Challenges and Prospects of the Indian Corporate Bond Market

Issue #8

Hey people, welcome to the latest issue of Markets and Macros. In this issue;

Challenges and Prospects of the Indian Corporate Bond Market

Highlights from RBI’s MPC meeting

The inflation nightmare and more…

Written by Abhinav, Bhuvan, Esha, Meher, and Shubham

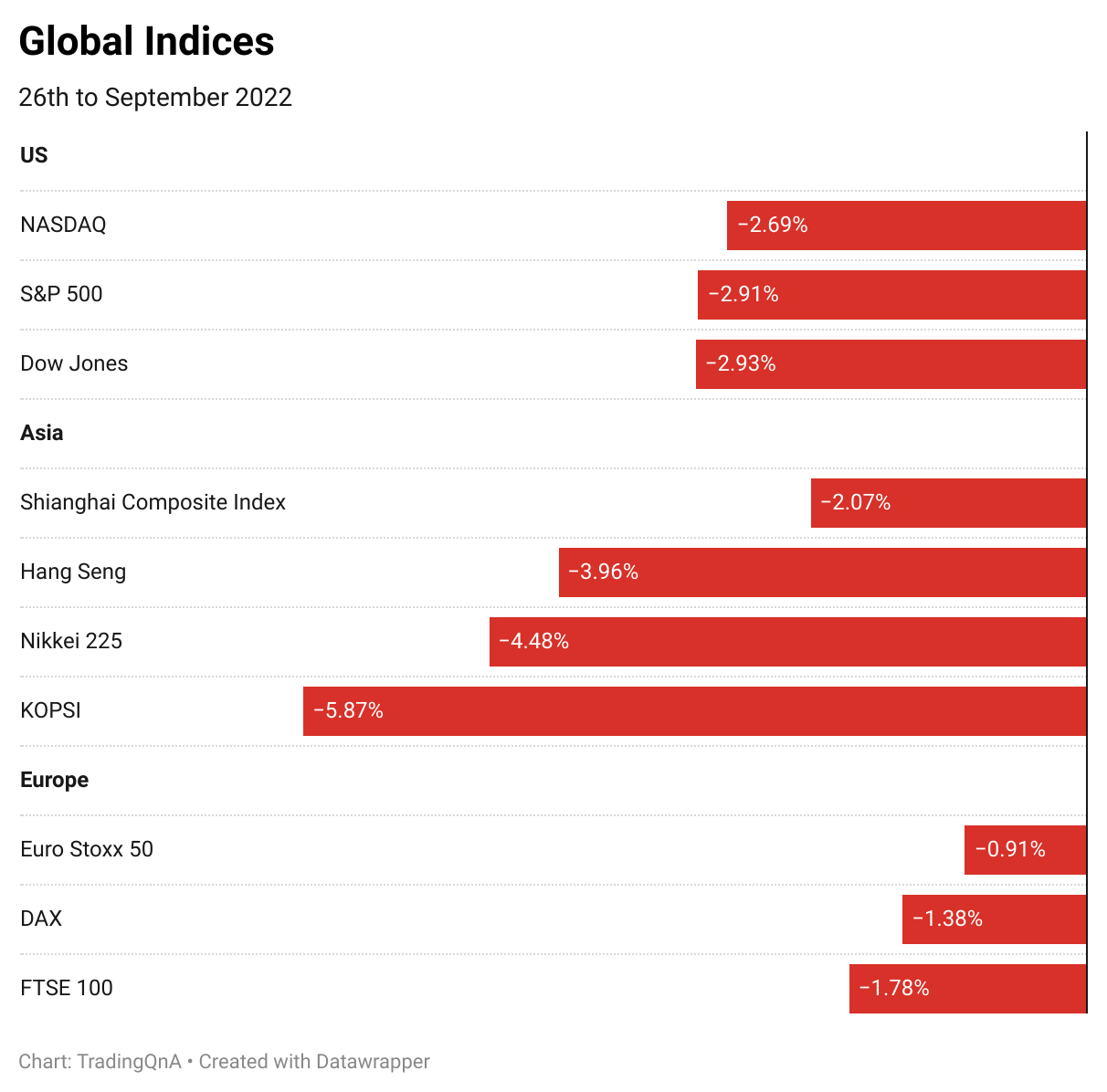

Weekly Market Wrap

A brief overview of market performance in the week ended 30th September 2022;

Challenges and Prospects of the Indian Corporate Bond Market

In August 2022, Rabi Sankar, the Deputy Governor of RBI, delivered an address on the state of the Indian corporate bond market at the Bombay Chamber of Commerce & Industry. Here’s a summary;

Why do we need a corporate bond market?

Just like a vibrant and deep government bond market can help sovereigns raise money easily to reduce borrowing costs, a deep and liquid corporate bond market can help companies raise money easily. It also helps spread risks in the system away from banks, which are the biggest source of capital for companies. Not a budget speech goes by without a mention of the need to deepen the Indian corporate bond market.

In August 2022, Rabi Sankar, the Deputy Governor of RBI, delivered an address on the state of the Indian corporate bond market at the Bombay Chamber of Commerce & Industry. The speech was a concise summary of the state of the Indian corporate bond market—a few highlights.

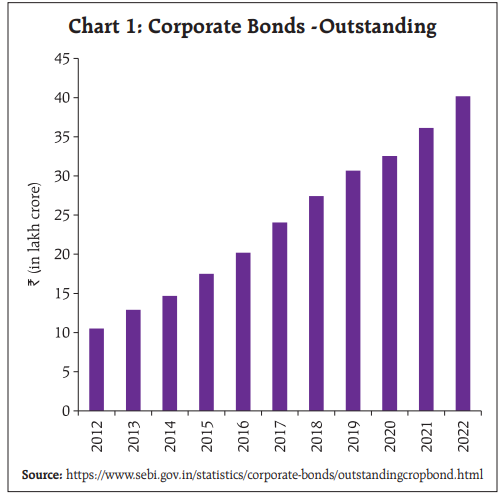

The Indian corporate bond market

Outstanding corporate bonds rose four-fold from Rs. 10.51 lakh crore by the end of FY 2012 to Rs. 40.20 lakh crore by the end of FY 2022.

Annual issuances during this period have increased from Rs. 3.80 lakh crore to close to Rs. 6.0 lakh crore.

The ratio of bond issuances by non-financial entities to non-food credit increased from 0.09 in 2010-11 to 0.50 in 2020-21.

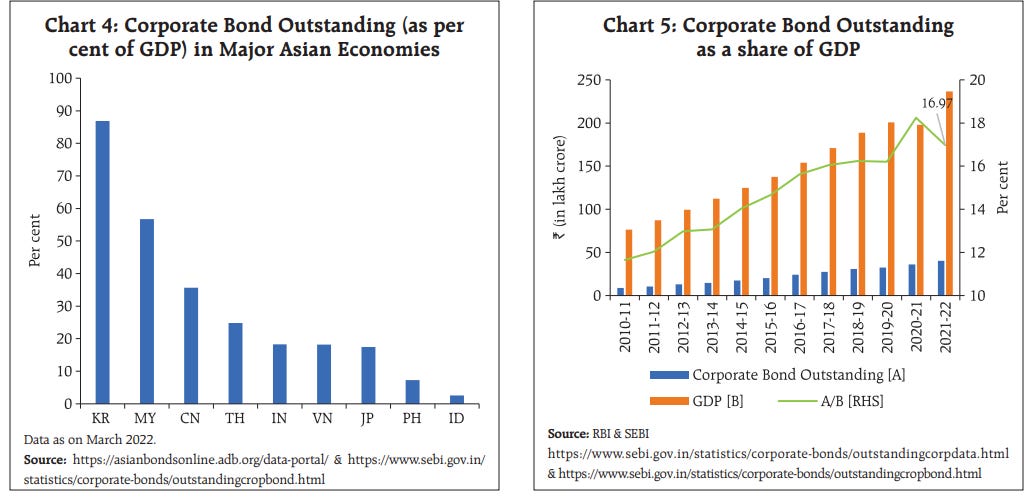

These are still early days. The Indian corporate bond market, as measured by bonds outstanding as a percentage of GDP, is small compared to other major Asian emerging market economies such as China, Malaysia, and Korea. However, it is growing steadily and reasonably, given the traditional bank dominance.

What’s driving the growth of the corporate bond market?

Issuances by new types of entities like REITs and InvITs.

SEBI guidelines on the issuance of municipal debt bonds have enabled market-based financing of infrastructure projects.

A budding albeit nascent market for distressed corporate debt.

Secondary Market

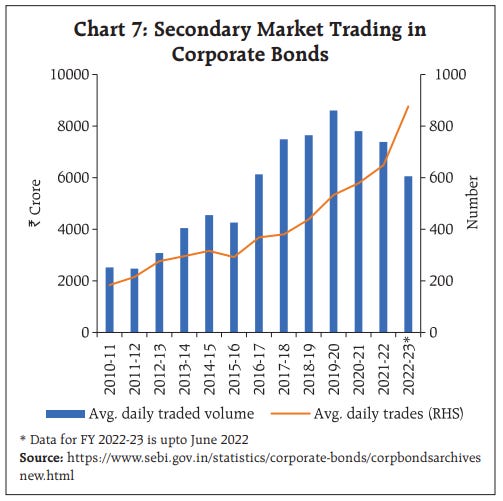

An important metric to assess a corporate bond market is the development of secondary bond markets, and secondary market trading volumes have grown over the years.

The total settled value of secondary market trades during FY 2010-11 was Rs. 4.50 lakh crore which rose to Rs. 14.37 lakh crore in FY 2021-22.

As of June 30, 2022, outstanding corporate bonds stood at Rs. 39.58 lakh crore. The number of instruments outstanding was 29,745. The average size was Rs. 133 crore – a small amount, leading to low liquidity in the secondary market.

For comparison, the currently outstanding stock of G-Secs is at Rs. 84.71 lakh crore in 100 instruments, making them highly liquid.

SEBI has been making efforts to nudge the market towards re-issuances to reduce fragmentation and improve liquidity.

Other factors that contribute to the limited activity in the secondary market are the “buy and hold” nature of investors and the predominance of a private placement which we will cover later.

Development of complementary markets

Well-functioning derivatives and repo markets play a key role in aiding the liquidity of corporate bond markets by helping investors hedge and manage risks better.

The primary risks associated with holding corporate bonds are interest rate and credit risk. The interest rate derivative market is reasonably liquid, particularly the overnight indexed swaps market. Markets for other interest rate derivative products like swaptions (Swap Options) are still developing.

The lack of a market for credit derivatives, despite regulatory initiatives for more than a decade, is an issue. There seems to be a chicken and egg problem here. The dominance of top-rated issuances reduces the need to manage credit risk, while the development of a Credit Default Swap market is essential for the issuances of lower-rated bonds.

The market for repo in government securities is one of the most liquid markets in the country, but repo in corporate bonds has not taken off. Issues related to the lack of a trading platform like the one available for repos in government securities, lack of a central counterparty, high margin requirements, etc., have impeded the development of the market for repos in corporate bonds. SEBI is trying to facilitate the setting up of a repo clearing corporation.

Issues, concerns, and challenges

Rating profile

In FY 2021-22, 22.5% of the bonds were rated AAA, 29% were rated AA, and 5.3% were non-investment grade. In value terms, 80% of issuances in value terms were rated AAA, and another 15% were rated AA. It is fairly obvious that the corporate bond market largely meets the needs of highly rated corporates.

Mode of issuance

The bulk of corporate bond issuances is through private placement. In FY 2021-22, public issuances of corporate bonds raised just Rs. 11,589 crore – about 2% of the money raised through private placement (Rs. 5.88 lakh crore).

Public issuance is important due to the transparency and efficiency of price discovery. SEBI is making efforts to make the private placement process more transparent and efficient, for example, through the introduction of the Electronic Bidding Process on stock exchanges.

Investor profile

The investor base for corporate bonds is largely dominated by domestic institutions – insurance companies, banks, and mutual funds. Retail participation remains low.

Earlier, we had mentioned the limited access of lower-rated issuers to the corporate bond market for mobilising resources. Part of it is due to the investor base in the market, which is closely regulated and has a preference for highly rated issuances.

Specialised Bonds

Indian corporates have been tapping international markets to raise Environmental, Social & Governance (ESG) funding, while domestically, such issuances have been low. We need to create conducive conditions for ESG bonds in India - greater transparency and credible checks against greenwashing, including through arrangements for independent audits.

The announcement in this year’s Union Budget referring to the mobilisation of resources via ‘Green Bonds’ is expected to enable a price anchor for ESG bonds in due course.

There is also a limited investor base for capital bonds issued by banks in India. This has resulted in Indian banks accessing global markets for raising capital.

Price Transparency

High-quality and timely information on financial markets is basic to the development of the market. While in the G-Sec market, information about every single trade is disseminated in near-real time, ensuring the highest standards of transparency, the timeliness and integrity of data on primary and secondary market transactions in the corporate bond market are still lacking.

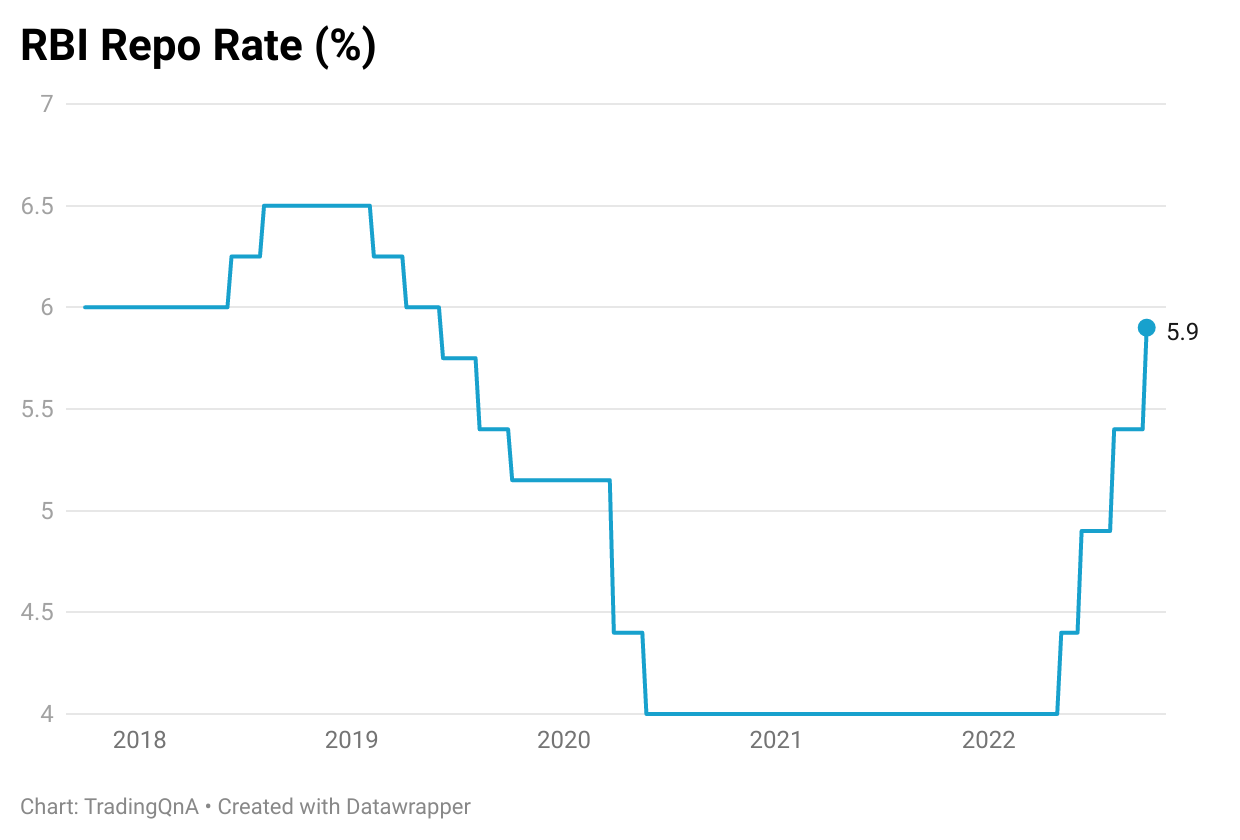

Highlights from the RBI MPC meeting

The Reserve Bank of India, at its monetary policy meeting this week, increased the repo rate by 50 bps to 5.9%. Below are some highlights from the meeting;

The Standing Deposit Facility (SDF) pegged 25 bps below the repo rate stands at 5.65%. While the Marginal Standing Facility Rate, pegged 25 bps above the repo rate, now stands at 6.15%.

The RBI retained inflation projections at 6.7% in 2022-23. Inflation in Q2FY23 was seen at 7.1%, Q3 at 6.5%, and Q4 at 5.8%.

The GDP growth was marginally revised for 2022-23 to 7% from 7.2%. Q2FY23 is seen at 6.3%, Q3 at 4.6%, and Q4 at 4.6%. Growth for Q1FY24 has been revised to 7.2%.

Bank credit has grown at an accelerated pace of 16.2%.

India’s foreign exchange reserves stand at $537.5 billion. The forex reserves last year by this time were $640 billion.

These terminologies are hard to understand; explain to me like I’m 5.

Here’s a thread where we’ve broken down the key terms about the RBI policy meet. This will come in handy whenever you feel like you need a little help with understanding such macros:

Suyash Choudhary, the head of fixed Income at IDFC Asset Management, who’s one of the most sensible bond market watchers, had a succinct take on the policy meeting. A few highlights from his piece:

If what one looks for is assured navigation in central bankers, then Das is amongst the best we have ever had. Thus there is a clear recognition of our strengths and a sense of confidence in the face of global challenges.

We expect the repo rate to peak at 6.15 – 6.25% in this cycle with the final hike likely in the upcoming December policy. This is higher than our earlier expectation of 6% and reflects changes to DM rate forecasts by a very sharp extent lately, something that we weren’t expecting earlier. This still means that we don’t have to follow the US Fed lockstep, even as some upward adjustment is prudent given the latest aggressive changes in Fed (and other DM central banks’) terminal pricing lately.

The global slowdown will take its toll via the export channel. Thus it is highly unlikely that the current momentum on domestic growth continues, even as India’s relative growth will still be much better compared with much of the world.

Our current account deficit (CAD) is an issue, but it is on account of two factors: One, the commodity shock emanating from the Russia-Ukraine conflict was in effect a forced exporting of savings for a commodity importing nation such as India. However, this shock is unwinding in a host of commodities and this should have a salutary effect on our CAD with a lag.

Dive deeper here

Inflation is going to be a long nightmare!

Came across this really interesting chart from Thanos Vamvakidis of Bank of America Corp. According to his analysis, once inflation crosses 5% in advanced economies, it takes 10 years for it to drop.

This is as scary as things can get for emerging markets like India because if advanced economies don’t do well, we won’t either.

An extreme nightmare scenario is that if inflation becomes entrenched, the US will have to hike rates aggressively, which means a stronger dollar.

A strong dollar is a nightmare for the global economy, especially for the most vulnerable emerging and developing countries and corporates.

But given the looming fears of a recession in the US and stagflation in Europe, a large segment of the market thinks that inflation will moderate in the next 1-2 years.

The majority view seems to be that inflation won’t be back to the pre-pandemic lows but will remain in the 3-4% range. At this point, this is probably the best outcome one could hope for.

Speaking at the Sohn conference earlier this year, legendary investor Stanley Druckenmiller made a similar observation. Here’s a lightly edited snippet:

Two undefeated records are once inflation gets above 5%, it's never come down unless the fed fund rate has gotten above the CPI. Since the CPI is 8% that would call for a fed funds rate of above 8%. Frankly, I don't think we'll get there because of the extent of the asset bubble and the damage that would be done. Think about the fact that we have virtually no bankruptcies.

The other statistical fact is once inflation's got above 5% to use your word, it's never been tamed without a recession. So if you're predicting a soft landing, you're going against decades of history. It could happen, anything's possible, but I don't think it's probable.

Interesting bits from around the web

Reading Recommendations

Surviving a Bear Market When You’re Done Saving by Ben Carlson

Financial planning is far more complex for someone spending down their portfolio than someone building it up.

When you’re young, time and human capital are your biggest assets. You have time to allow compounding to be the wind at your back. You have the time to wait out a prolonged bear market.

A retiree sits in an entirely different position when it comes to assets. You don’t have nearly as much time to wait out nasty bear markets. You don’t have income from your job anymore. And you have to shift from an accumulation mindset to one of decumulation since you need to begin taking withdrawals from your portfolio.

Thank you for reading, that’s it from us today. Hope you loved reading the latest issue, do let us know your views in the comments section below. And do like and share 😃

If you have any queries related to trading, investing and anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna