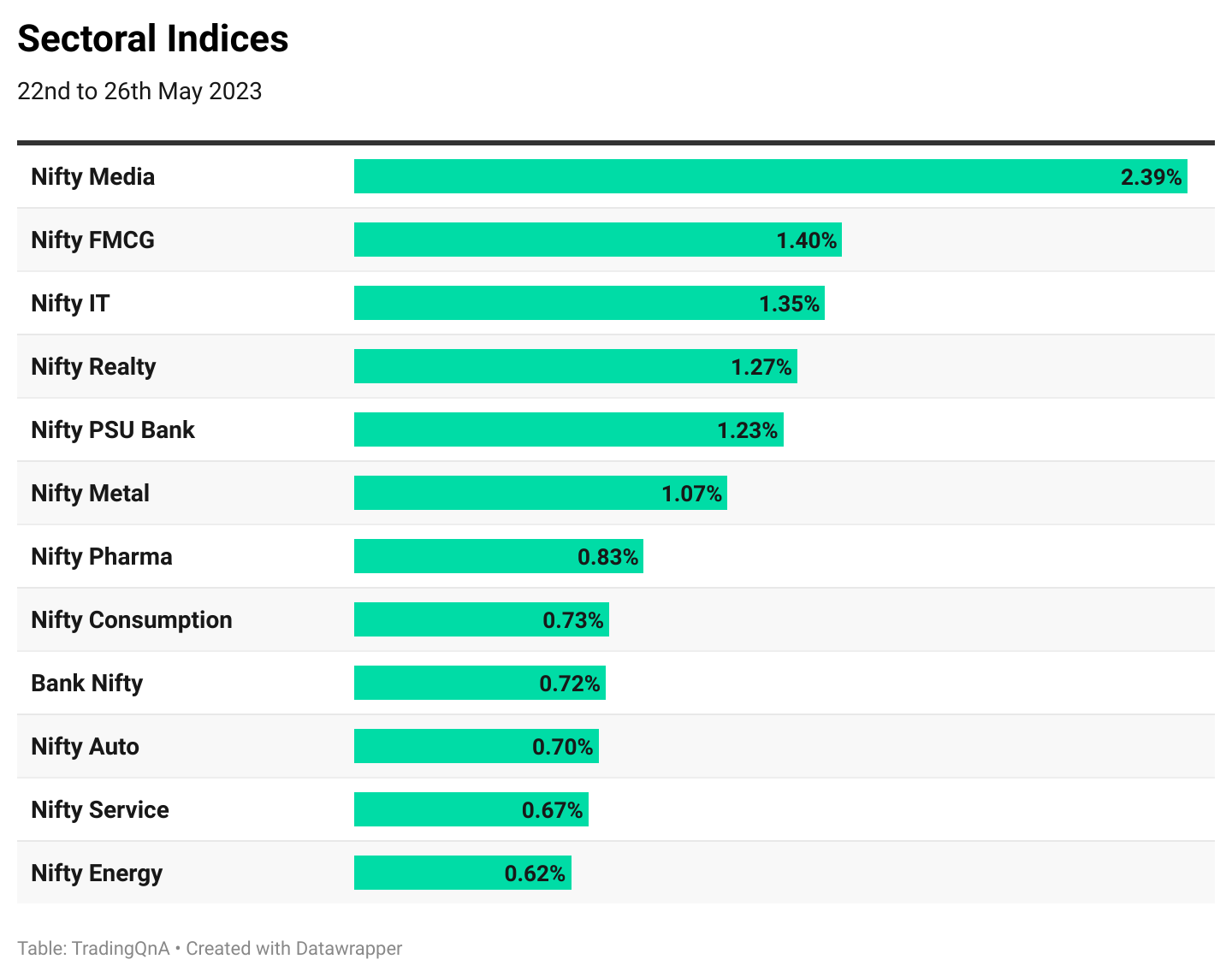

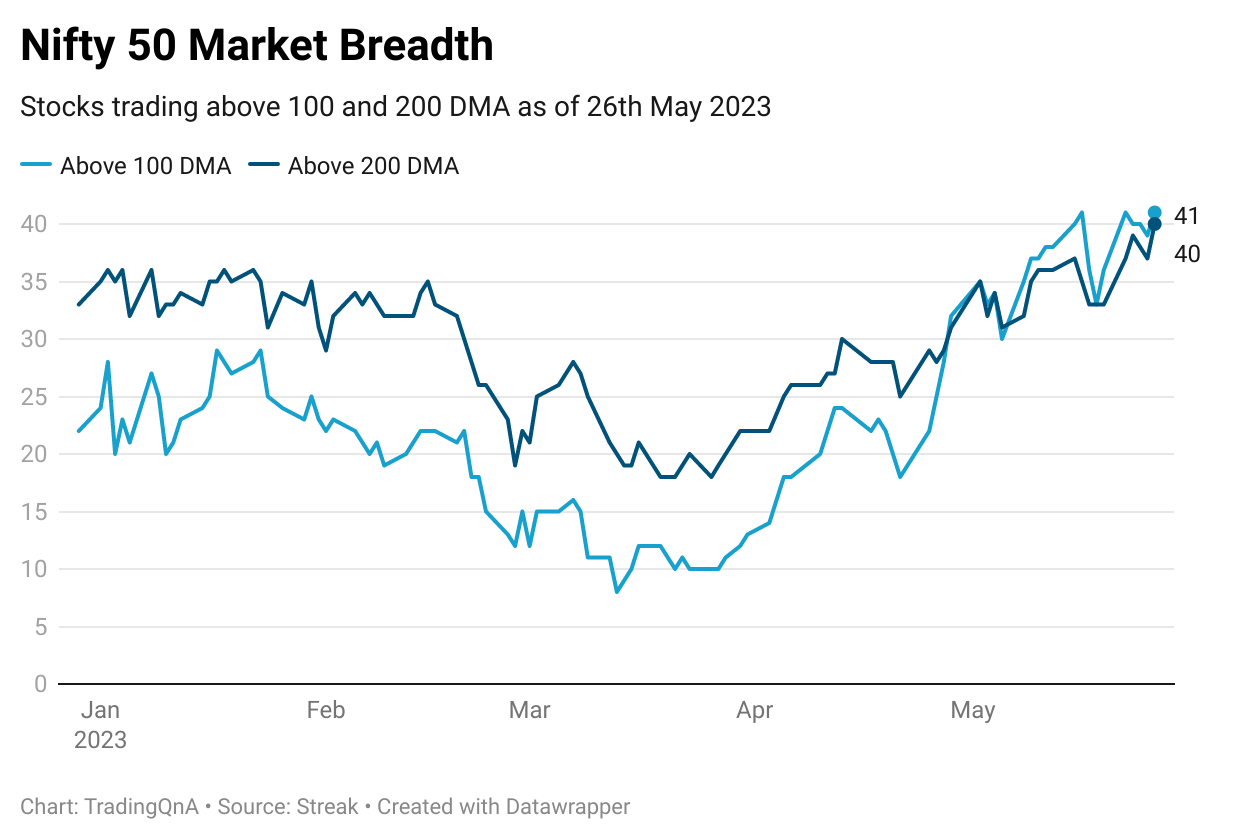

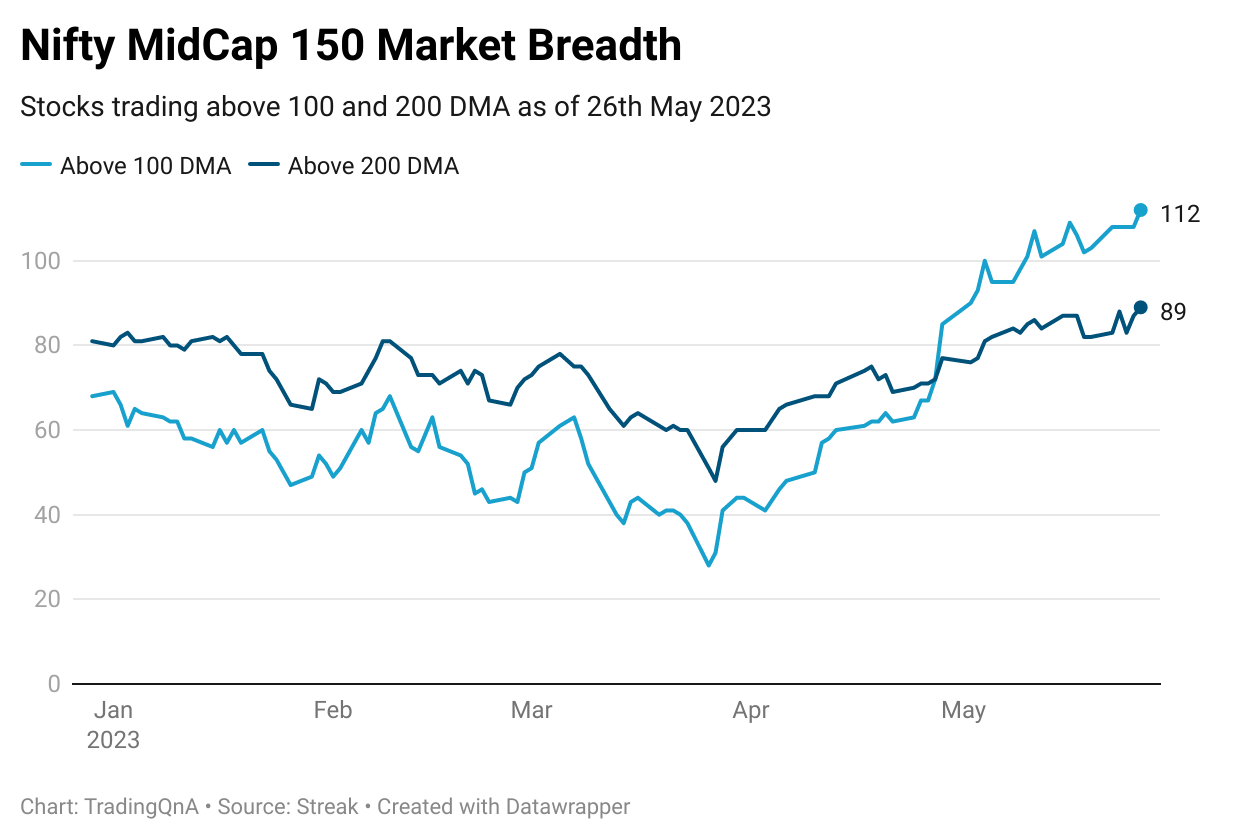

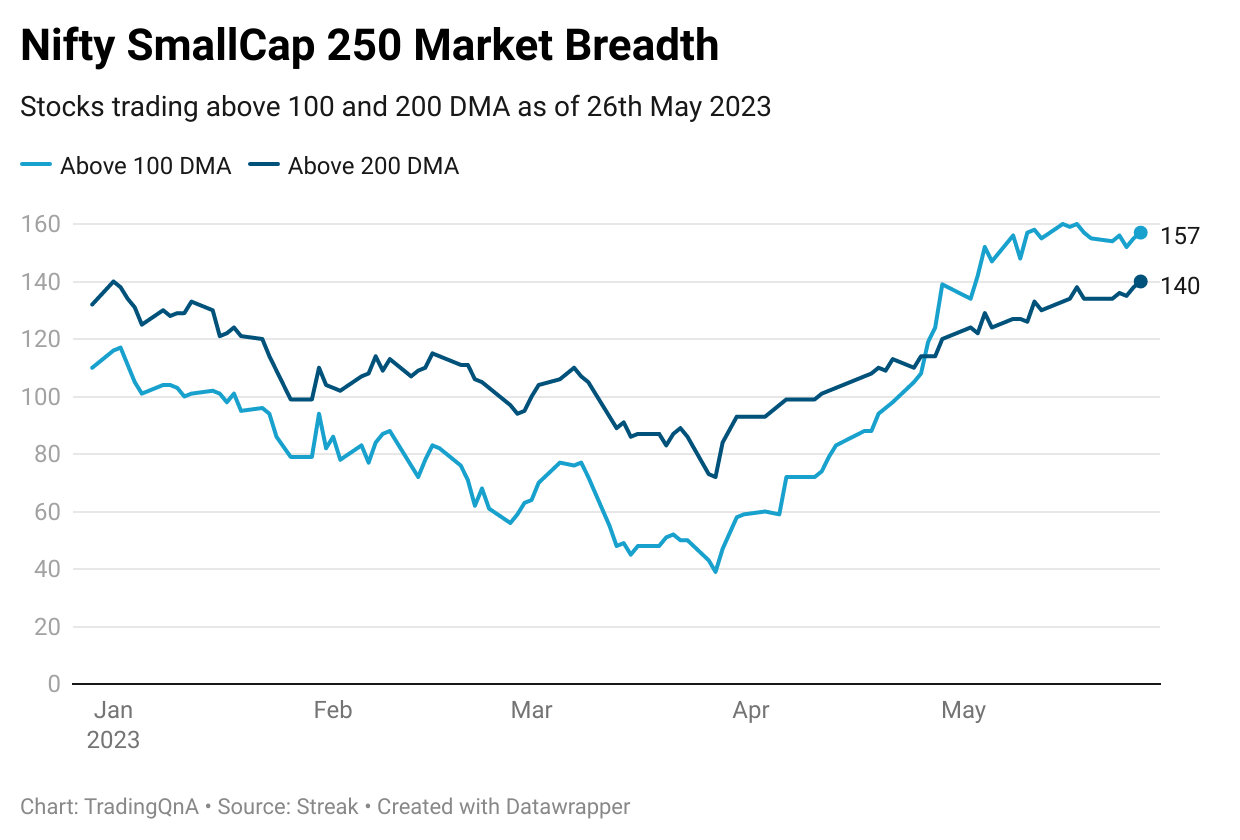

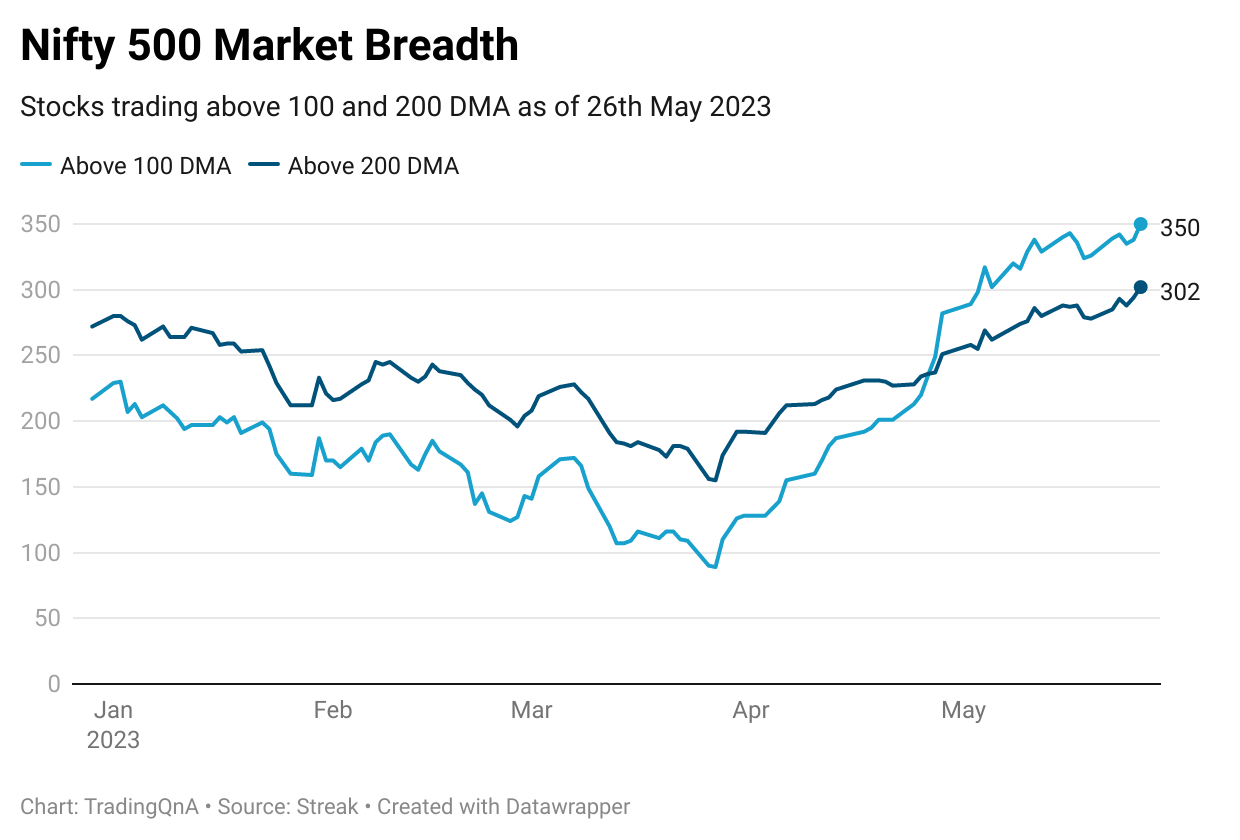

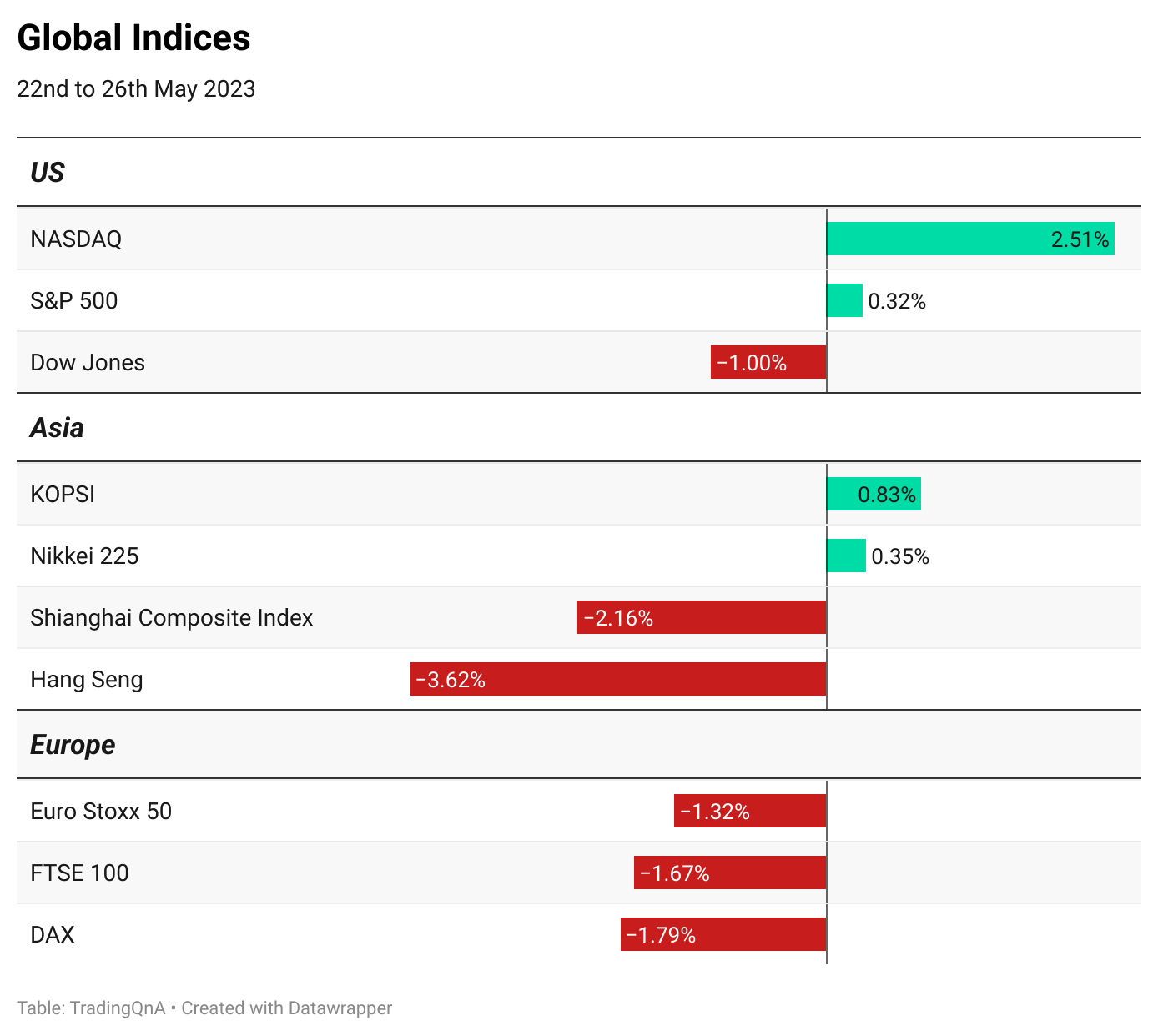

Weekly market wrap

Highlights from RBI’s May 2023 bulletin

My colleague Meher Smaran has gone through the RBI’s May 2023 Bulletin and has covered the insights from it in this post on Trading Q&A.

This post covers a broad range of topics ranging from FDI in semiconductors, corporate performance, bond markets, rice and wheat procurement, Rainfall and Reservoir levels during El Niño years, state finances, India's merchandise exports growth trajectory after COVID, coal, renewable energy and more.

Passive funds

IndiaDataHub has shared a thematic report on passive funds with some interesting data points and charts.

IndiaDataHub works towards addressing the problem of accessibility of data. All the data on this platform has been sourced directly from primary sources such as the various ministries of the Government of India or the RBI or in the case of Global data from organisations like the World Bank, the World Trade Organisation, or the Bank for International Settlements.

So if you are someone who needs access to such data, do check them out.

Coming back to the report on thematic funds, you won’t be able to download it unless you subscribe to the pro version of IndiaDataHub, but don’t worry Meher is here to the rescue. He has shared some insights from the report on this post on TradingQ&A.

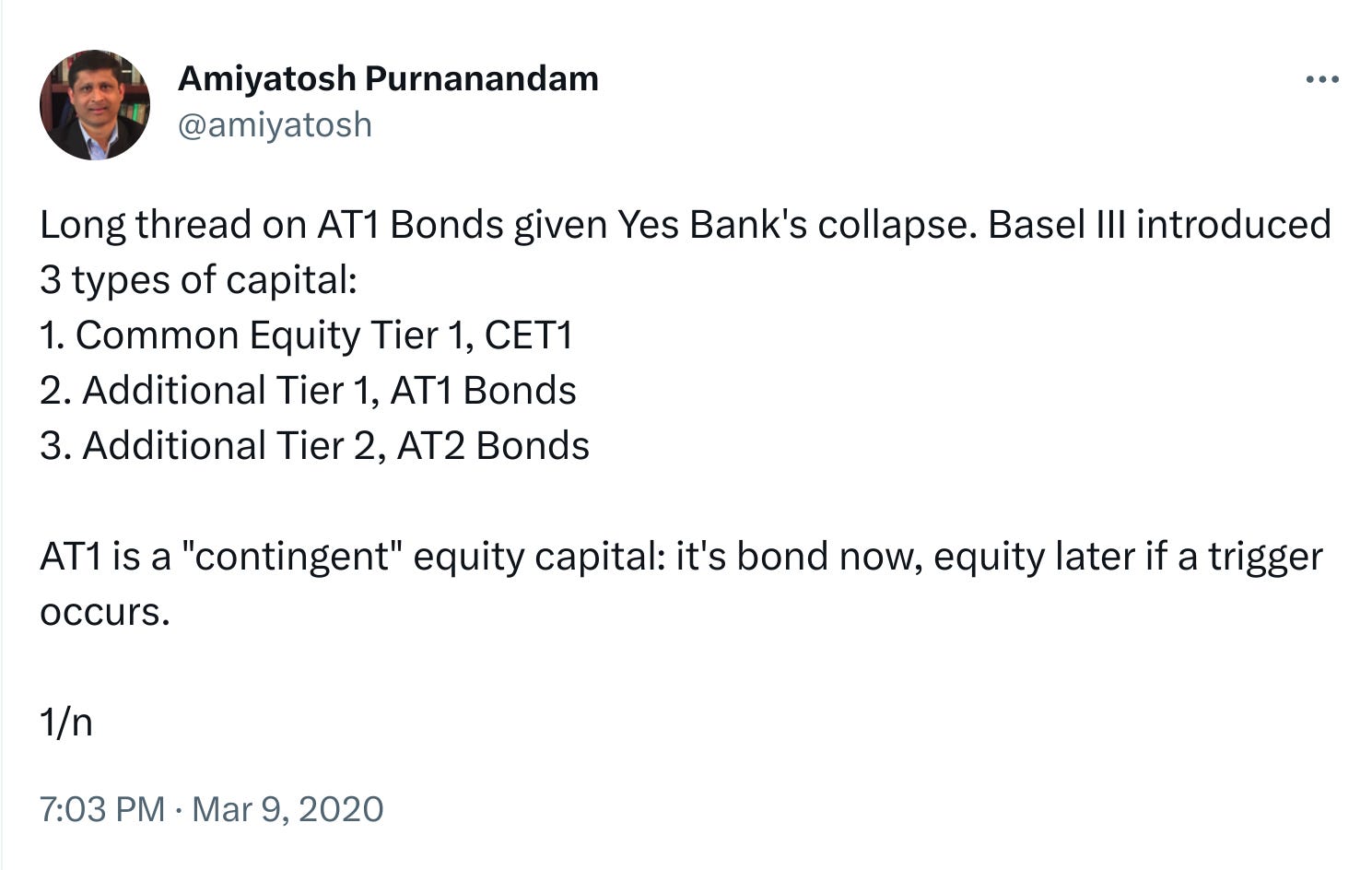

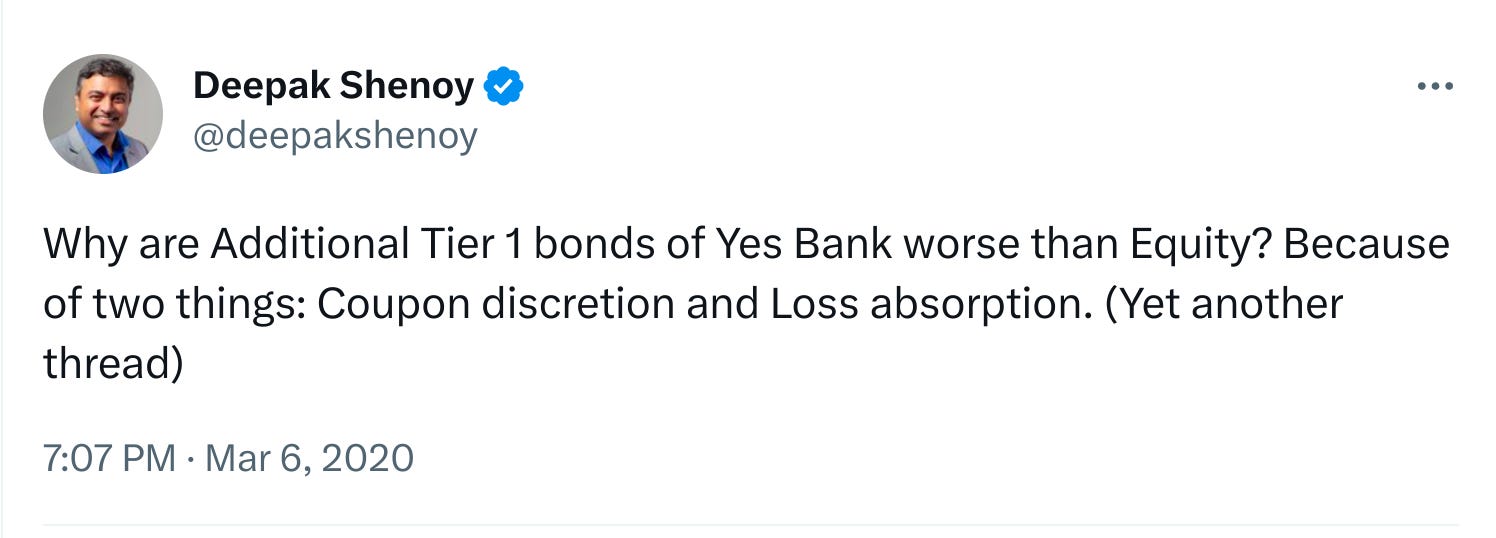

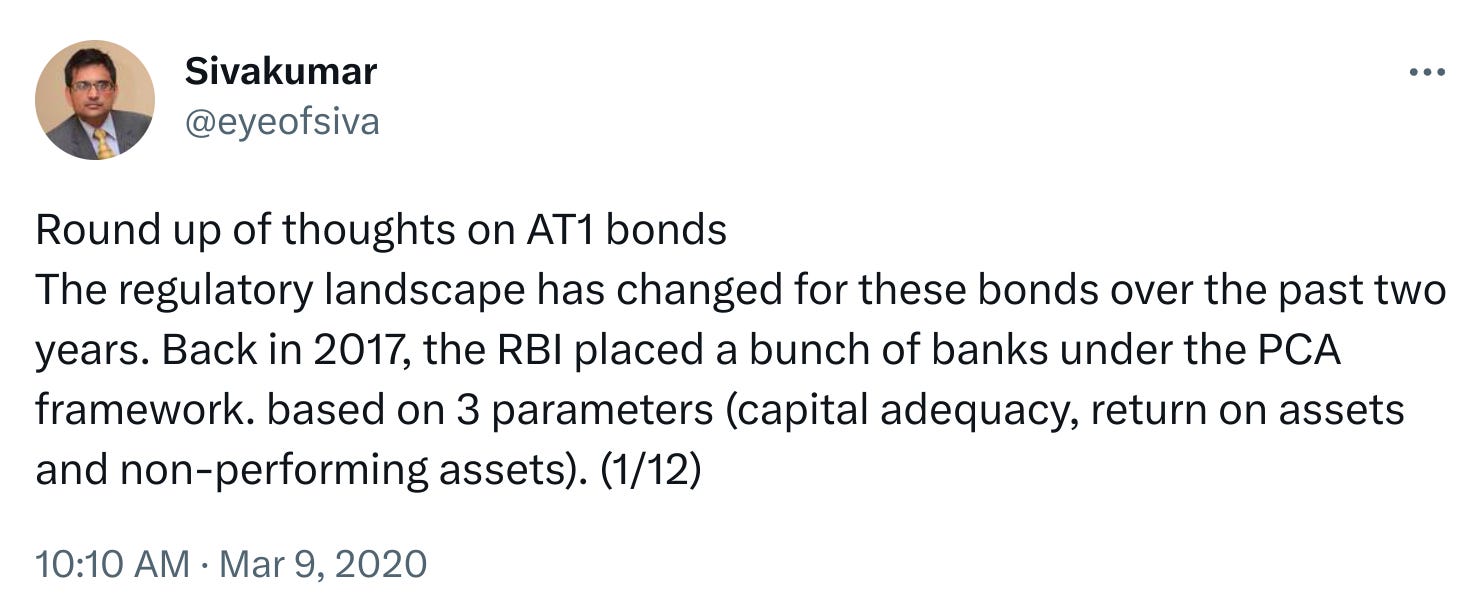

AT1 Bonds

I just came across this alleged case of mis-selling of AT1 Bonds by HDFC Bank employees. This instantly reminded me of 2020 when Yes Bank wrote-off Rs 8,500 crore worth of such bonds from its balance sheet. Unsuspecting retail investors, who had been mis-sold these bonds saw huge chunks of their investments wiped out and are still fighting a court battle against Yes Bank's decision.

So what exactly are AT1 bonds?

Remember the Lehman Brothers and the subsequent banking crisis? That’s what birthed the concept of AT1 bonds. After a bunch of banks bungled, regulators formulated Basel III norms for banks. Under Basel III banks had to raise the amount of their own capital they needed to hold before they raised external deposits and loans.

Basel III norms require Indian banks to maintain a total capital ratio of 11.5%, split into 8% in tier 1 capital (own equity, reserves etc) and tier 2 (supplementary reserves and hybrid instruments).

AT1 bonds, also known as “unsecured subordinated perpetual non-convertible” bonds, make up part of a bank’s Tier 1 or permanent capital and banks issue them to make sure they can meet Basel III norms on equity capital.

Want to know more about AT1 bonds? Follow these Twitter threads to get an idea:

Click here to read the full thread.

Click here to read the full thread.

Click here to read this full thread.

So what is the mis-selling angle?

Read this to know how AT1 bonds are mis-sold. Long story short, innocent investors are lured with phenomenal returns and are blissfully kept unaware of the risks.

We at Zerodha have always advocated for investor education, check out Varsity, since we believe that one should never invest in things they don't understand irrespective of the promise of phenomenal returns. Irrespective of our best efforts, these things continue to happen.

What are the risks involved with AT1 bonds? Check this out.

Are we doing enough on the climate front?

The World Meteorological Organisation (WMO) has warned that at least one of the next 4 years could be 1.5 degrees hotter than the pre-industrial average. This was supposed to be the target for this century under the Paris Agreement. While this is going to be a temporary (hopefully) outlier event, this is still worrisome. The average global temperature in 2022 was about 1.15°C above the 1850-1900 average. When the policymakers meet in Dubai later this year, this is something that they will have to take a look at and try to increase the seriousness of the global effort against climate change.

As per the World Meteorological Organization’s Atlas of Mortality and Economic Losses from Weather, Climate and Water-related hazards, India had the 2nd highest number of deaths from climate change from 1970-2021. Apart from this

Extreme weather, climate and water-related events caused nearly 12 000 disasters from 1970-2021

Reported economic losses are US$4.3 trillion and rising

The death toll is at 2 million, with 90% in developing countries

Gender and climate change

Climate change impacts everyone, but its harshest consequences are felt by the most vulnerable. In times of crisis, women are often left behind and face increased health and safety risks due to inadequate infrastructure and the unequal burden of domestic care. To ensure effective and equitable solutions to climate change, it’s essential to recognise the disproportionate impact on women and provide them with a seat at the decision-making table. While writing for the Indian Express Shagun Sabrawal and Saumya Swaminathan cover this topic extensively, you can check out their opinion piece here.

Recycling plastics is not as efficient as you think

A recent study suggests that anywhere between 6-13% of the plastic processed could end up being released into water or the air as microplastics. There are growing concerns that recycling isn’t as effective of a solution for the plastic pollution problem as many might think. Not to say that we shouldn’t recycle, we should just keep in mind that just recycling is not enough.

Book recommendation - Reclaiming life from work

I recently came across a book review for The Good Enough Job: Reclaiming Life from Work, by Simone Stolzoff. Today many of us are completely consumed by our work and the distinction between work life and life in general is blurring. This can’t obviously be a good thing even though for most people their work is their most fulfilling pursuit and often ends up defining their identity. If you feel like I am talking about you, you should definitely read this book. It seems like an interesting read and covers 5 important insights. Briefly put, they are:

Intrinsic motivation tends to be more fulfilling than extrinsic motivation

Valuing time tends to be more fulfilling than valuing money.

Satisficing tends to be more fulfilling than maximising

Define what good enough means to you

Diversify your identity beyond work.

Podcast recommendations

That's all from us for this issue. Thank you for reading. Do let us know your feedback in the comments below and share the post if you liked it.