China just sneezed again, will the world catch a cold?

Issue #3

Hey folks, hello and welcome to the latest issue of the Markets and Macros by TradingQnA. In this issue, we take a look at:

Is the Chinese economy in trouble?

State of the global economy and inflation

Timeless Principals of Investing with Sankaran Naren and more…

Written by Shubham, Abhinav, and Meher.

🇨🇳 Is the Chinese economy in trouble?

When China started its economic reforms program in 1978, it was one of the poorest countries in the world. Today, it’s the second-largest economy and the factory of the world, accounting for 15% of global exports and lifting over 800 million people out of poverty. Over the last decade, China has also been a key engine of global growth contributing one-third to the global GDP.

This Chinese miracle was fuelled by massive Govt investments and productivity gains. The investment-led growth meant a rapid growth in the total debt to GDP ratio from 126% in 2000 to 268% in 2022. Non-financial debt rose from 96% to 159% while household debt rose from 12% to 62% in the same period.

China is a managed economy where the Govt exerts a tremendous amount of control. Whenever the Chinese economy was in trouble, the Govt. would stimulate the economy through monetary and fiscal measures through state-owned enterprises, banks, and local governments. We saw this in 2008 and in 2013 and 2016. Market participants used to jokingly call Chinese officials the plunge protection team.

Fast-forward to 2022, the Chinese economy is once again in trouble. This time, it’s the property sector that’s the source of trouble.

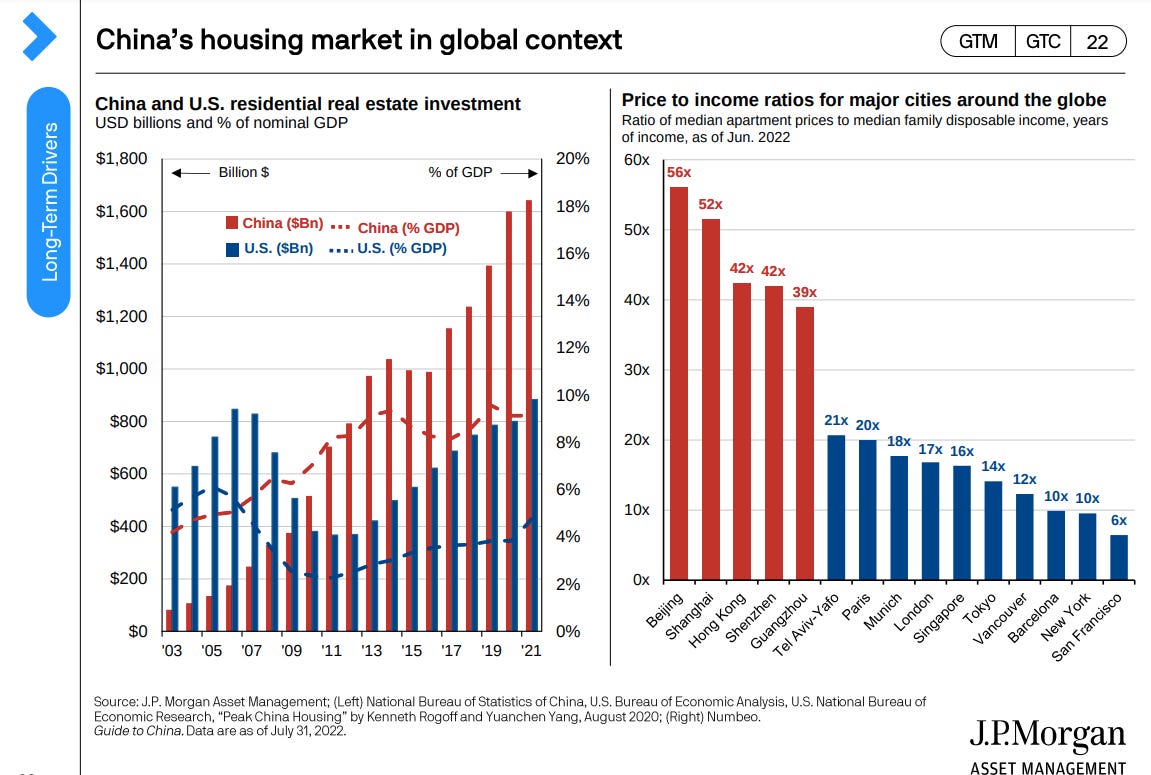

Why is the Chinese property sector important?

It accounts for 25-30% of the Chinese GDP.

Investment is one of the growth engines of the Chinese economy, accounting for 43% of its GDP with real estate being a huge contributor to fixed investment.

Property-related loans account for 25-30% of total loans.

Over 60% of Chinese household wealth is in real estate.

What’s happening in the Chinese real estate market?

Housing is the preferred asset for investment in China. The homeownership rate is also among the highest in the world at 90%.

As China urbanized rapidly and incomes rose, housing demand boomed. Developers took on huge debt to finance their construction activities. This led to a steady rise in property prices so much so that several Chinese cities are among the costliest in the world measured by price-to-income ratio.

But soon, housing became a speculative asset in China.

The interest coverage ratio of the 21 largest Hong Kong-listed developers fell from about 1.47 to 0.94. Interest coverage below 1 is typically a bad sign.

To curb excessive leverage, regulators introduced a policy called three red lines which imposed leverage limits on developers.

At the same time, China was following the Zero-Covid policy of mass lockdowns and testing. This was because China has an aging population and low vaccination rates among the elderly. Moreover, Sinovac—the domestically manufactured vaccine is less effective than other mRNA vaccines.

About 41 Chinese cities which account for a large chunk of its economy have varying degrees of lockdowns and restrictions, leading to serious economic damage.

Given all these issues, Chinese economic growth has been flagging. The economic data released in August paints a worrying picture of retail sales, industrial production, and investment. The IMF has downgraded Chinese growth to 3.3% down from 4.4%. Consumer confidence has cratered, and credit has also contracted across the board.

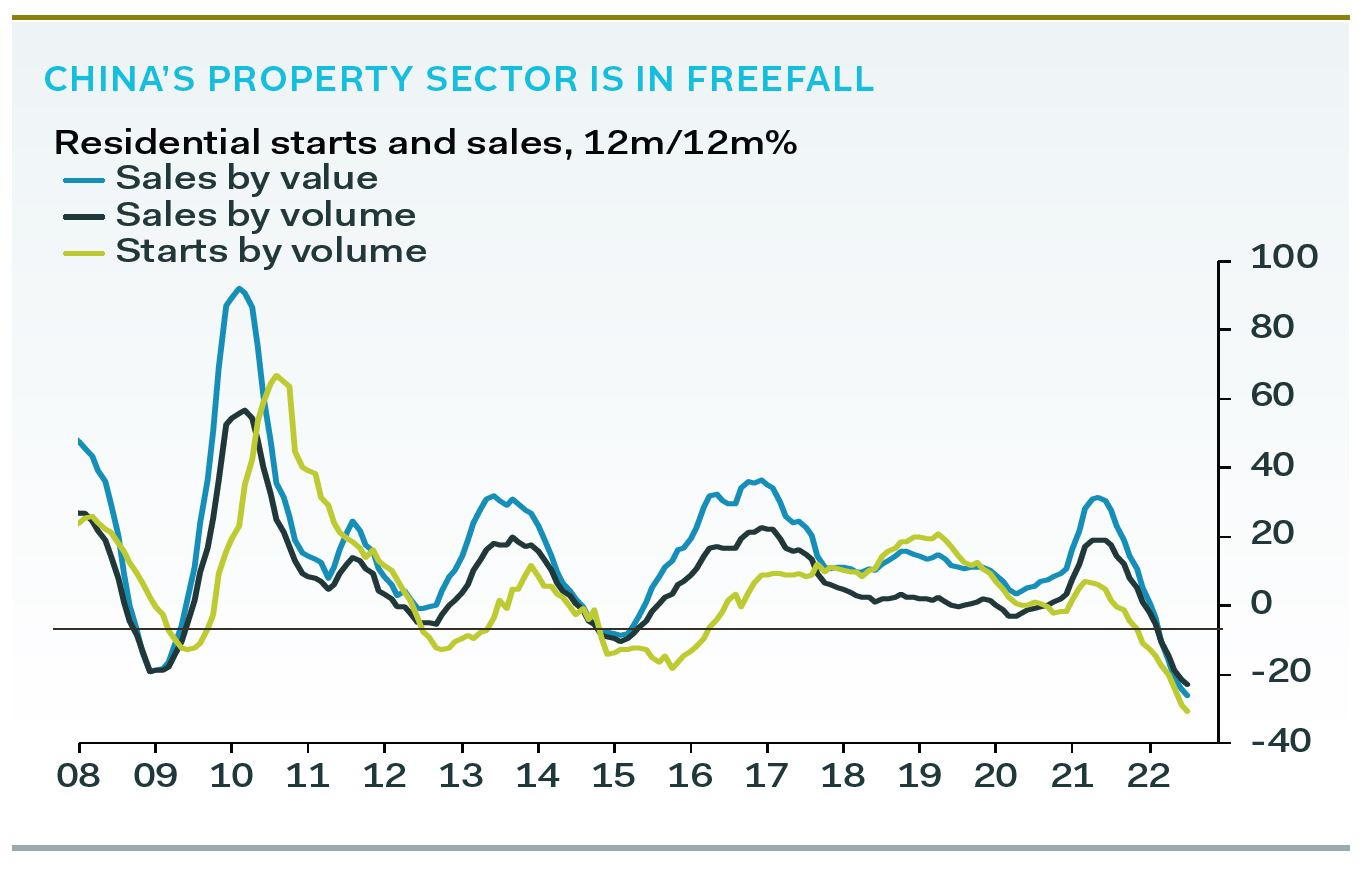

Chinese property prices have fallen by about 30-40% for 11 straight months. The property sector also is a significant source of employment and also has other downstream effects in the form of demand for commodities like steel, coal, aluminium, copper, etc.

The three red lines policy and falling property sales have led to a liquidity crunch for the developers. They are unable to borrow while at the same time advance payments from new sales, which were a huge source of funding for developers, have dried up.

Adding to the woes, investors in over 300 projects have gone on a mortgage boycott and stopped making interest payments.

Is China crashing?

China has cut rates twice in a span of weeks and unveiled several small bailout and support packages to support the real estate market. But these measures are half-hearted at best.

Given the significant corporate leverage, especially in the property sector, China affords to let housing prices collapse. But demographic issues, declining urbanization, falling incomes, and rising unemployment will act as secular downward forces on housing prices.

At the end of the day, the Chinese government and the people have a tacit deal—In return for steady growth, the people accept authoritarianism.

But the Zero-COVID policy, rising youth unemployment of 20%, and falling property prices threaten this social contract. If it gets worse, the worry for The Chinese Communist Party (CCP) is the probability of people revolting.

Adding to the problems, China is facing the most severe heatwave in recorded history. This is affecting everything from key industries to agriculture.

Soaring temperatures and falling rain have led to the water levels in the key Yangtze river hitting a record low. This has led to a sharp decline in hydroelectricity leading to the closure of factories such as Toyota and Foxconn in key industrial cities like Sichuan.

(Source: Pantheon Macro Twitter)

What does it mean for the global economy and markets?

The consensus at this point is that this is unlikely to lead to contagion, but will cause a slowdown. The mortgage boycotts aren’t a big headache for the banking system.

Given the significant debt, China is unlikely to unleash large-scale stimulus programs, the likes of which we saw in 2008. So, we are unlikely to see a quick resolution of this anytime soon.

Having said that, we’ve seen China go through serious challenges in the past and this won’t be the last. Though China has to make some painful adjustments to reduce the leverage in the property sector; this is unlikely to be a serious overhang for the markets.

The only silver lining is that falling Chinese importance can help cool the global inflationary pressures to some extent. But a slowing China won’t help the rising inflationary probabilities around the world.

Did you know?

The MSCI China Index (USD) has essentially given 0 returns since its inception;

Diver deeper

So has the China bubble burst? We’ve been here before.

Michael Pettis is one of the most authoritative voices on China. His analyses are a must-read to get a sense of what’s happening in China.

🆙 State of the Global economy and inflation

An overview of some interesting facts, figures, and opinions related to the global economy.

(Source: Global Data Business Fundamentals)

In 15 of the 34 countries classified as Advanced Economies (AEs) by the IMF’s World Economic Outlook, 12-month inflation through December 2021 was running above 5%. Such a sudden, shared jump in high inflation has not been seen in more than 20 years.

In many ways, emerging markets and developing economies (EMDEs) have been the worst hit. 78 out of 109 EMDEs have annual inflation rates above 5%.

This inflationary spike comes at a time when EMDEs are dealing with a toxic cocktail of falling incomes, rising food and commodity prices, food shortages, and severe supply chain disruptions. Add to this, a strong dollar that’s making it harder for them to service their debt.

For EMDEs, currency depreciation (due to lower foreign capital inflows and sovereign credit rating downgrades) has contributed to inflation among imported goods.

Since inflation in EMDEs is more prone to currency fluctuations compared to AEs, the effects of exchange rates on prices are more pronounced. As the AEs currencies lose value against the dollar, the prices of imported goods increase stressing the already under pressure AEs. Moreover, their exports also become less profitable for them.

Food inflation is bad for low-income countries, given that consumption is the largest component of household incomes. This is further compounded by high energy prices, which is another big component of household expenditure. Food inflation however has shown signs of easing, something that we covered in our previous newsletter.

Average inflation numbers mask the wide dispersion in inflation impact. Here’s a chart of CPI inflation and sub-components of G20 countries and a few other countries.

Is tightening a solution?

The US has started tightening, but some economists believe it’s far behind the curve with the Fed Funds rate at 2.25-2.50% and CPI inflation running hot at 8.5%. The fear is over the spectre of a 1970s-like inflationary shock when inflation hit 14%. Paul Volker, the Fed chairman back then, hiked the Fed Funds rate to 22%.

This current rate hike cycle coupled with the supply chain disruptions and the Russia-Ukraine war doesn’t bode well for the most vulnerable EMDEs.

In March 2022, the World Bank warned of a wave of defaults among the poorest and vulnerable EMDEs stating that Close to 60% of the poorest countries were already in debt distress or at high risk of it. Debt-service burdens in middle-income countries were at 30-year highs.

This is something we posted on Twitter earlier as well.

While we talk about the USA, it is worth noting that inflation in Britain jumped 10.1% in July from a year earlier, the fastest pace in four decades. It now has the highest inflation rate among the G7 countries. It is being projected that UK inflation could hit 18.6% as gas prices surge and it faces an even bigger problem than the USA.

Europe is currently facing an energy crisis, elevated by Russia's invasion of Ukraine. The entire European continent is operating at electricity prices above €600 per MWh, which is likely to worsen as winter approaches.

This thread provides a detailed rundown on the European energy crisis 👇

You can also take a look at a few interesting charts depicting how inflation is changing the economic script compiled by McKinsey and Co.

On TradingQnA

In the latest episode of the Zerodha Educate podcast, we had a really special guest. We caught up with Sankaran Naren, one of India’s most admired and well-known fund managers, and the chief investment officer (CIO) of ICICI Prudential AMC.

In this conversation, we spoke about his 3-decade career in the Indian markets as an investor, broker, and fund manager. He’s perhaps best known for his contrarian style of investing that has helped him create immense wealth for investors.

You can listen to this episode along with the transcript here 👇

Zerodha Educate Podcast: Timeless Principals of Investing with Sankaran Naren

On Twitter

ICAI in its latest guidelines provided some good news for options writers, clarifying that when calculating turnover to determine tax audit only the profit or loss has to be considered. No need to separately add premium received when writing options as turnover. If you have got any questions regarding this, you can post them on this thread on TradingQnA 👇

ICAI 2022 guidelines - No need to consider premium received as turnover

Reading Recommendations:

Long tails drive everything. They dominate business, investing, sports, politics, products, careers, everything. Anything that is huge, profitable, famous, or influential is the result of a tail event. Most of our attention goes to things that are huge, profitable, famous, or influential. And when most of what you pay attention to is the result of a tail, you underestimate how rare and powerful they really are.

No matter what you’re doing, you should be comfortable with a lot of stuff not working. It’s normal. This is true for companies, which need to learn how to fail well. It’s true for investors, who need to understand both the normal tail mechanics of diversification and the importance of time horizon, since long-term returns accrue in bunches. And it’s important to realize that jobs and even entire careers might take a few attempts before you find a winning groove. That’s how these things work.

Read 👇

Tails, You Win by Morgan Housel

It is often said that a useful measure of happiness is the gap between reality and expectations. A similar approach can be adopted for identifying poor investment decisions. They tend to occur when our expectations of what we are capable of exceed the reality. This miscalibration leads us into activities and behaviours that we really should avoid.

An insightful read on some of the most significant examples of what we think we can do, but probably can’t. Read 👇

What Do Investors Believe They Can Do But Can’t? by Joe Wiggins

Thank you for reading. Do let us know your feedback in the comments below and share the post if you liked it.

If you have any queries related to trading, investing and anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna