A report card for Indian VCs

#Issue 23

This is the latest issue of Markets and Macros by TradingQnA written by Abhinav and Shubham.

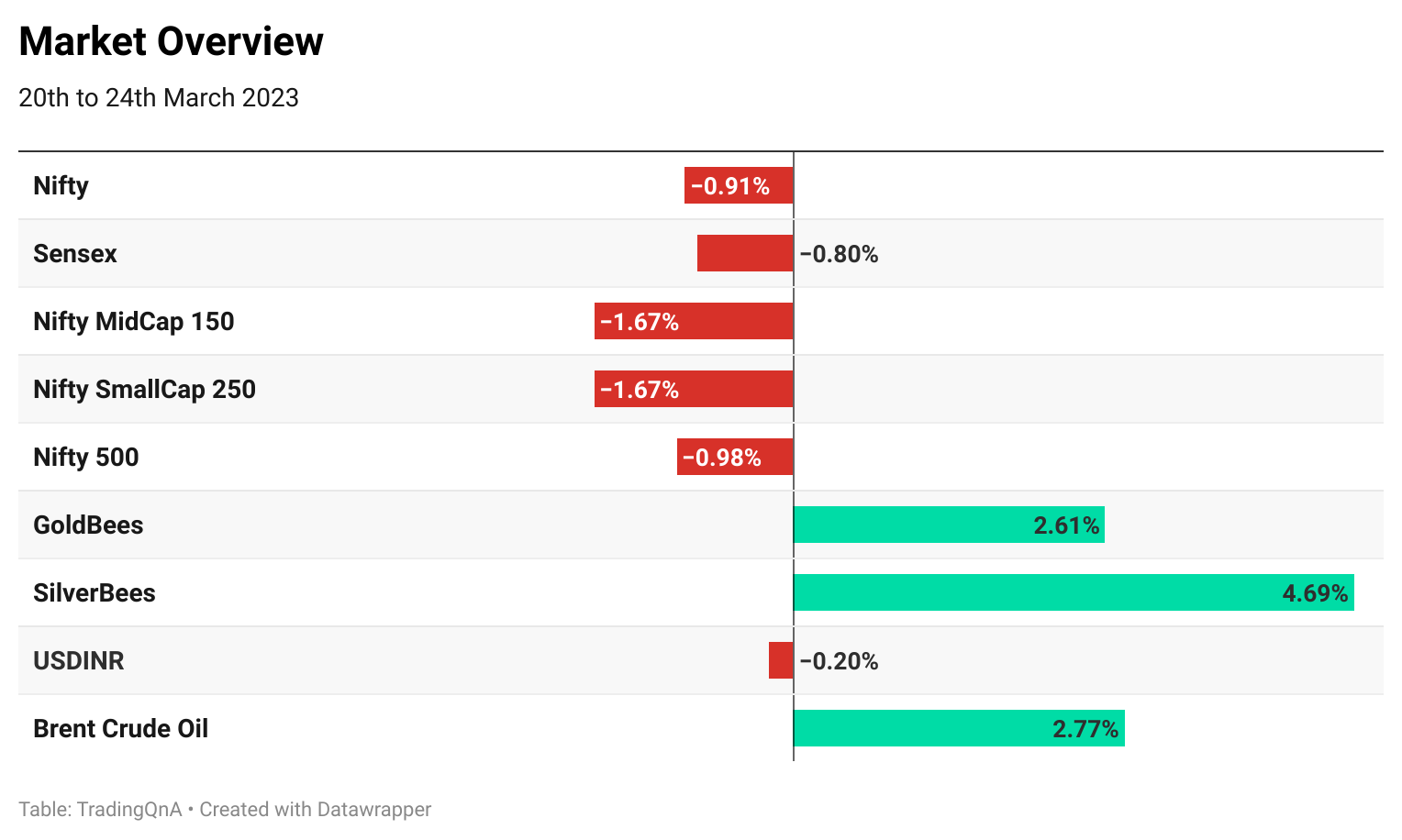

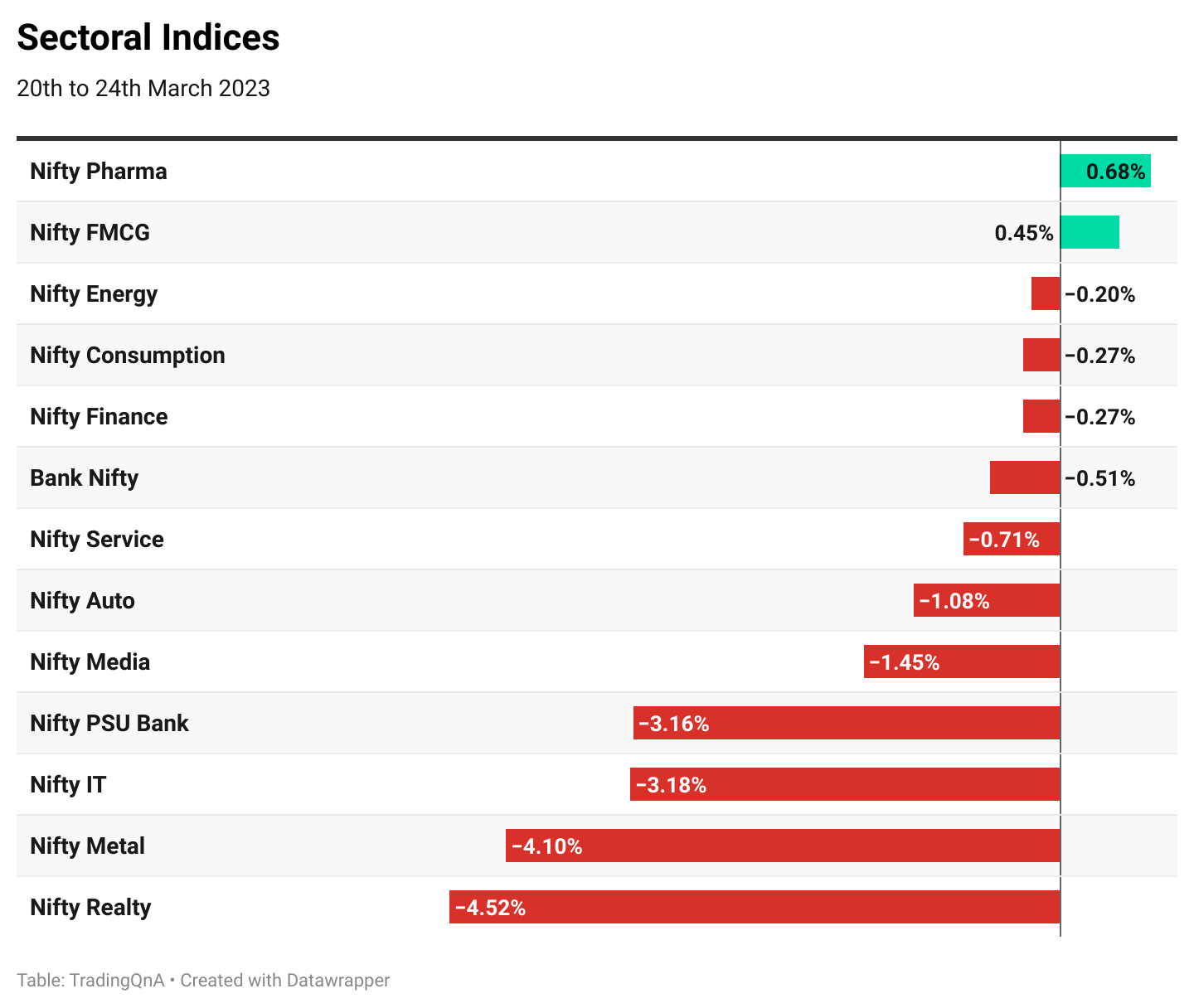

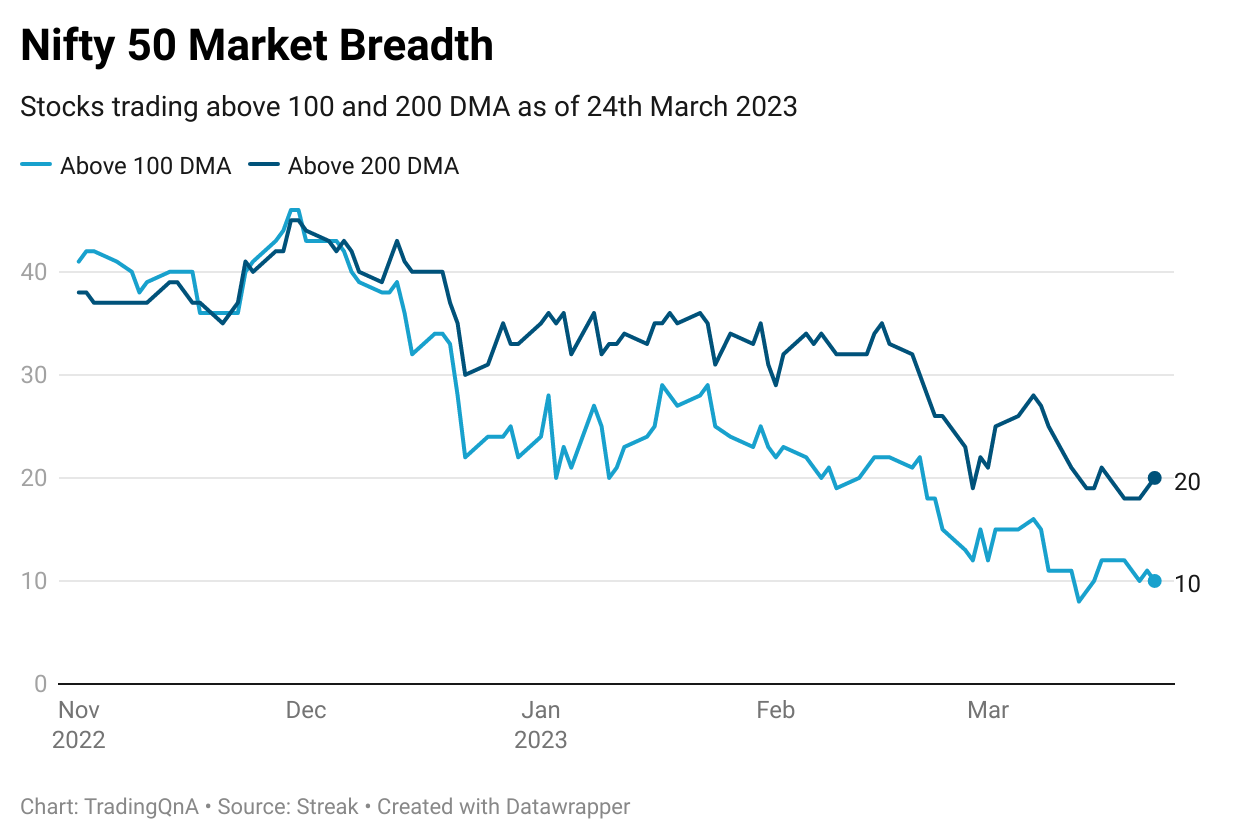

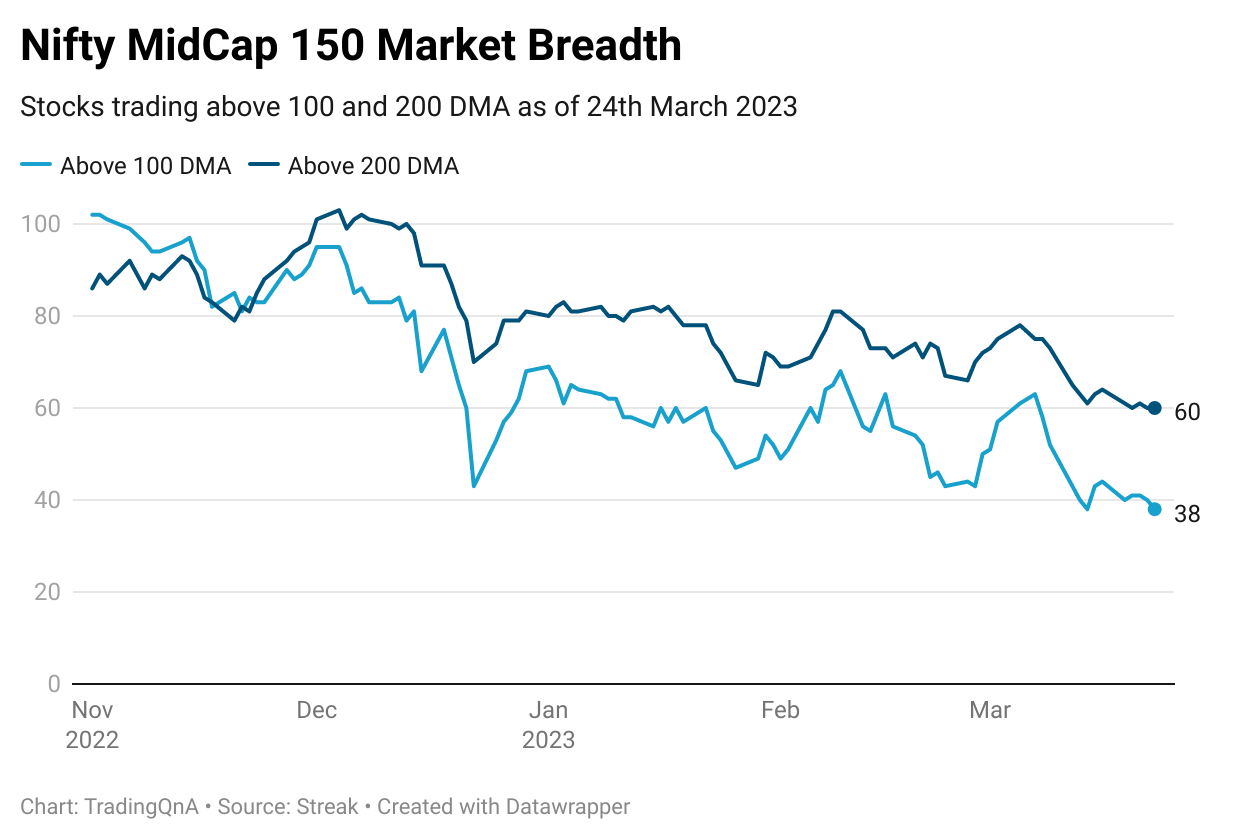

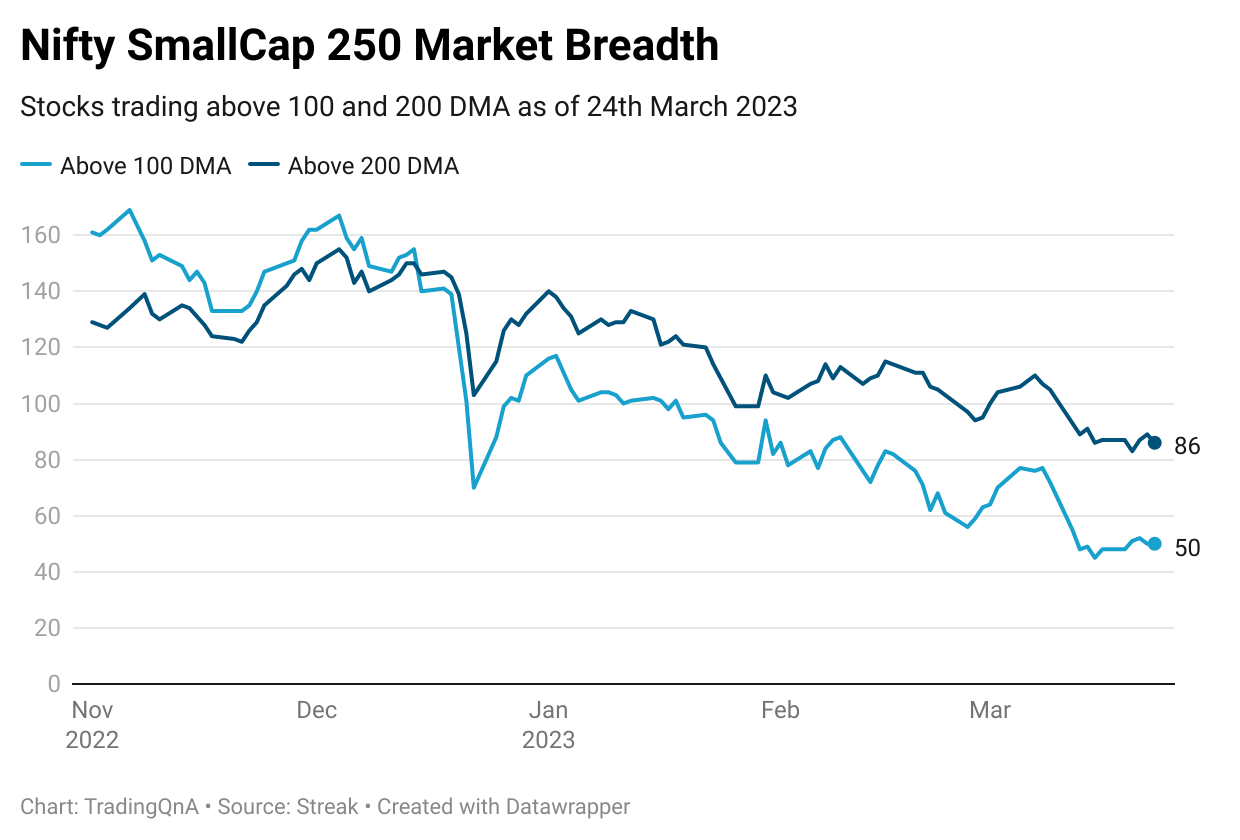

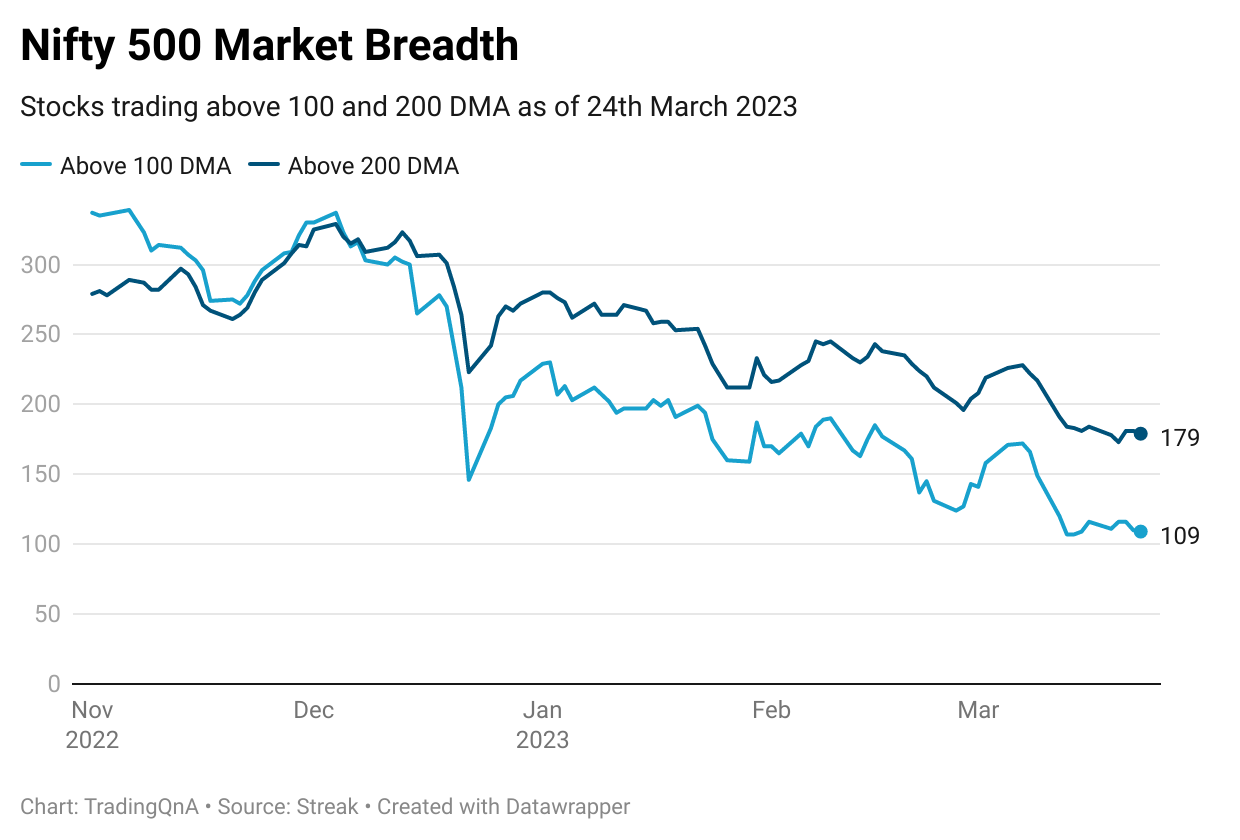

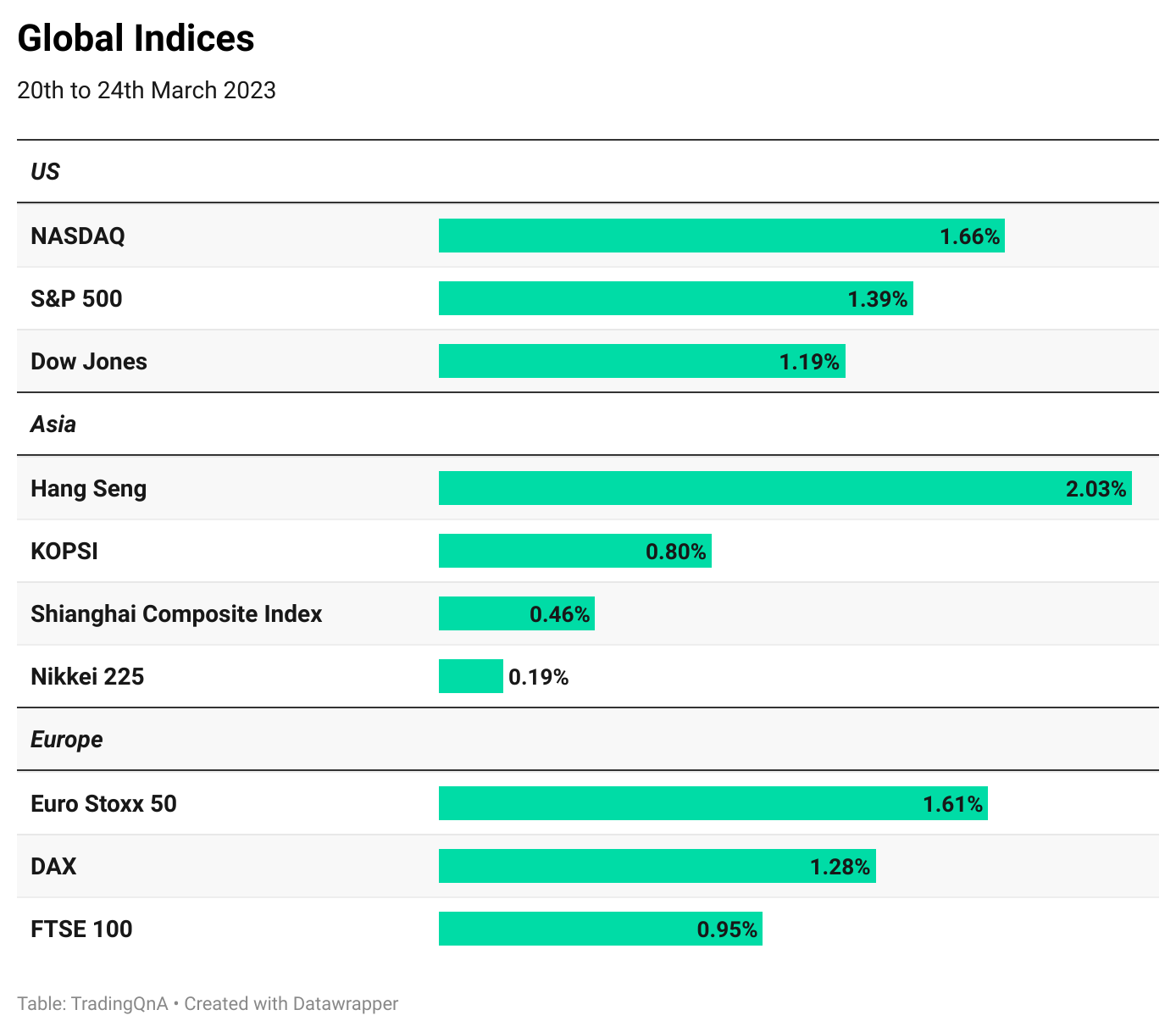

Weekly market wrap

A report card of Indian VCs

Bain and Company recently released the India Venture Capital Report 2023 and there are some interesting insights from this report that are worth noting.

2022 was a year of recalibration for VC investments after a record capital influx over the last few years. This was triggered by

monetary policy tightening

intensifying geopolitical tensions (Russia-Ukraine conflict, US-China decoupling)

sanctions and ensuing global supply chain shocks

corporate governance irregularities across the tech ecosystem (Sam Bankman Fried for example).

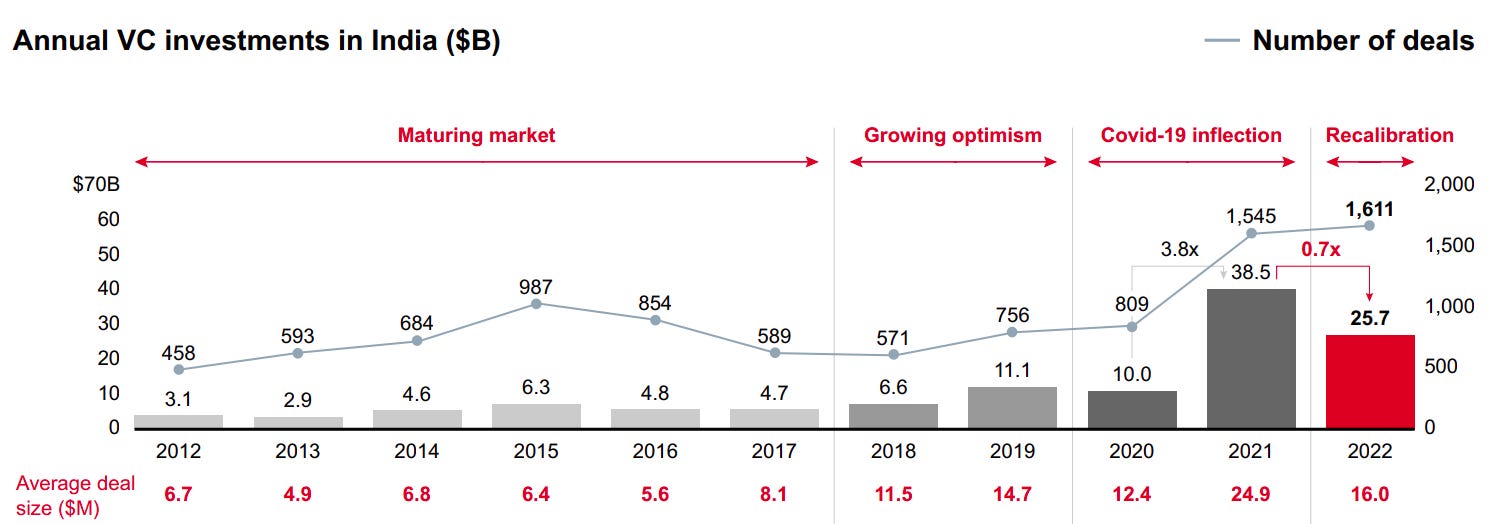

For India, the total deal value reduced from $38.5 billion to $25.7 billion from 2021 to 2022. However, India can be resilient because of some structural advantages like

Large consumption base: A sizeable middle class with a large working-age population, a services-driven economy and an expanding manufacturing base.

Inclusive economic growth led by scale adoption of digital rails: UPI for payments, ONDC for e-commerce, electronic health records and cheap access to data.

Fiscal and monetary discipline: Judicious fiscal stimulus during the pandemic, efficient commodity sourcing given global price volatility keeping inflation in check.

Global push to reduce dependence on China: Incentives boosting manufacturing (like PLI) and a push for global supply chain diversification. We had written about this topic in detail in our previous newsletter.

While the average deal size reduced from $25 million to $16 million, deal volume expanded marginally (indicating significant early-stage activity as the seed and series A-B funding rounds are of a smaller ticket size). Megarounds ($100 million+) reduced from 92 in 2021 to 48 in 2022 while early-stage deals saw a ~1.2x growth in volume compared to 2021.

Source: Bain and Company

India’s share in Asia-Pacific VC investments increased to ~20% compared to ~17% in 2021.

Bain and Company also hinted at a maturing ecosystem based on an increasing share of investment outside of Mumbai, Bengaluru, and the NCR to 18%. In 2022, 9 of 23 unicorns were from these cities implying a democratisation of funding.

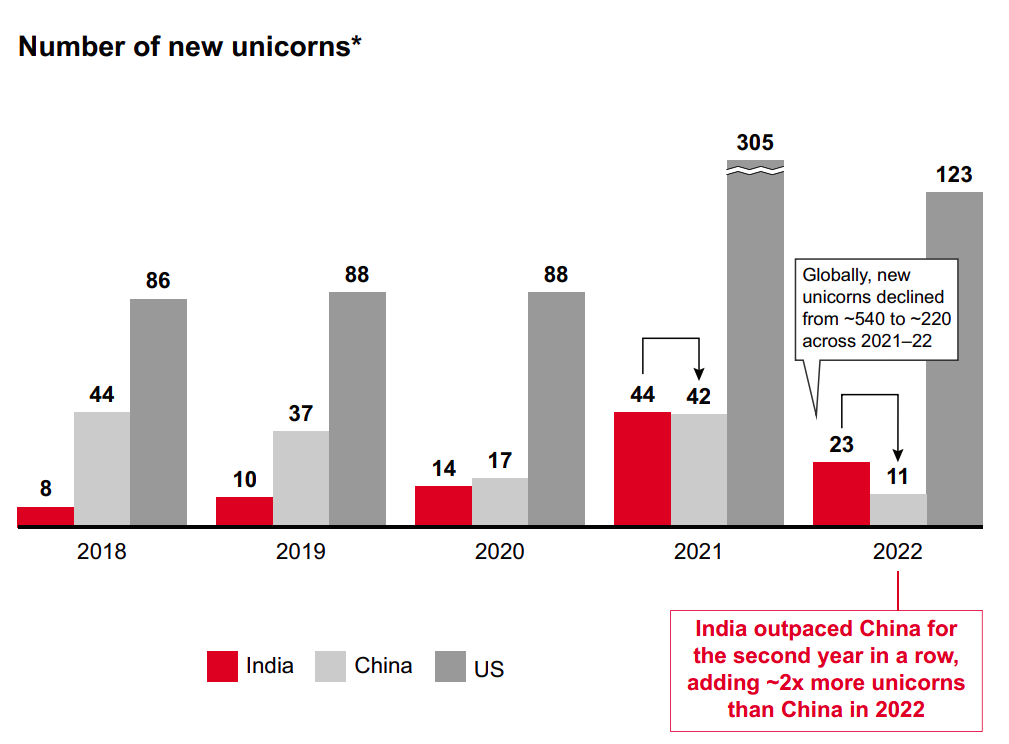

While the number of unicorns shrank from 44 to 23 over 2021–22, India added more unicorns than China, 23 and 11 respectively, for the second year in a row. India became the 3rd country to have created 100+ unicorns—Open Technologies became the 100th unicorn in May.

Source: Bain and Company

A sector-wise look

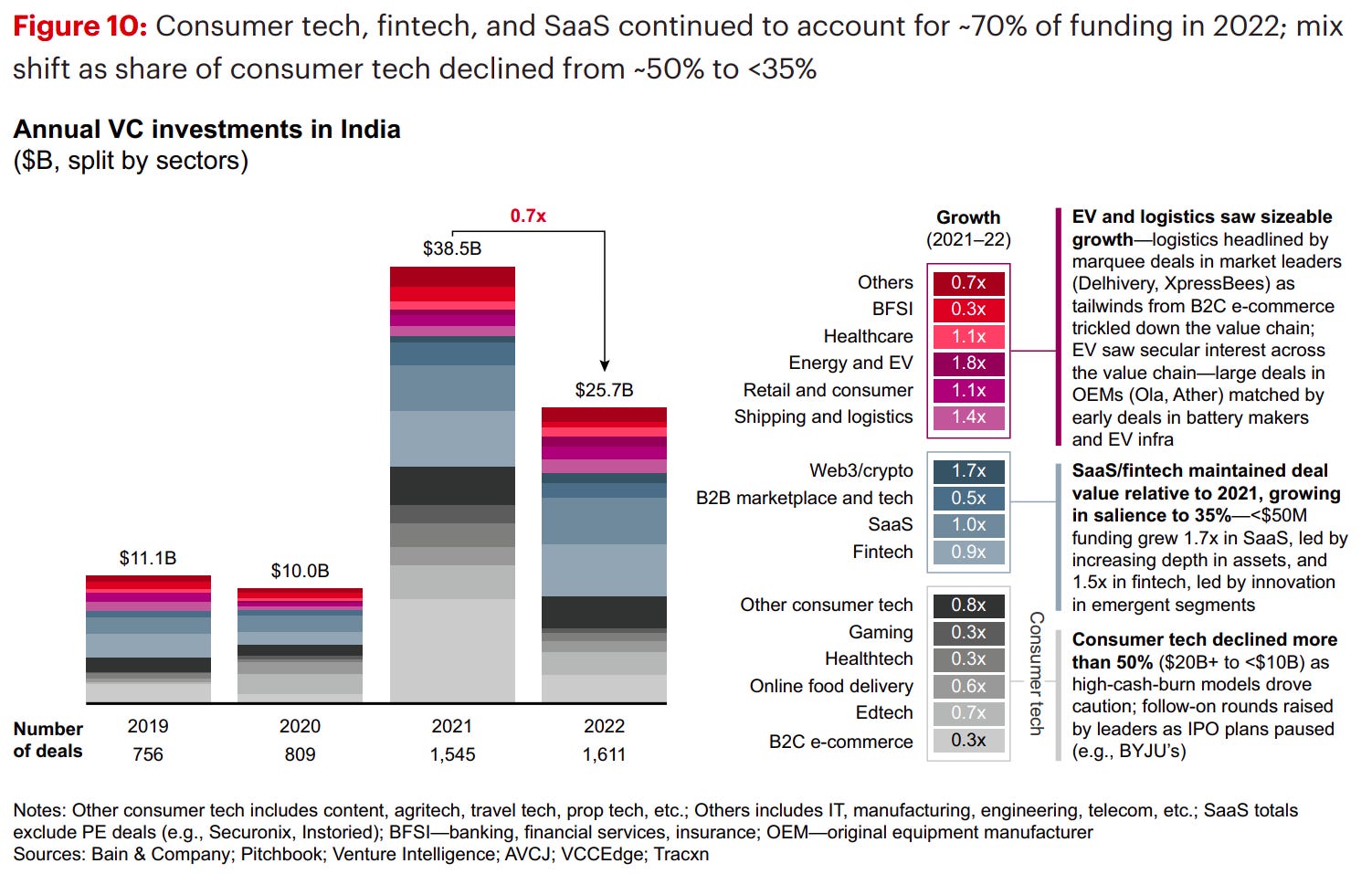

Software-as-a-service (SaaS) and fintech grew from ~25% in 2021 to ~35% of total funding in 2022.

Consumer tech saw a 55% drop, from more than $20 billion in 2021 to less than $10 billion in 2022. This was seen across segments such as ed-tech, online food delivery, B2C commerce, and D2C brands. Due to the typically higher cash-burn business models in consumer tech, investors were cautious about large deals in 2022.

Emergent sectors like electric vehicles, agritech and deep tech (space tech, generative AI and climate/clean tech) saw significant interest.

Shipping and logistics grew 1.4x on the back of marquee deals—three deals of $300 million+ (Delhivery, ElasticRun, XpressBees) and three unicorns were added (Shiprocket, ElasticRun and XpressBees).

Source: Bain and Company

Where is the money coming from?

Share of leading funds reduced to <20% from 25% as activity from global crossovers and hedge funds slowed down.

While traditional PE funds continued to demonstrate interest in select growth equity deals and participated in several $100 million+ megadeals, micro VCs presence saw a significant increase in 2022. The base of active micro VCs grew from 65 to 80+ over 2021–22. Thematic micro VCs and women-founder focused VCs increased activity.

Family offices, corporate VCs, and first-time funds were active with 300+ deals, in line with 2021.

In sharp contrast with the slowdown in investment activity, 2022 saw record fund-raising as multiple investors raised their largest ever India-focused funds.

What about exits?

There was a large decline in exits with VC participation in 2022, relative to 2021, from $14 billion to less than $4 billion in total exit value. Secondary transactions accounted for 47% of the exits, but the overall value dropped as large anchor exit deals declined (only 11 secondary exits greater than $50 million in 2022 compared to 19 in 2021).

The share of public market exits was 40% but saw a shift from IPO-driven exits to trades—specifically exits by anchor VC funds as lock-ins on tech IPOs expired but total

IPO-driven exit value remained muted relative to 2021. Several IPOs were deferred in 2022 affecting overall exit value.

Has the startup ecosystem changed?

Some of the fundamental shifts which will have a near to medium-term effect are:

Investors: They pivoted from “growth at all costs” to “sustainable unit economics” and venture debt as an alternative funding option became viable.

Regulators: Regulatory tightening affected fintech and cryptocurrency the most. Apart from this, regulations continued to act as enablers in the ecosystem ( PLI, a framework on tech listings by SEBI and an ongoing focus on building public digital rails such as Open Network for Digital Commerce).

Start-ups: There were more than 20,000 layoffs, several distress mergers and acquisitions, corporate governance issues and more than 10 deferred IPOs.

There was a growth of new emerging hubs and increased diversity in leadership positions within start-ups.

What lies ahead for us?

In the longer term, global investors will remain positive about the India Story due to solid macro-fundamentals, a large consumption opportunity, a sizeable workforce entering the formal economy, a digitally enabled population and a deepening innovation ecosystem.

Interest rate cycles and bonds

Before moving further let’s establish some basic concepts about long-term and short-term bonds.

When interest rates fall, long-term bonds benefit more due to their greater sensitivity to rate movements. This means that their prices increase, resulting in more significant returns. However, in a situation where interest rates and inflation rise, these assets can experience a sharp drop in value. The last year serves as a good example of this.

Short-term bonds have little to no interest rate risk, making them less vulnerable during periods of rising interest rates but at the same time short-term bonds offer lower returns and do not provide as much protection against recession or deflation as long-term bonds. This is because short-term bonds lack the price appreciation component of long-term bonds when interest rates fall.

US perspective

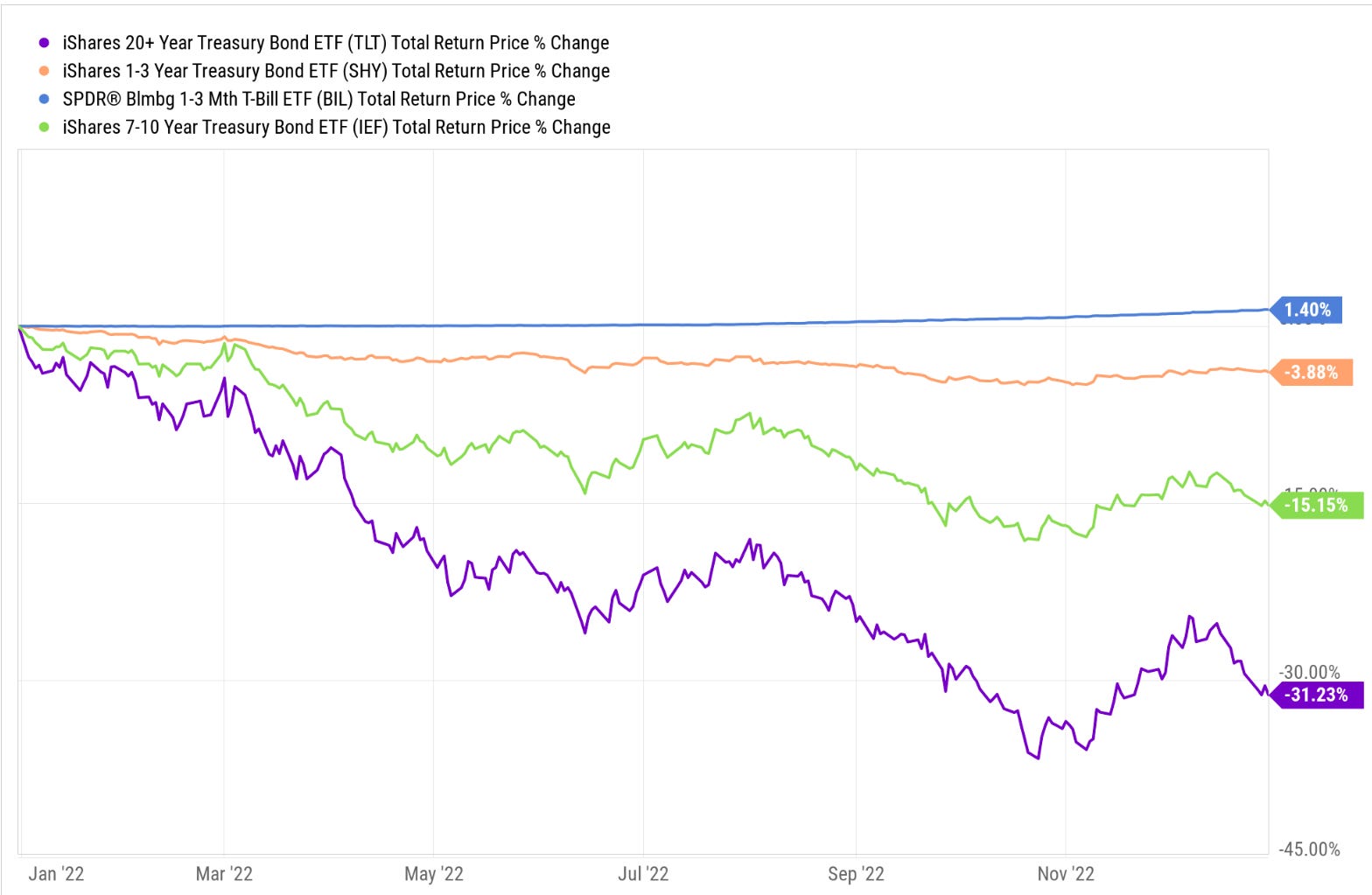

Over the last 2-3 decades, investors were enamoured with the concept of holding long-term bonds as they typically yielded higher returns and served as a buffer during most stock market downturns. However, this trend changed last year. Take a look at the performance figures for long bonds, intermediate bonds, short bonds and ultra-short bonds (essentially cash) in 2022:

Source: A wealth of common sense

In short, long-term bonds experienced a significant drop, declining more than the stock market. Intermediate term bonds were also heavily impacted, while short-term bonds experienced a smaller decline and T-bills were not affected.

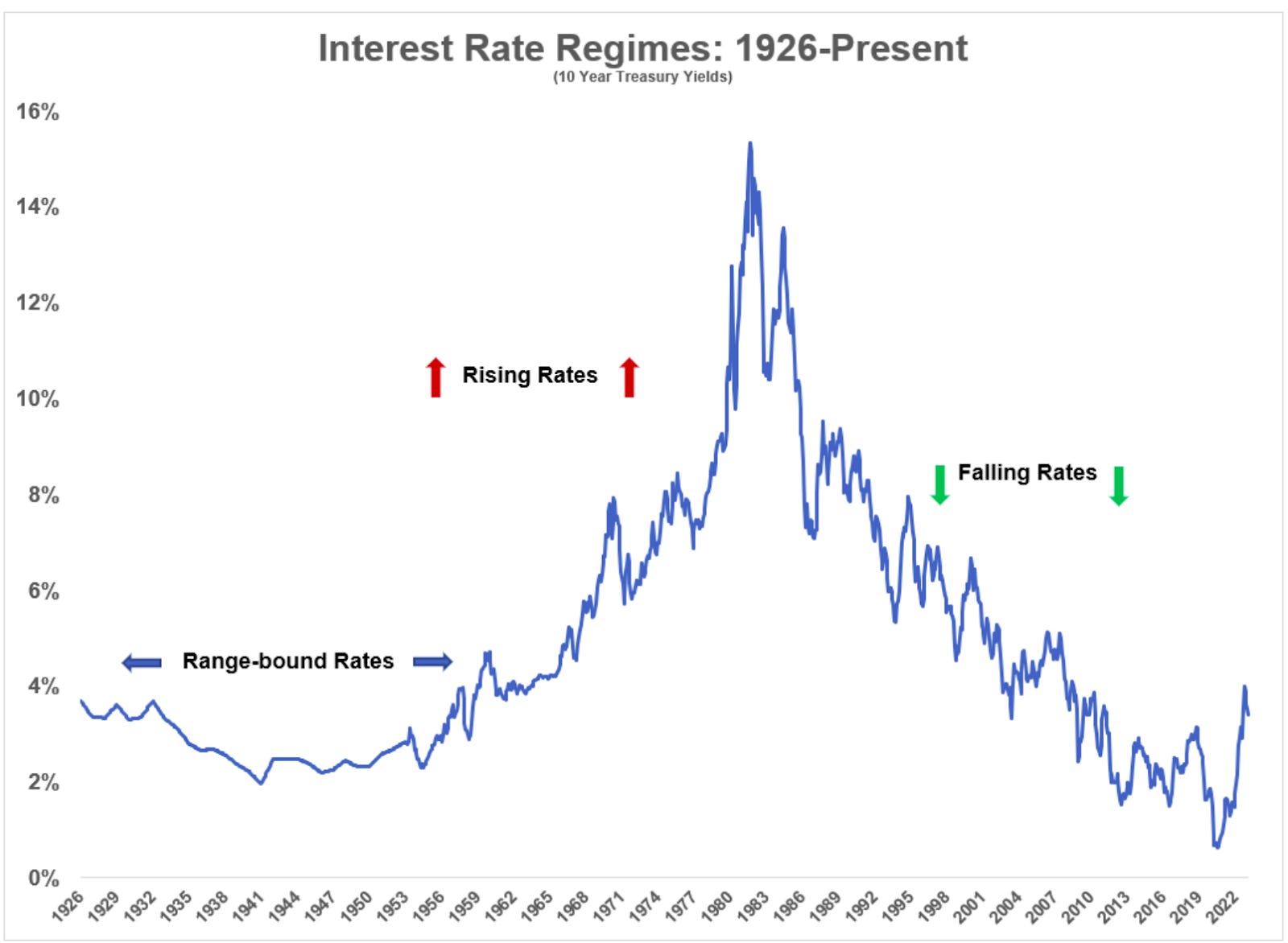

Last year was a bad year but it was just 1 year. Let us look at the secular interest rate cycles to see how different bond maturities have fared historically. This article states that there were essentially 3 interest rate cycles in the US. The graph below traces the 10-year treasury yield through these cycles.

Source: A wealth of common sense

Under normal circumstances where interest rates remained stagnant, riskier bonds performed better than risk-free T-bills. However, when interest rates and inflation were high, cash investments outperformed both intermediate and long-term bonds. For a period of 3 decades, one-month T-bills yielded better returns than long term bonds.

Conversely, during the following 4 decades, when interest rates rose, long-term bonds experienced significant gains during a remarkable fixed-income bull market. It is uncommon to earn an annual return of 7-10% in bonds.

India

About interest rates in India, I found this research paper. This is a short summary:

India’s interest rates are inflexible due to high public debt, non-performing assets, and the RBI’s policy of accumulating foreign exchange reserves. They are influenced by both domestic and international factors with interest rates primarily being affected by movements in international interest rates, with a significant lag.

As India’s interest rates integrate with global rates its financial markets are not immune to the global financial system.

Take a look at the graph for 10-year Gsec yields for India. One thing to note is that a developing country like India is expected to have a higher floor of interest rates than rich countries with surplus capital.

Source: CEIC

A few economic pundits are predicting that the cycle of rate increases in India might end soon. How does this affect your investments in fixed-return assets? DSP has shared some interesting insights about this.

If you have any questions about bonds, we have a specific category for you on Trading Q&A which can help you.

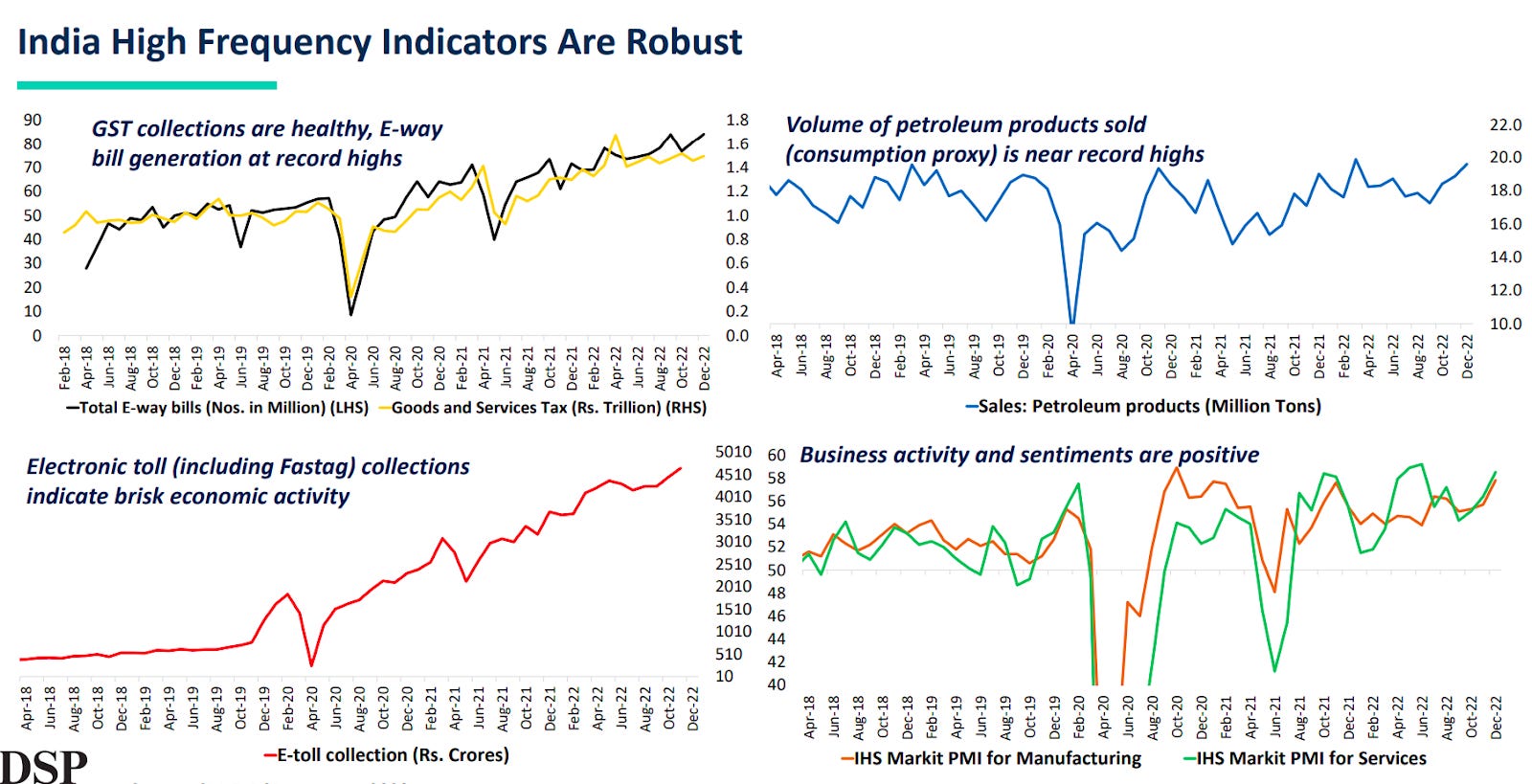

Indian economy through charts

Source: DSP

Can money buy you happiness?

Something that I have felt intuitively has now been confirmed by some new studies that having more money can improve our well being.

The process of reaching a conclusive answer to this question is quite fascinating. In 2010, Daniel Kahneman, a Nobel Prize-winning economist and psychologist, proposed the idea that there exists a monetary happiness plateau. According to this theory, once you reach a certain income level, earning more money does not increase your happiness. However, in 2021, Matthew Killingsworth published a study disagreeing with this theory, demonstrating that happiness does in fact increase with income and there is no evidence of a plateau.

Now, the two researchers have collaborated on a new study, which suggests that both of their previous conclusions have some truth to them, but Killingsworth’s idea is more accurate. In general, earning more money tends to make most people happier, but there are some nuances and complexities to this phenomenon that must be considered.

“Does money buy happiness?” is not the right way to frame this question. A better way to frame it is “What is the value of money beyond its basic utility for survival? Where do the laws of diminishing returns kick in? Read this to find out more.

Something to listen to over the week

Thank you for reading. do like and share this with your friends and let us know your views in the comments section below.

If you have any queries related to trading, investing or anything related to stock markets, post them on our forum.

For more, follow us on Twitter: @Tradingqna