AI, Ukraine's economy, you are better off investing on your own, limits of diversification, P2P lending and more

AI, Ukraine's economy, you are better off investing on your own, limits of diversification, P2P lending and more

#Issue 28

This time, it feels different (about AI)

I have been covering interesting pieces related to AI in this newsletter. You can read some of them here and here.

The reason why this resonates with us is because of its potential to exacerbate inequality and cause job losses. We have tried to address some of the AI related anxiety for our employees by coming up with our AI policy.

Click here to read the entire thread.

Along these lines, this is what Kailash Nadh, our CTO, has to say about AI/LLM in his blog post: This time, it feels different:

It (the AI policy) states that no one at Zerodha will lose their job if a technology implementation (AI or non-AI) directly renders their existing responsibilities and tasks obsolete. The goal is to prevent unexpected rug-pulls from under humans. Instead, there will be efforts to create avenues and opportunities for people to upskill and switch between roles and responsibilities. While this is a reassuring stopgap for individuals in the organisation who have been naturally asking questions fueled by AI anxiety, it is not an unconditional AI-shield or a bulletproof solution. The fact that such a policy had to be formulated marks an inflection point, the implications of which, I am yet to comprehend. Neither blockchain, serverless, web3, big data, nor earlier AI / ML technologies brought this about. But, the specific breakthroughs in the past few months finally did. All it took was 30 minutes to integrate, during which, it generated the code to integrate itself. This time, it feels different.

The blog makes you ponder about larger questions regarding efficiency gains, decision making, job losses, regulatory response and streamlining of organisations.

Whats happening with Ukraine’s economy

When Russia invaded Ukraine many assumed it would be a one-sided conflict and Ukraine’s economy would be snuffled out, but Ukraine seems to have pulled through much better than expected.

The International Monetary Fund upgraded its growth forecasts for Ukraine projecting that Ukraine’s economy will expand between 1% and 3% this year, from a range of -3% to 1% earlier.

A McKinsey report has noted that Ukrainian businesses have shown remarkable resilience, with 98% of companies surveyed by McKinsey managing to continue operating despite “extremely deep and wide ranging” hits to sales. It also stated that Ukrainian companies swiftly adjusted and prioritised the preservation of team spirit, leading to the majority of them successfully keeping a large portion of their workforce. Right now their primary focus is onexpanding their supply networks and exploring new avenues for generating revenue.

Source: McKinsey

You are better off investing on your own

I just came across this article by Vivek Kaul where he says that in the last 10 years only 2 out of 5 regular mutual fund schemes in India delivered returns equal to or higher than their benchmark.

2 basic questions first. What are regular mutual funds and what is this benchmark that we are talking about?

Mutual funds come in 2 avatars. Direct and regular. In a regular scheme, investors use a distributor to invest thus there is an extra expense charged to you to compensate them. Under the direct route, there are no middlemen and hence no commissions, thus lowering the expenses and ensuring higher returns. So how do you find direct mutual funds to invest in? Coin is here to the rescue.

The performance of a scheme is measured against a benchmark, which represents the

broader market. For example, the benchmark of a large-cap scheme might be the Nifty 50 index.

If you are very new to this, I recommend that you go through this chapter on Varsity.

Now let's get to the meat of it. Why would you want to invest in mutual funds? I’d do it because I would like someone with expertise to manage my money and so that I can continue with my life. The problem now is that these MFs aren’t beating the benchmarks. Wouldn’t I be better off just investing in the Nifty 50? I don't have to pay for any expertise, and I still generate decent returns. On top of that, I eliminate the effort/luck of choosing the right MF.

So how do I invest in the benchmark? Welcome to the world of index funds. Click here to read more about this.

Diversify your portfolio, but to a limit: Play the winner’s game

Don’t put all your eggs in one basket. This is something we have grown up hearing in some context or the other. This applies to investments as well. But like all things, there is a limit to it. To understand this better, let's talk about your stocks portfolio.

A certain level of diversification is beneficial; having a portfolio of 5 stocks significantly lowers the standard deviation (risk) compared to owning only 1. But there is a point where you will eventually reach a point of diminishing returns. There isn't a fixed number for everyone but typically, the advantages of diversification should cease at around 20-30 stocks. Beyond this point, adding additional stocks to the portfolio primarily reduces potential return rather than further reducing risk as per this post by Conor Mac.

Having too many stocks in a portfolio is hard work (assuming you aren't a professional with a dedicated team for this, if you are then this post is not for you). The hidden costs are just too much. You will spend most of your time on due diligence and trying to figure out the latest developments, in most cases you will do a poor job of it because I am assuming you have a life to live as well. Whether it results in a poor quality of life or a poor quality of due diligence, neither outcome is efficient

In the latter part of this post Conor talks about how in every endeavour in life, there are two games: the winner’s game and the loser's game. Lets try to understand what these two mean through a tennis game analogy from this paper:

“In a match between two professionals, the gameplay is hard-hitting, precise, and the players are attempting to play the ideal sequence of shots to put their opponent at a very slight disadvantage. The margins are fine, and the points will be dictated by the skill of each player. They are playing to win. For two average joes schlepping it at their local court, each game is likely to be decided by whoever makes the least unforced errors. The next time you play tennis or table tennis with an equally matched friend, try focusing solely on returning the ball to the other side of the court and avoid making any fancy shots. Let them make the errors, and watch the points roll in. These are two entirely different ways of playing tennis, and this phenomenon of winner’s and loser’s games exists everywhere.”

Just like tennis, you can be a successful investor by approaching the game in your own way. However, what sets investing apart is that everyone shares the same court simultaneously. Regardless of the specific strategy you adopt, please note that you are ultimately competing with professionals.

This concept of winner's and loser's games has really interested me. If you want to find out more about it and become a better investor read this.

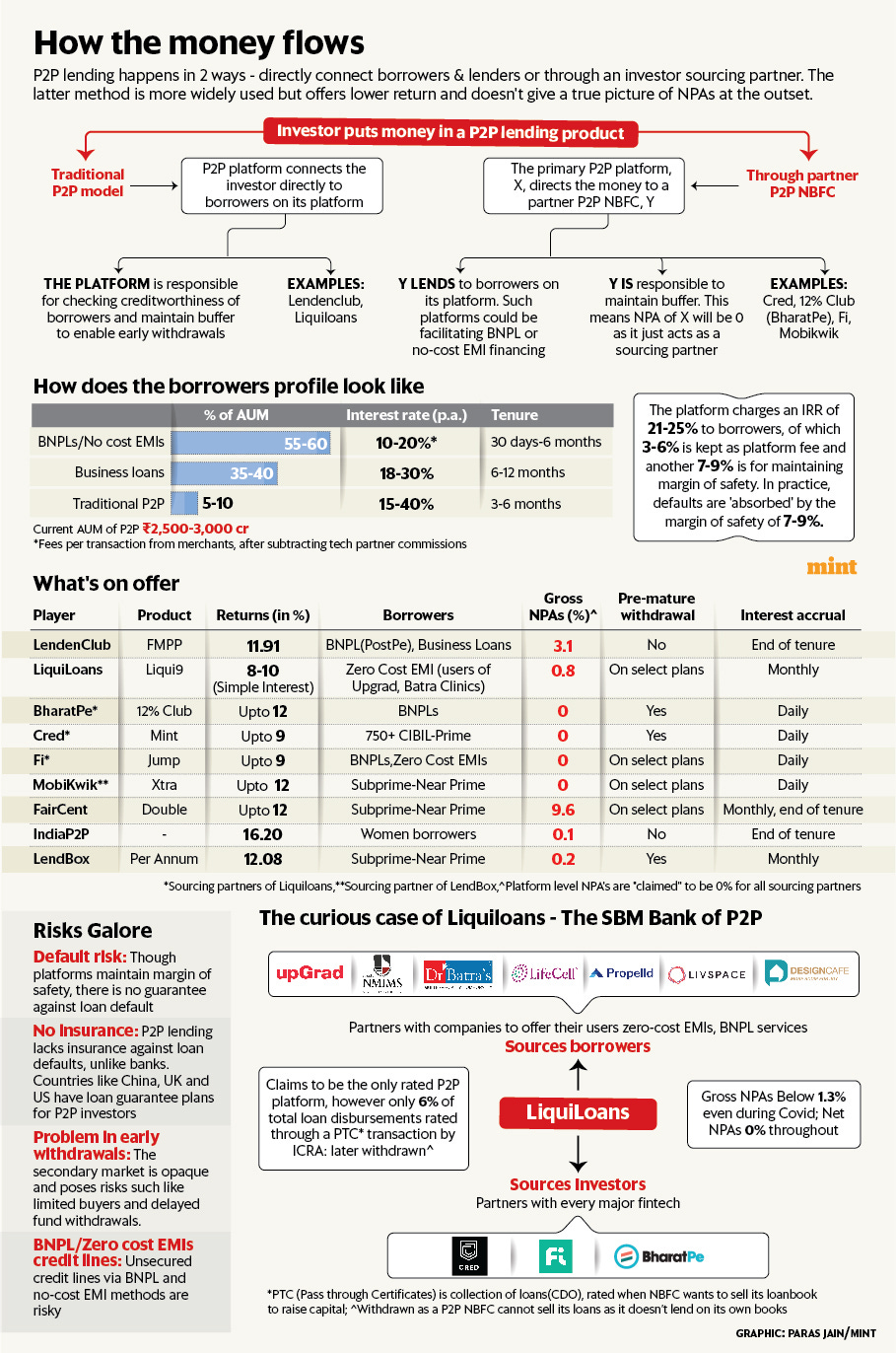

Peer to Peer (P2P) lending

You would’ve heard something about Peer to Peer (P2P) lending. It has emerged as an alternative investment. It gives you a lucrative opportunity to invest for short periods at a 10-25% rate. P2P lending is also very flexible allowing on demand withdrawals in contrast to traditional bank fixed deposits.

Is it something you should be looking at? Akshat Rohtagi discusses this in his article where he explores the Indian P2P lending market.

“While theoretical risks of borrower defaults exist, P2P lending platforms have taken measures to mitigate such risks. They tend to absorb losses within their buffers, minimising the potential losses and adhering to principles of the BASEL III capital norms implemented for banks.

However, this may create a false sense of security among investors. Initially, the idea was to connect lenders with individual borrowers directly but over time P2P lending has evolved to bring in an interesting mix of borrowers, diversifying potential opportunities within the industry.”

This article covers the P2P space in great detail and makes for a very interesting read.

Auto Finance NBFCs

Centrum broking has recently shared an interesting report on the Auto Finance NBFCs and my colleague Meher has taken out some insights from the same in this TradingQ&A post.