India is a bright spot in a gloomy world

Issue #9

Hey folks, welcome to the latest issue of Markets and Macros by TradingQnA. In this issue, we take a look at:

Stanley Druckenmiller's conversation at the Sohn conference

State of the global economy—updates from IMF, WTO, and the World Bank and more…

Written by Meher, Bhuvan, Abhinav, Esha, and Shubham

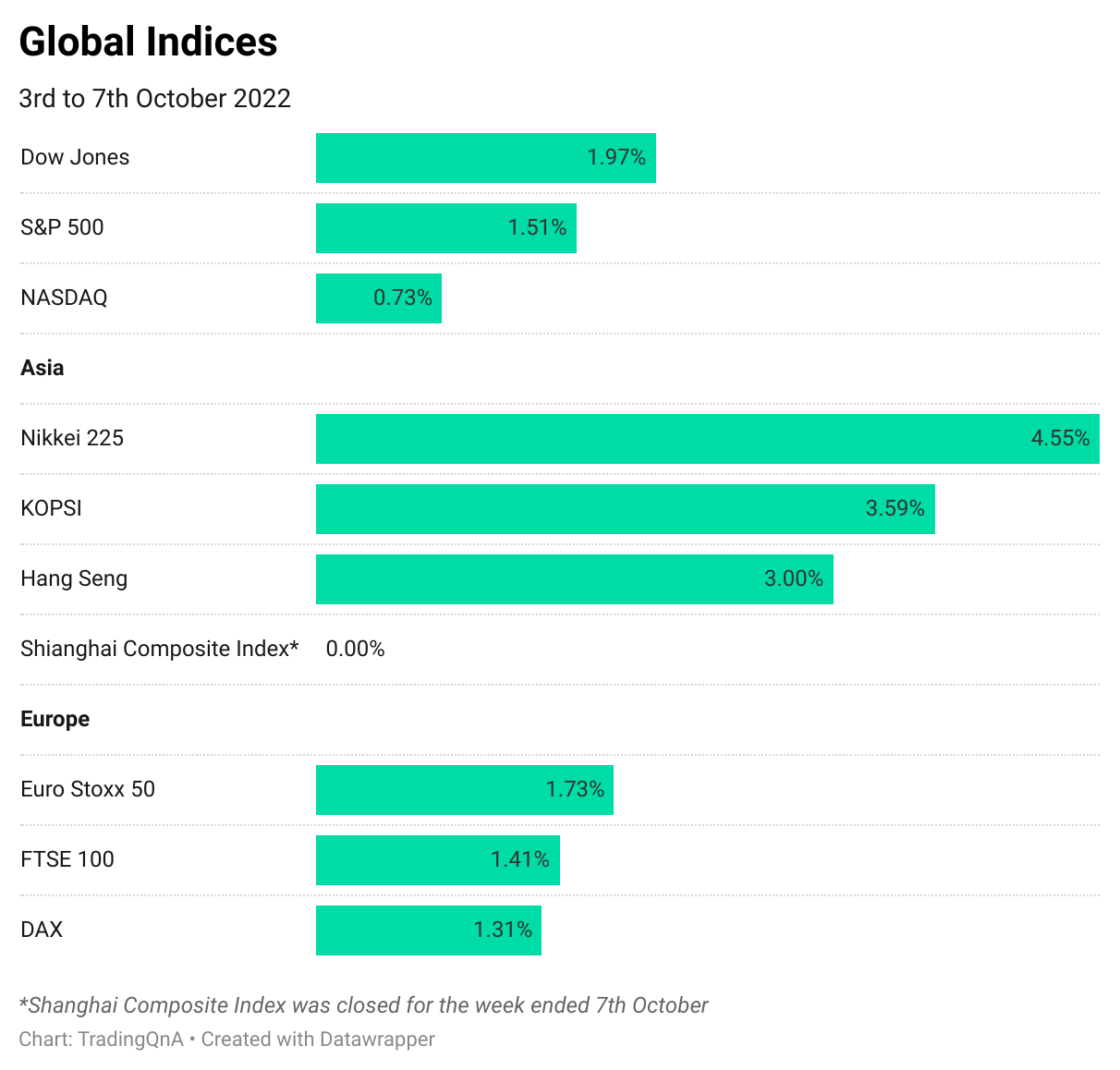

Weekly Market Wrap

A quick look at what the markets were up to in the week;

After declining for three consecutive weeks, markets closed this week in green. Both Nifty and Sensex surged around 1.3% each. While the MidCap index was up 2.41% and SmallCap 2.59% for the week.

Indian Rupee continued to depreciate against the US Dollar to lows of Rs. 82.4150. Prices of Brent Crude Oil were up over 15% for the week following OPEC+ production cuts.

US markets managed to end the week in the green despite tanking between 2.1% to 3.8% on Friday. Apart from the Shanghai Composite Index which was closed for the week on account of Chinese National Day, all major indices managed to close the week in gains.

Stanley Druckenmiller on investing and the US economy

Stanley Druckenmiller was at the Sohn conference in June and spoke with John Collison, the co-founder and CEO of Stripe. In case you don’t know, Stanley is a legendary investor and an all-time great, and he used to work with George Soros until he went solo. He’s had an amazing track record and has never had a down year in his 3+ decades of investing.

The conversation was absolutely brilliant, and we decided to summarise it.

On inflation and the US economy

Once inflation gets above 5%, it’s never come down unless the fed funds rate (interest rates) have gotten above the CPI. Since the CPI is 8%, that would call for the fed funds rate to be above 8% which I frankly don’t think we’ll get there because of the extent of the asset bubble and the damage that would be done.

If you are predicting a soft landing, you are going against decades of history. It could happen, anything is possible, but I don’t think it’s probable. I’m strongly assuming a recession sometime in 2023.

On his approach to the analysis of the markets and economy

I don’t use what traditional economists use to predict the economy, like employment and a bunch of top-down statistics. I learned that the inside of the stock market gives a better picture of economic activity.

Stocks tend to lead the fundamentals by somewhere between 6-12 months. You can look at industries that lead, and lag the economy to get a better picture. For example, housing is a leading economic indicator while retail and capital goods lag.

The other signal I found quite prescient for markets is the bond market. But unfortunately, it has not signalled anything in the last 10-11 years as the central banks took it upon themselves to manipulate bond prices.

In the mid-70s, I started in equities. I also learned particularly in bear markets that I had to move into bonds, commodities, and foreign currency.

The biggest challenge currently—It has something to do with my dysfunctional personality—is that I’ve always made even higher returns in bear markets than bull markets. All I did was pretty much ignore equities, take them off the table, buy bonds, and treasuries and go home in the past.

I’ve never been presented with a cocktail where we have 8% inflation, you think the economy might weaken, and bond yields 3%. It's an analogue with no precedent in history.

Bonds have been my go-to asset in terms of a recessionary bear market atmosphere. They may work, but things can be different this time around, as we’ve never had negative interest rates with 8% inflation. Investing is an art form, and you have to constantly innovate and not just be a slave to past models.

In bear markets, macros make all their money because that’s when you have the biggest bond and currency moves, and it really moves in chaos. So, a macro investor sort of roots for chaos.

I have a bearish bias and I know it. One of my jobs is to manage myself and know that bias exists in me.

My philosophy is completely contrary to what they teach you in business school, “If you are highly diversified, you have less risk than if you are highly concentrated” - I don’t believe in this at all.

On crypto

If I think we're going to have an inflationary bull market I'd want to own bitcoin more than gold and if I thought we're going to have a bear market you know stagflation type thing I'd want to own gold.

Watch the full conversation 👇

State of the global economy

One of the topics that we’ve written a lot about so far is the state of the global economy. This is because the world has suddenly become a much scarier and unpredictable place. If you had told me in 2019 that we’d be seriously considering nuclear threats, I would’ve laughed, yet here we are. I can’t remember the last time the global economy was in such a state of flux.

As the Russian invasion of Ukraine takes a new turn, as inflation remains sticky, and the Fed continues hiking, things are becoming increasingly uncertain. Recession probabilities are among the highest they’ve ever been. Sentiment has also been worsening, which means the bearishness could lead to a recession becoming a self-fulfilling prophecy.

Despite tightening financial conditions, it’s remarkable that nothing has broken so far. But the first sign of strains seems to be emerging. Last week, the Bank of England had to intervene to stop the UK bond market from disintegrating. The liquidity in the US treasury market, which is the largest and the most important bond market on the planet, is getting worse. The probabilities of debt defaults are increasing among the most vulnerable countries as the dollar strengthens and energy prices remain elevated despite the recent moderation.

This week, the IMF, World Bank, and the World Trade Organisation published updates that paint a depressing picture of the global economy. Here are some highlights:

Excerpts from the IMF’s update

Soaring energy prices, food prices, and rising interest rates are affecting global growth.

Europe is suffering due to Russia cutting off gas supplies. Chinese growth is faltering due to its zero-COVID policy and a property market that’s in deep trouble. The growth momentum in the US is slowing as inflation is eating into people’s incomes, while higher interest rates are leading to lower investments.

World economic growth projection has already been revised three times to 3.3% for 2022 and 2.9% for 2023. The growth for next year will be downgraded again.

Countries accounting for about one-third of the world economy will see at least two consecutive quarters of contraction this or next year.

Overall, we expect a global output loss of about $4 trillion between now and 2026. This is the size of the German economy—a massive setback for the world economy.

More than a quarter of emerging economies have either defaulted or had bonds trading at distressed levels, and over 60 per cent of low-income countries are in—or at high risk of—debt distress.

We need to step up our efforts to counter acute food insecurity—which is now affecting a staggering number of people: 345 million.

World Trade Organisation (WTO) on the global economy

WTO predicts a merchandise trade volume growth of 3.5% in 2022 but only 1% in 2023 vs. a previous estimate of 2.4%.

Higher inflation and higher interest rates in the US and high energy prices in Europe are squeezing household incomes, leading to slower growth.

WTO is projecting world growth of 2.8% in 2022 and 2.3% in 2023 which is lower by 1%.

Based on the current assumption, world trade growth could be in the range of 2% to 4.9%. In the case of downside risks, it could be as low as -2.8%, and in the case of upside surprises, it could be as high as 4.6%.

Merchandise exports and imports by region, 2019Q1-2023Q4

Imports by the Commonwealth of Independent States (CIS) dropped by 21.7% in Q2 2022. Imports by other resource-rich regions such as South America, Africa, and the Middle East rose on the back of higher commodity prices, which allowed them to import more. Asian imports are faltering with a growth of just 0.7%.

RWI/ISL global container throughput index, January 2015-July 2022

The RWI/ISL container throughput index tracks global goods trade quite closely. Although the index remained near its all-time high in July, it has been mostly flat since October 2020. Throughput of Chinese ports dipped in the spring due to pandemic-related lockdowns, but traffic rebounded again after these measures were relaxed. The decline in China was partly compensated by increased container handling at U.S. ports, which had previously experienced severe congestion. Overall, the index suggests continued stagnation in merchandise trade.

India-specific highlights from the World Bank fall update

Services-oriented economies like India may grow reasonably despite the global economic headwinds.

Economic activity in India has recovered faster than the rest of the world on the back of stronger economic growth, foreign reserves, and a restrained monetary policy.

Tourist arrivals to India are recovering but still lower than pre-pandemic levels.

The effects of supply chain issues can still be seen, but there are signs of improvement.

Indian employment growth remains slower than the rest of the world ex-Asia. Demand for rural employment (MNREGA) remains high,

Consumption growth in high-income households has recovered faster, while it remains quite weak among low-income households.

Depreciation of the rupee against the dollar and higher oil have contributed to higher inflation.

After a record FPI outflow of $29.7 in the first half of 2022, foreign investors have become net buyers since July.

Indian markets have recovered as foreign investors turned net buyers, along with strong buying from domestic investors.

On Twitter

📖 Reading Recommendations

The Inflation Game: War, Peace, and the Perils of Central Banking by Mark J. Higgins

“The descent is always more sudden than the increase; a balloon that has been punctured does not deflate in an orderly way.” — John Kenneth Galbraith

The Fed is in a difficult position: It must prepare the public for the impending economic pain but without inciting a panic. The reality, however, is that a recession is now a virtual inevitability. Why? Because the Fed can only use blunt policy tools to reverse what have become extreme economic conditions. This makes it extraordinarily difficult to engineer a soft landing.

Continue reading…

🎧 Listen to

That’s it from us today. Hope you loved reading the latest issue, do let us know your views in the comments section below. And do like and share 😃

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna