Interest rates, inflation and debt. Where are we headed?

Hello all, welcome to the latest issue of Markets and Macros by TradingQnA.

The future of interest rates

With the US Federal Reserve aggressively hiking rates, the big question is when will the interest rate cycle turn.

An interview with Howard Marks, co-founder of Oaktree Capital Management, can give the answer.

Many think that the low-interest regime was normal and we will go back to normal, but he disagrees. He says that interest rates will largely stabilize around current levels.

Some insights from this interview:

When rates were low, equities were the only option to generate yield—TINA. But now that interest rates around the world have gone up, bonds are looking good—There Are Reasonable Alternatives” (TARA).

Low interest pushed people looking for high returns toward emerging markets. But now that US bonds are yielding ~3.5%, the risk-to-reward equation has to be revisited.

The easy money days are over. Zombie companies who survived by borrowing at low rates can no longer do so. If rates remain high, bankruptcies and defaults will rise—It will be the survival of the fittest.

India has incredible potential if it can get its act together by reducing occupation, bureaucracy, red tape and improve governance.

People have short memory spans. We must look at what has happened over a few decades to understand things with proper context.

He says inflation should ebb away soon, but let's look at inflation from a historical perspective.

A history lesson on Inflation

Historically, once inflation goes up, it can take far longer to return to normal levels than most people realize.

Here are a few interesting factoids about inflation from a recent paper by Rob Arnott and Omid Shakernia of Research Affiliates based on the study of 14 OECD developed-economy countries from 1970-2022:

An inflation jump to 4% is often temporary, but when inflation crosses 8%, it proceeds to higher levels over 70% of the time.

If inflation is cresting, inflation levels of 4 or 6% revert by half in about a year. If inflation is accelerating, 6% inflation reverts to 3% in a median of about seven years, threatening an extended period of high inflation.

Reverting to 3% inflation, which we view as the upper bound for benign sustained inflation, is easy from 4%, hard from 6%, and very hard from 8% or more. Above 8%, reverting to 3% usually takes 6 to 20 years, with a median of over 10 years.

Chart of the week: $300 trillion Global debt

S&P Global recently published a report outlining how the global debt is currently more than the pre-global financial crisis (GFC) peaks.

Source: SNP Global

Indians are falling into a debt trap

“In recent years, Indian banks appear to have displayed herding behavior in diverting lending away from the industrial sector towards retail loans. Empirical evidence suggests that a build-up of concentration in retail loans may become a source of systemic risk”

- RBI Report on Trend and Progress of Banking in India, 2021-22

In 2016 banks started growing their retail loan books to offset the impact of corporate NPAs. Since 2016 the repo rate has also been under 7% and fell until May last year. As a result, in September 2021, outstanding retail loans surpassed industry credit for the first time since 2007.

It turns out that the average Indian is now borrowing to finance consumption.

The stigma around debt is withering away. Social media and hustle culture induce greed and aspirations to buy a big house, a big car, or the latest smartphone. It doesn’t matter if it is on loan.

Buying things you don't need with money you don't have is not sustainable.

An example from an Economic Times article highlights what I am talking about:

“Parmar gives an example of a client who came to his company’s platform with debt of over INR87 lakh. The client had over 37 loans of which 28 were app loans. Despite having a job, which paid over INR2 lakh, the interest cost on these loans had far outstripped the client’s Earnings.”

The current situation has been summarized below

“Over-abundance of credit and lack of financial education is creating a huge debt trap. The household savings rate has consistently fallen, wage growth has not kept pace with rising credit or soaring inflation for that matter. So, macroeconomically, we are moving into a credit-driven economy”

- Ritesh Srivastava, founder of India's first debt-relief platform FREED.

Gold loans rise as the vulnerable borrow to finance their consumption needs

Households’ debt levels have been increasing since the pandemic. The quantum of gold loans taken by Indian households grew by 194% between October 2019 and 2022.

It is a dire situation if Indians have to start pledging/selling their gold to meet their expenses.

Much like the pincer movement from Tenet, we are seeing debt balloon from both ends.

Unnecessary consumption loans by the well-to-do and loans for survival by the underprivileged.

The art and science of spending money

I hope you guys aren't doing what we read about above and are not revenge spending either.

In a blog post, Morgan Housel talks about revenge spending.

“After Covid lockdowns there was the concept of “revenge spending” – a furious blast of conspicuous consumption, letting out everything that had been pent up and held back in 2020.

Revenge spending happens at a broad level, too. The most stunning examples I’ve seen of this are wealthy adults who grew up poor – and were heckled, bullied, and teased for being poor as kids. Their revenge spending mentality can become permanent.”

I like him for his ability to break down people’s relationship with money into very simple and understandable language.

In his book, he calls money “the greatest show on earth” due to its ability to reveal people’s character and values. People’s investments are usually hidden from view but how they spend is visible. What it shows about who you are can be even more insightful.

I sincerely recommend that you read this blog post to understand your relationship with money and become better at managing it.

While you are at it check out this money formula by Antony Isola.

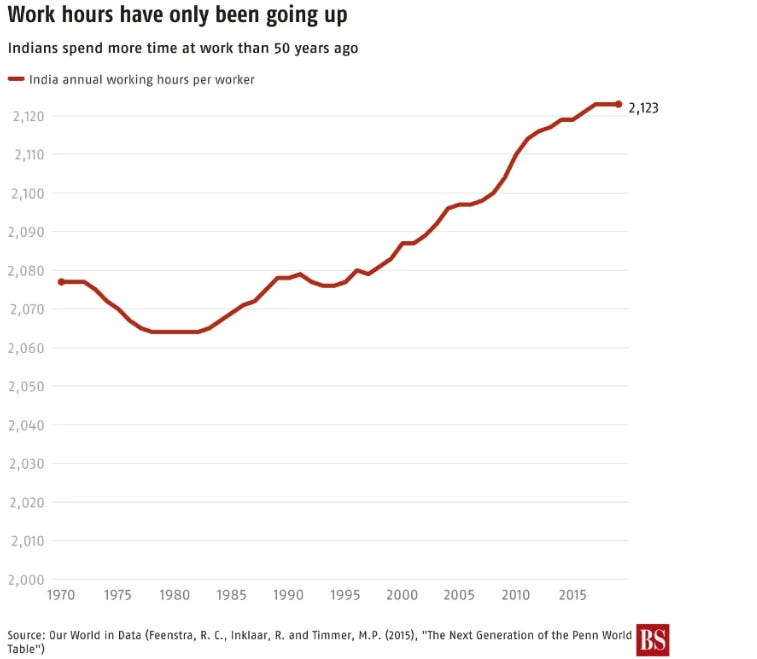

India’s growing work hours

An article points out that Indians want to work for longer hours. An ILO report shows only 4.4% of Indians feel over-employed. Around 47.1% of workers would like to work longer hours!

Indians are among the most overworked workers across the world and earn the lowest minimum statutory wage in the Asia-Pacific region, excluding Bangladesh, as per another ILO report.

Low incomes in developing countries make people work long hours to make ends meet (a government report suggested that around 90% of Indians earn less than Rs 25,000 a month).

Maybe the work hours will go down as people become more secure as India becomes wealthier.

Prosperity will have to precede any hope of a work-life balance.