Markets and Macros by TradingQnA: Issue #5

Issue #5

Hello people, welcome to the latest issue of Markets and Macros by TradingQnA. In this issue, we take a look at;

What’s happening with the housing market?

Climate change and its economic impact

TradingQnA Book Club: The Wisest Owl, and some more interesting stuff…

Written by Bhuvan, Abhinav, Meher and Shubham

What’s happening with the housing market?

Globally, real residential property prices increased by 4.6% year on year in Q1 2022. This is reflected in an 11.2% surge in nominal terms, the first double-digit growth recorded since the 2008 financial crisis. Advanced Economies (AEs) recorded 8.5% year-on-year growth and Emerging Market Economies (EMEs) recorded 1.6 % growth on average.

In real terms, global house prices now exceed their immediate post-2008 average levels by 29%. They have been up by 41% in the AEs and by 19% in the EMEs.

Recent developments confirm the significant rise in global residential prices observed since the Covid-19 pandemic. Compared with Q4 2019, real prices have increased by 60% in Turkey, by 30% in Canada and by more than 20% in the US and Australia. A major exception is India, where they have fallen by 7%.

What has been happening in the US Housing market since the pandemic?

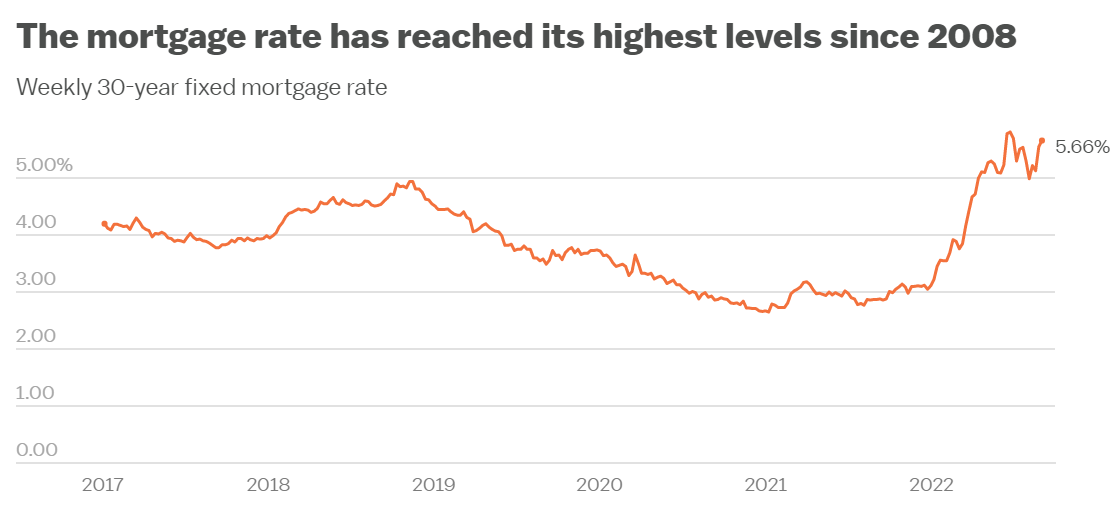

The average 30-year fixed mortgage rate reached 5.66 per cent on Sept 1, slightly down from its peak of 5.81% in June. During the pandemic, mortgage rates fell sharply (in January 2021, they reached 2.65%) increasing the demand for homes as lower rates made purchasing a house cheaper.

With mortgage rates rising again, buyers are getting priced out of the housing market leading to a cooling of demand and an increasing inventory. The share of US homes that were listed for 30 days or longer increased by 12.5% in July compared to a year earlier.

Initially, prices increased as people took advantage of lower rates earlier in the pandemic. The combination of lower mortgage rates and a short supply of houses led to bidding wars. Now prices are starting to come down but they still remain much higher than they were a year ago.

The median existing-home price was $403,800 in July. That’s down $10,000 from June, but still 10.8% higher than a year before.

Construction of new homes has slowed as builders worry about a drop in demand because of higher mortgage rates. Construction on a new residential housing unit fell to 1.45 million in July. That was a 9.6% decline from the month before.

After rising steadily earlier this year, new listings dropped to 670,766 in July, that’s down 132,649 new listings from the month before.

After rising steadily earlier this year, new listings dropped to 670,766 in July, that’s down 132,649 new listings from the month before.

“They were able to lock in really low mortgage rates, so they don’t really have a reason to sell. If we entered into a recession and unemployment went up and homeowners couldn’t pay their mortgages anymore, then that would lead to a much faster decline in prices than what we’re seeing now. But I think it’s unlikely that will happen.” - Daryl Fairweather, the Chief Economist at Redfin

Even as new listings fall, the total inventory of houses has climbed as supply improves. The number of active for-sale listings increased by 5.1% in July from the month before, marking the fifth consecutive month that inventory has increased.

At the same time, however, affordability is falling. It fell in June as the monthly mortgage payment climbed 53.7% while the median family income rose 5.8% compared to a year ago.

Are we poised for a correction?

“So right now we’re getting a backlash of the change in direction from free money to now the rise in [mortgage] rates and inflation. So the market is poised for a fairly significant [price] correction. And we’re already seeing signs of that over the last several months”

“As fast as [inventory levels] are rising and demand is plummeting, we could see pretty substantial [home] price corrections. But it’s going to vary by market,”

Moody’s expects US home prices to decline up to 5% nationally. If a recession hits, Moody's forecast moves from 5% to 10%. Fitch Ratings forecasts that home prices could fall between 10% and 15% if the housing downturn takes a worse turn.

However, not everyone shares this bearish outlook. Over the coming year, Zillow predicts that U.S. home prices will rise another 2.4%. Goldman Sachs released a paper titled “The Housing Downturn: Further to Fall” forecasting that the US housing market will end 2022 down across the board. They expect home price growth to decelerate significantly but still forecast that home prices will rise 1.8% in 2023 and 3.5% in 2024.

A look at the Indian property market

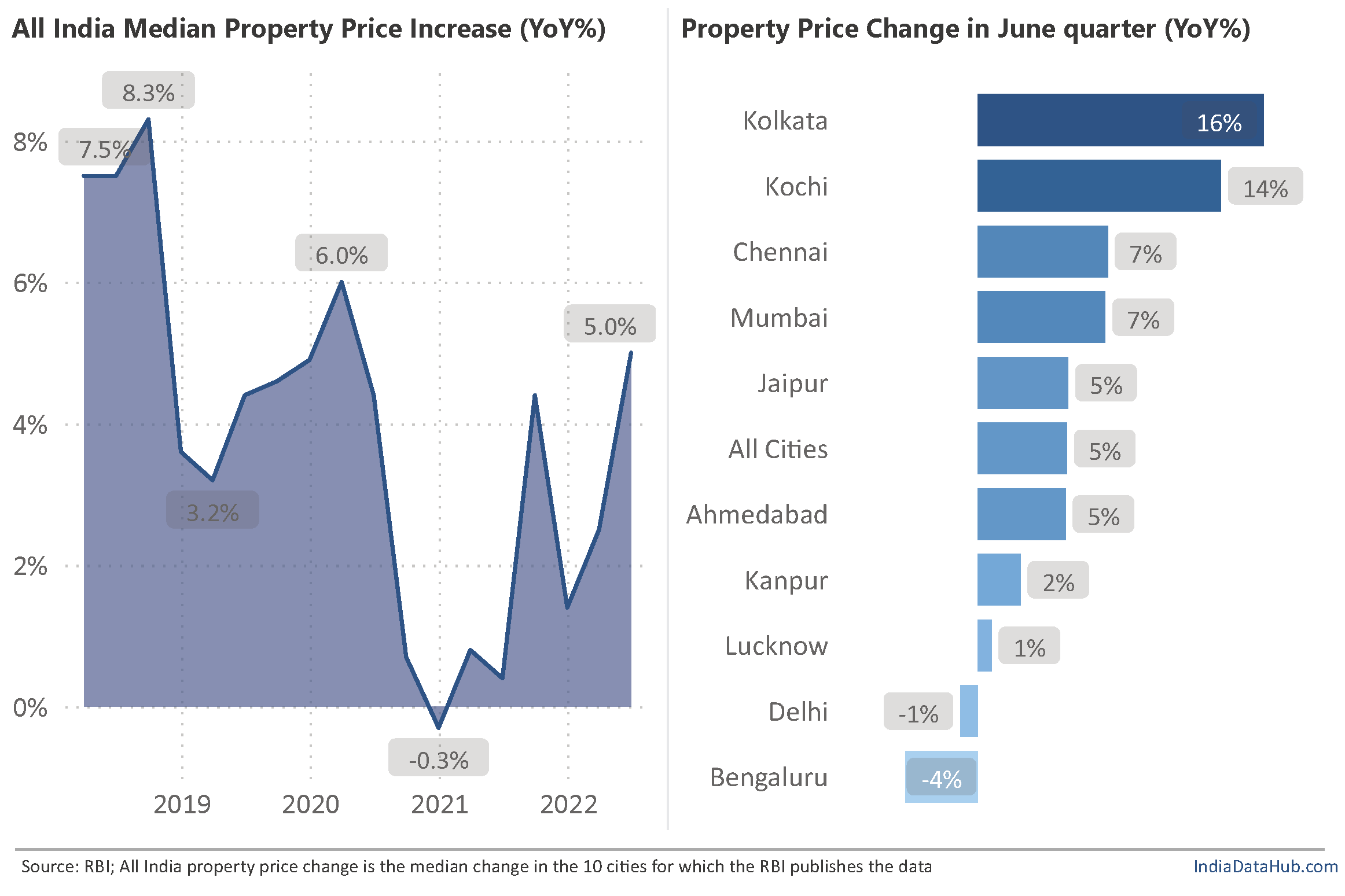

In India, property prices have seen s strong revival in the June quarter. Prices on average have increased by 5 per cent year-on-year across the 10 large cities in the country. The highest rate of growth in over two years.

However, This rebound in property prices is not uniform across the county. Property prices in Kolkata and Kochi have seen a double-digit list while Mumbai and Chennai have increased by 7 per cent year-on-year.

While cities like Dehli and Bengaluru continue to struggle and have seen negative growth.

Want to dig deeper into this issue? We suggest the following reads:

These 183 housing markets could soon see home prices fall 20%: Moody’s

The housing market and home price boom made bigger by investors and Wall Street.

Must Watch 👇

Climate change and its economic impact

As per a working paper by the IMF, an increase in temperature will have uneven macroeconomic effects, with adverse consequences concentrated in countries with hot climates, such as most low-income countries.

According to the World Economic Forum’s Global Risks Report 2020, the top 5 risks over the coming decade, in terms of likelihood, are all climate-related: anthropogenic environmental disasters, climate action failure, natural disasters, biodiversity loss and extreme weather events.

In an unmitigated climate change scenario, model simulations suggest that it will cause a loss of around 7% of output globally and 9% for a low-income country by 2100. The Network for Greening the Financial System (NFGS) group of world central banks puts it even higher at 13%. In a Reuters poll of economists, the median figure for the output loss in that scenario was 18%.

The majority of the world’s poor live in tropical or low-lying regions already suffering climate change fall-outs like droughts or rising sea levels. The NFGS report also projects output losses of above 15% for much of Asia and Africa, rising to 20% in the Sahel countries.

Climate change will drive up to 132 million more people into extreme poverty by 2030, a World Bank paper concluded.

Did you know? The Nobel Prize for Economics in 2018 (William D. Nordhaus and Paul Romer) was awarded for integrating climate change into long-term macroeconomic analysis.

How can it affect the Indian Economy?

Lower Crop Yield: As weather patterns become less predictable uncertainties about monsoonal changes affect farmers' choices about which crops to plant and the timing of planting, reducing productivity. Earlier seasonal snowmelt and depleting glaciers will further reduce the river flow needed for irrigation.

Impact on Livestock: India has the largest livestock population in the world. The animals are used as household capital, particularly in landless households. Heat stress reduces fodder and creates conditions favourable to disease.

Reduced productivity: Workers' productivity is lower on hot days which leads to lower industrial output. Climate change impacts cognitive performance and decreases work hours in sectors requiring laborious outdoor activity like construction.

Energy Crisis: India’s primary energy demand is set to double by 2030 making it the 3rd largest energy consumer behind the US and China, overtaking the EU. The relationship between energy and climate is such that rising temperatures leads to a surge in energy usage.

Impact on Infrastructure: A good and sound infrastructure acts as a multiplier for the economic output. The ever-increasing climate change-induced natural calamities have caused heavy infrastructural damages.

As per the data collected from 70% of the states, extreme weather events like flooding led to the deaths of nearly 6,000 people and damages worth Rs 59,000 crore.

Inequality: Low-income households are more vulnerable to climate change-related economic losses, as they are directly impacted by inter alia rising cereal prices and declining agricultural wages.

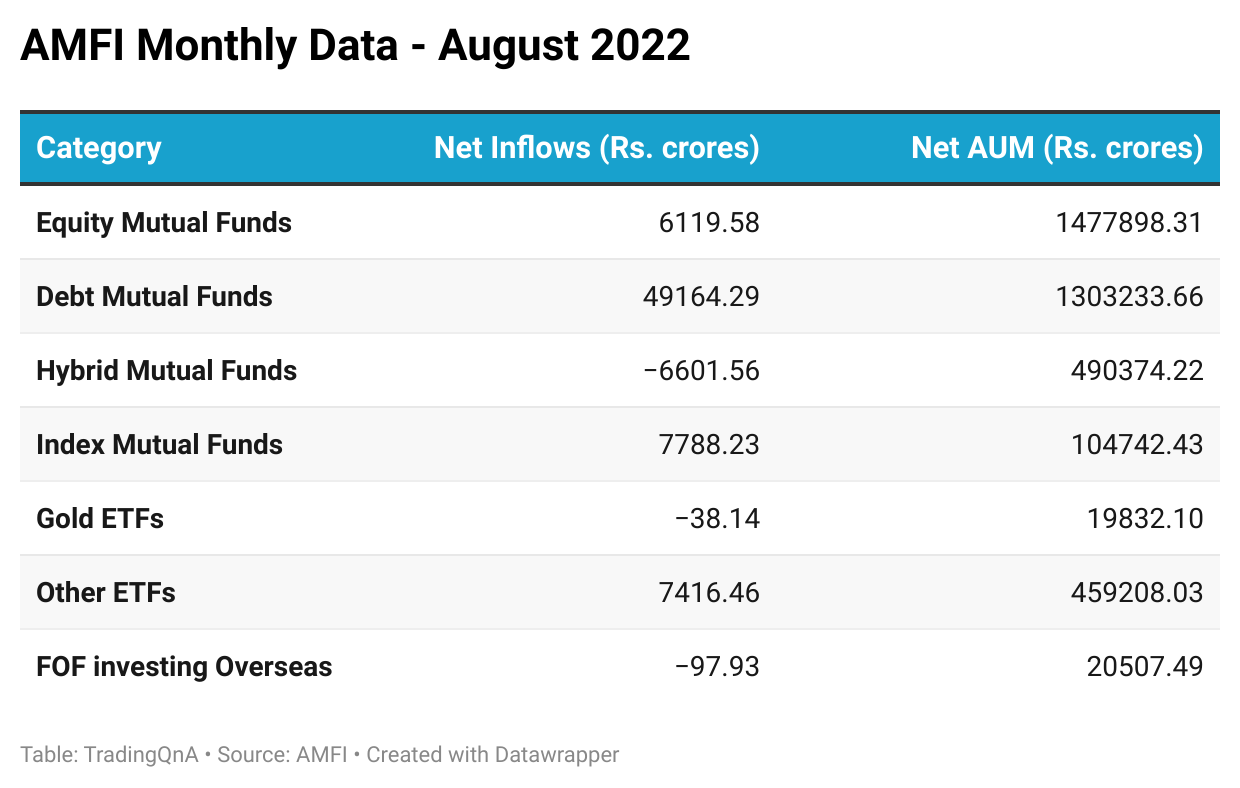

A look at AMFI’s monthly data - August 2022

AMFI (Association of Mutual Funds in India) released data for inflows in mutual funds for the month of August. Here’s a brief look at the latest numbers:

Inflows in the equity segment fell to a 10-month low of Rs. 6119.6 crores in August 2022

The SIP inflows however continued to remain strong, with inflows hitting record highs of Rs. 12,693 crores

A look at how various mutual fund schemes fared in August

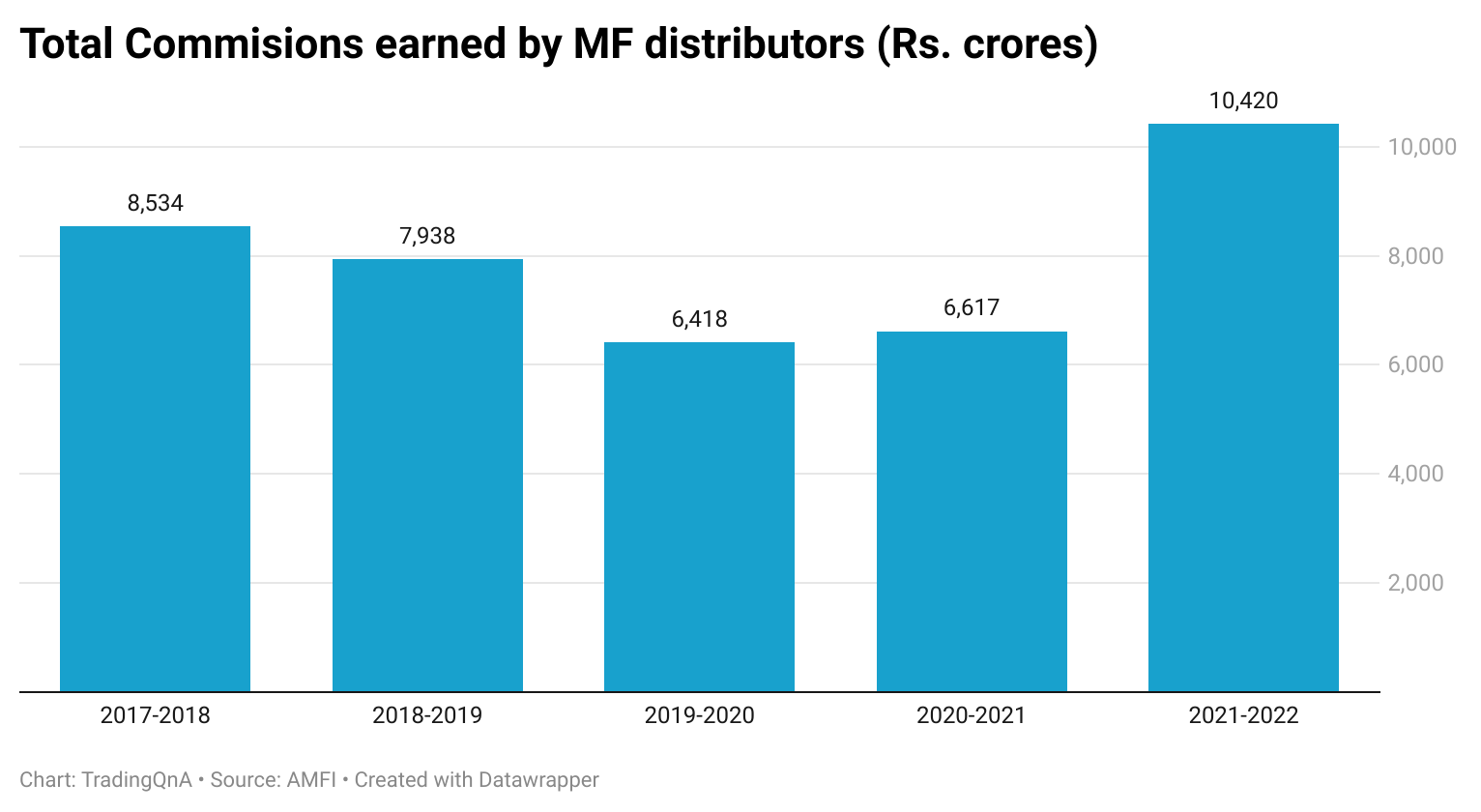

Another report that AMFI released was commissions earned by mutual fund distributors offering regular mutual fund plans. The commissions earned soared to Rs. 10,420 crores in 2021-22 compared to Rs. 6,617.49 crores in 2020-2021.

Top 5 mutual distributors

While the commissions you pay for investing in regular plans of MFs can seem small but these compound over time and as your investment corpus grows. If you're a DIY investor, it makes zero sense to invest in regular funds. You can save on commissions by switching to direct plans, this is what we offer on Coin 😃

Do check out this post on TradingQnA which has more insights.

On TradingQnA

This month on the TradingQnA Book Club we’re reading The Wisest Owl by Anupam Gupta. Anupam is a CA and author and the host of the popular finance podcast Paisa Vaisa. He has over 2 decades of experience as an investment research analyst and a research consultant with leading brokerages and has co-authored with Saurabh Mukherjea - The Victory Project: Six steps to peak potential.

Managing money is easy in theory, but surprisingly hard in practice. Think about pretty much every single thing you need to know about making your personal finances is common knowledge. Yet, only a tiny percentage of Indians actually invest. Of the people that do less than 20-30% of people remain invested in equities after 5 years. In a long-term asset class such as equity, only 2-3 out of 10 people invest for more than 5 years, let that sink in.

It’s not just investing. People also struggle with fundamental questions such as how much to save, what insurance to have, how to deal with financial emergencies etc. The fact that today we have more information than ever also complicates things. This book tries to help these young investors by offering them a framework they can use to create wealth in the long run.

So, grab your copy and let’s read this book together as a group and share our perspectives on various topics covered here 👇

TradingQnA Book Club: The Wisest Owl

On Twitter

Reading Recommendations

Good Enough by Morgan Housel

Sometimes we pretend we’re Greenland sharks, unburdened by threats and able to devote all our resources to a predictable future. But we’re closer to guppies, constantly facing risk from every direction. When you see how much effort and energy are devoted to forecasting the next year or two, then compare it to the constant level of threat and surprise we face, it’s astonishing. Mother nature would shake her head.

Investing in your long-term future is of course great, because the odds that you’ll be around and everyone else will become more productive are pretty good.

But trying to predict the exact path we’ll take to get there can be such a waste of resources.

The Tiger That Was a Wolf: Lessons From Julian Robertson by Frederik Gieschen

One of his key strengths was his ability to attract talented analysts and bring out the best in them. In combination with his exceptional network, he created a research engine to constantly source and test ideas for the portfolio. His greatest legacy are the Tiger Cubs, the diaspora of former analysts who were mentored and put in business by him and who carry on his philosophy.

But even Robertson had to live through moments when it looked like the markets were conspiring against him, when the world was upside down, and everything he’d worked for seemed to be falling apart.

Thank you for reading. Do let us know your feedback in the comments below and share the post if you liked it.

If you have any queries related to trading, investing and anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna